EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

1

Current Challenges in Housing

and Home Loans:

Complicating Factors and

the Implications for Policymakers

Eric S. Rosengren

President & Chief Executive Officer

Federal Reserve Bank of Boston

The New England Economic Partnership’s

Spring Economic Outlook Conference

on Credit, Housing, and the Consequences for New England

Boston, Massachusetts

May 30, 2008

As someone who is an ardent consumer of good economic analysis, I have often

been the beneficiary of work done by the New England Economic Partnership. So it is

certainly a pleasure to be with you today to participate in your discussion of current

trends in the economy, and credit and housing matters.

1

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

Over the past year, the economy has been buffeted by a series of shocks including

financial turmoil; an emergency acquisition of a major investment bank to avoid a

sudden, disorderly failure

2

; falling national housing prices; and oil prices that have

exceeded $130 a barrel. Despite all these challenges, the U.S. unemployment rate is at 5

percent; the rise in prices of “core” consumer goods and services (Personal Consumption

Expenditures) to a little above 2 percent, while unwelcome, has not been large compared

with past episodes; and the economy has been growing, albeit at a much slower pace then

we would prefer. These relatively benign outcomes to date are at least partly the result of

recent monetary and fiscal policy actions taken to mitigate some of the problems facing

the economy.

In keeping with the title of your conference – “Crunched: Credit, Housing and the

Consequences for New England” – I am going to focus on the continued downside risk

posed by falling asset prices, particularly in the housing sector. Residential investment

(the housing component of GDP

3

) has declined for nine straight quarters, and in all

likelihood will decline this quarter as well. This has been an unusually long period of

continuous decline in the housing sector, and coupled with falling housing prices

nationally, has complicated predictions of what will happen in the economy going

forward.

I would like to begin by first looking at some of the macroeconomic issues related

to the housing sector, and considering why – despite being a relatively small component

of GDP – housing continues to be a source of such significant uncertainty in the

economy.

2

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

Then secondly, I will discuss some of the varied and interesting research done

recently at the Federal Reserve Bank of Boston by economists and analysts (including

Prabal Chakrabarti, Chris Foote, Kristopher Gerardi, Lorenz Goette, Kai-Yan Lee, Adam

Shapiro, and Paul Willen). This work highlights some striking differences, and some

similarities, between the current housing problems and those experienced in New

England in the early 1990s. In particular I will note the observation that foreclosures

remained elevated well after their peak in the last downturn, and the finding that multi-

family properties are playing a much more important role in the current housing

downturn.

Thirdly, I am going to discuss why developing solutions to the current housing

problems has not been easy, and why the housing sector, despite being sensitive to

interest rates, remains very weak notwithstanding a significant amount of monetary

stimulus in the form of Federal Funds rate reductions. In particular, I will highlight the

important role of so-called “piggyback loans,” or second mortgages; the implications of

homeowners having “negative home equity” as a result of falling house prices; and the

complications created by the securitization of many mortgages.

Finally, I am going to briefly discuss some implications for policymakers in

seeking to develop and implement responses to the problems posed by falling house

prices and rising delinquencies and foreclosures.

I. Macroeconomic Implications of Housing Trends

Figure 1 highlights how precipitously single-family housing starts have declined

since their peak. This is actually the largest peak-to-trough decline in housing starts to

3

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

cade,

occur in nearly 50 years. The decline is occurring in what would seem, in fact, to be a

relatively benign economic environment, with U.S. unemployment at 5 percent and

interest rates low by historical standards.

However, the reduction in credit availability generated by recent, significant

disruptions in the securitization of mortgages has made it particularly difficult for

borrowers seeking subprime

4

and “jumbo” loans. What was likely to be a weak

residential market has become a market characterized by major declines as builders seek

to reduce their swelling housing inventories and as continuing price declines raise the

costs of holding on to land or unsold homes.

These problems have begun to have an impact on some financial institutions that

had taken outsized positions in construction loans, or whose business model was focused

on the types of residential lending most impacted by the downturn. Of course, the

dramatic decline in housing starts should expedite the process of reducing the inventories

of unsold homes, and over time provide a basis for stabilizing the housing market –

although with sales continuing to decline, the most recent readings show little or no

progress in cutting inventories relative to sales.

A potential problem for financial institutions is the interaction between falling

housing prices and homeowners’ home equity lines of credit (HELOCs

5

) and junior

liens

6

(home equity loans). As housing prices have risen over the course of this de

products have proliferated that allow consumers to tap into the wealth created by home-

price appreciation. As can be seen in Figure 2, home equity loans and HELOCs have

expanded rapidly – together they now account for over $700 billion of bank assets (which

4

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

accounts for about one-third of the $2.1 trillion in one-to-four-family mortgages held by

the nation's commercial and savings banks as of March 31, 2008).

Using home equity can be particularly attractive to consumers because of the tax

advantages of borrowing with the home as collateral, the lower interest rate on mortgage

loans relative to other forms of consumer debt, and the ability to expand the credit line

during a period of rapid appreciation in home prices.

Despite the advantages to consumers, these products are potentially risky to

lenders during periods of falling home prices. Most financial institutions will not take

possession of homes when borrowers default on their home-equity loans (junior liens),

because this would require them to assume the first mortgage. With falling housing

prices, assuming the first mortgage is not an attractive option from the lender’s

perspective. An additional complication is that default will frequently not occur until the

home equity line of credit has been fully utilized, as borrowers who are having difficulty

making payments can tap their credit line again and again. Thus, credit problems may

first appear as rising balances rather than a failure to make payments.

As Figure 3 illustrates, the delinquency rates (specifically, the share of loans 90 or

more days past due or nonaccruing) on junior liens and home equity lines are rising quite

rapidly. One should note that most banks were not lending to so-called subprime

borrowers, but nonetheless, the delinquency rate on one-to-four family mortgages just

surpassed the levels seen in the early 1990s

7

.

As noted earlier, the rapid rise in delinquencies for home equity lines and junior

liens held at banks is occurring despite an unemployment rate of about 5 percent – so,

should the unemployment rate rise and housing prices continue to fall, financial stresses

5

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

caused by the housing correction could well spread beyond the large banks involved in

complex securitizations, and the smaller banks with sizeable portfolios of construction

loans, to a larger set of financial institutions. Not surprisingly, in regions where housing

prices are falling and delinquencies are rising, we are seeing that banks are beginning to

reduce the lines of credit available to borrowers.

A second potential problem for banks is that other types of consumer debt can

suffer “collateral damage” from the difficulties in the housing sector. Regions that have

experienced falling house prices over the past year are also areas that are seeing some of

the larger increases in delinquencies on consumer loans. Banks with significant

consumer loan exposures are observing that consumer delinquencies are becoming

elevated in regions most affected by housing problems.

To date, credit problems have been focused on large financial institutions, many

of whom have shown the capacity to raise new capital. However, should the challenges

in housing continue, problems could expand beyond securitized assets to have an impact

on the nonsecuritized assets held by smaller banking institutions. It is possible that these

institutions may not be able to tap additional capital quite as easily as larger institutions,

and if so they may be forced to constrain other lending to address any losses. So I leave

you with the cautionary note that while small and medium sized businesses have not

generally experienced significant problems with credit availability to date, further

deterioration in housing markets, if it occurs, could carry over and begin to impact

lenders who serve such borrowers.

6

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

II. Length and Duration of Housing Downturns, and Other Recent Research

from the Boston Fed

New England is no stranger to falling asset values. As you no doubt know, during

the early 1990s, New England experienced a steep decline in housing prices. We at the

Boston Fed think it may be useful to compare that experience to what we have

experienced to date with falling housing prices, and we are pursuing a number of research

avenues to do that.

A new research paper by Foote, Gerardi, Goette and Willen is one example

8

. The

authors have, among other things, done extensive data analysis that allows us to compare

the current situation to that earlier episode, using publicly available data from the

Massachusetts Registry of Deeds compiled into a database by the Warren Group. I will

say more about our researchers’ findings in a moment.

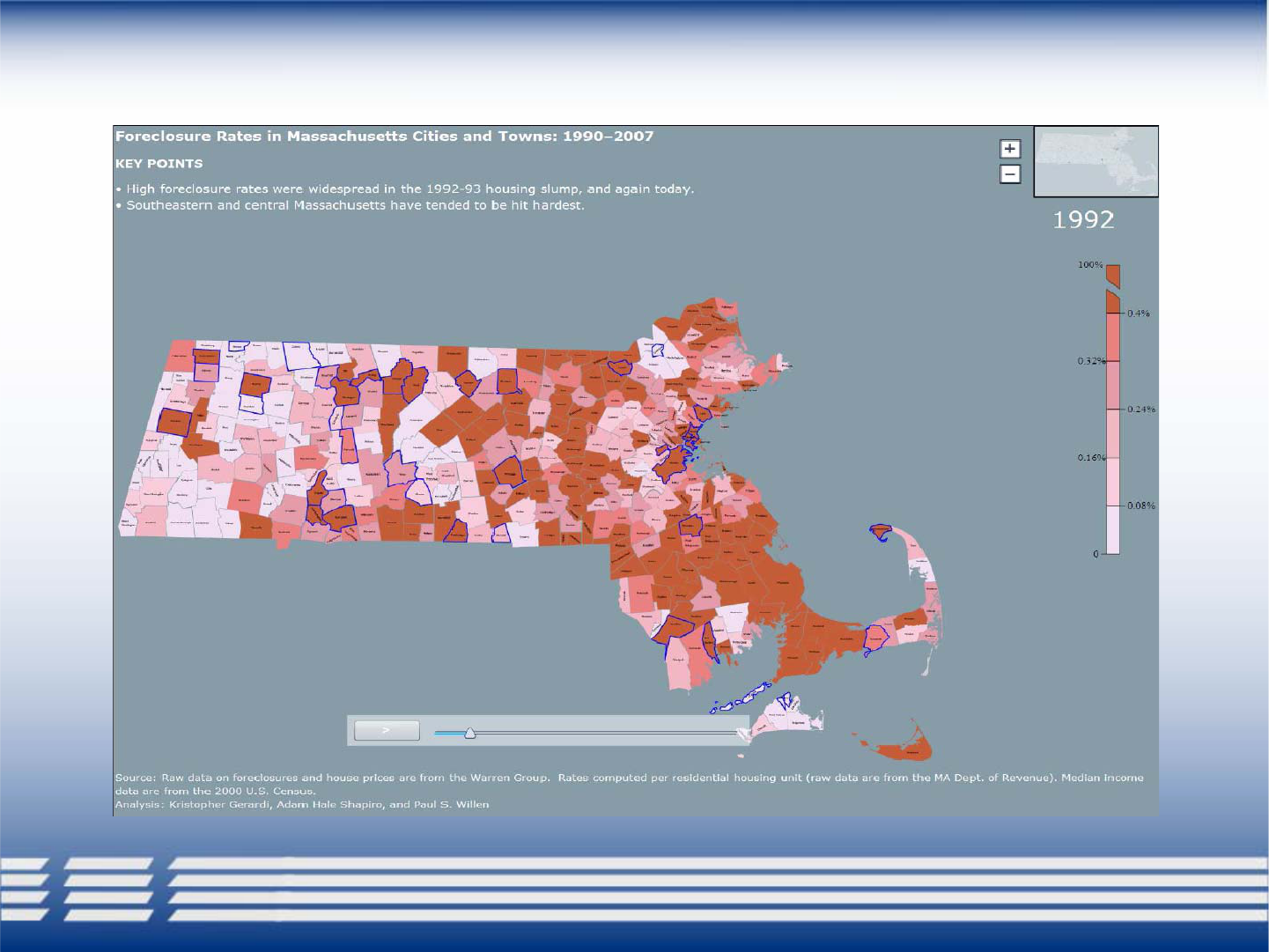

Separately, we are launching today an interactive mapping feature for our website

that tracks the rise in foreclosures and subprime activity, then and now

(http://www.bos.frb.org/subprimegraphics). The next few slides will give you a rough

sense of how it displays data -- although the site itself will show the year-by-year

progressions, dynamically, and I am going to just show you static shots of given years for

our purposes here today.

As you can see in Figure 4 and 5, Massachusetts moved quite rapidly from a

situation of relatively limited foreclosures in 1990 to a period of very high foreclosures in

1992. The timing is interesting. By late 1989, Massachusetts house prices had begun to

fall, but delinquencies and foreclosures did not really accelerate until there was also a

significant weakening of the economy. In fact, the unemployment rate in Massachusetts,

7

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

which had declined to 3.1 percent in late 1987, peaked at 9.1 percent in the second half of

1991. Declining housing prices alone did not cause very elevated foreclosures; it was

significantly compounded by an economic shock such as the loss of a job which disrupted

the ability of many borrowers to make payments. As house prices fell, many

homeowners who lost their jobs in the early-1990s recession could not sell their homes to

pay off their mortgages because they owed more than their homes were worth. For

unemployed homeowners with “negative equity,” foreclosure was often the only option.

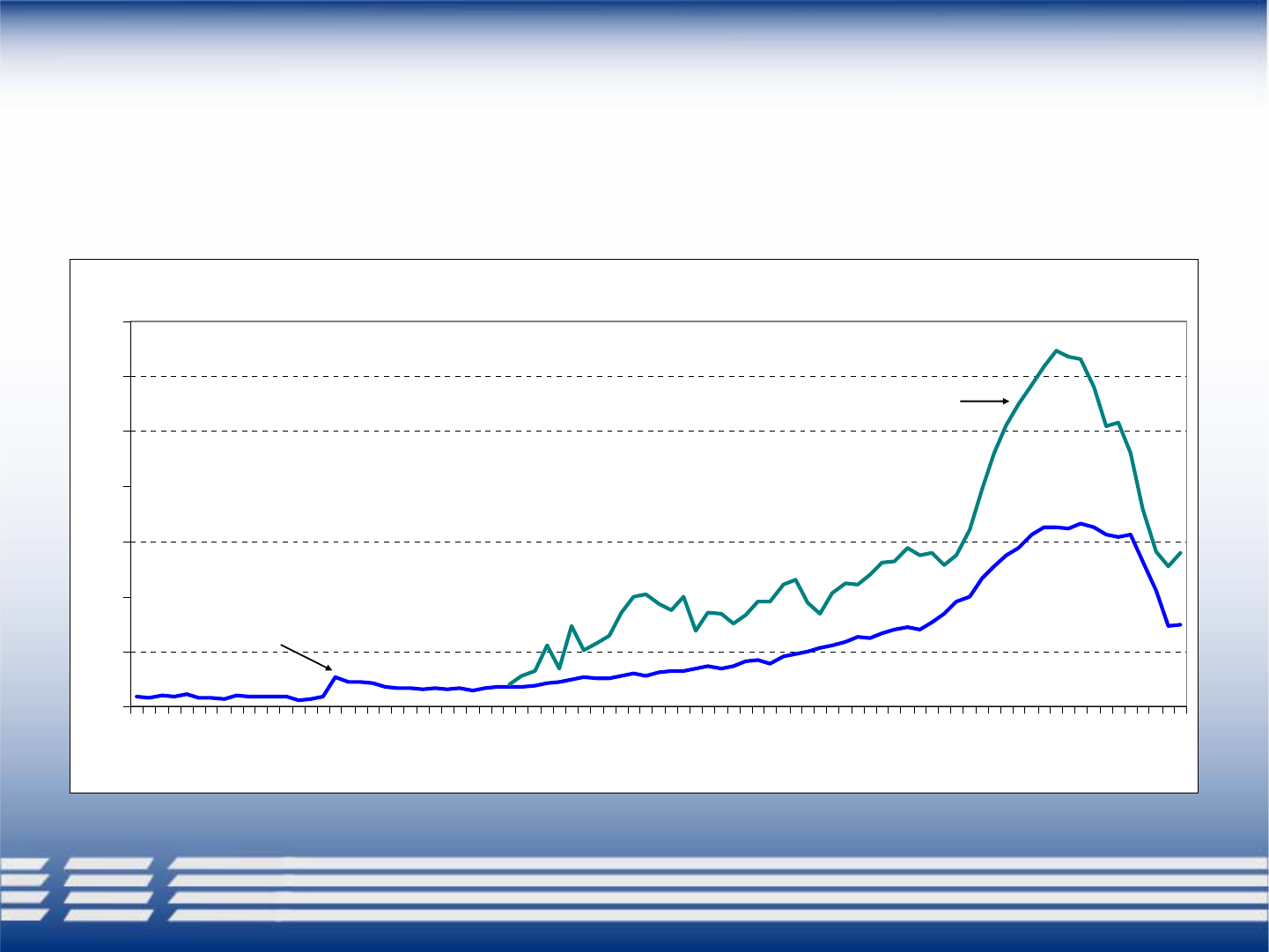

The more recent period also points to the importance of falling house prices and

negative equity in foreclosures. In the more recent period (shown in Figures 6 and 7), the

foreclosure rate – which was not particularly elevated in 2005 – had become quite

elevated by 2007 as house prices softened. This increase in foreclosures occurred even

though the Massachusetts unemployment rate averaged 4.5 percent for the year.

Why are foreclosures so high today, given that the economic situation is so much

better than it was during the early 1990s? Even in expansions, many homeowners

undergo adverse life events – like a job loss, a divorce, a spike in medical expenses, or

the like – that disrupt their ability to make mortgage payments. Of course, with regard to

unemployment, such household-level disruptions are not as prevalent in expansions as

they are in recessions. But when such a life event does occur, it can still precipitate a

foreclosure if the homeowner has negative equity because of a fall in house prices.

Another reason for elevated foreclosures today concerns changes in the

susceptibility of mortgages to economic shocks. In the late 1980s, many borrowers had

made significant down payments and had good credit histories. But the recent ability of

borrowers with weak credit histories and little or no down payments to purchase homes,

8

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

often with subprime loans (and sometimes with minimal income verification), means that

a greater share of today’s mortgages are a good bit more susceptible to the types of

disruptive life events that precipitate foreclosure. These borrowers were fine when

housing prices were rising because if needed, they had the ability to refinance or sell their

homes and pay off (or more than pay off) their mortgages. In contrast, in the current

environment of falling housing prices, borrowers who made small down-payments or

have otherwise risky mortgages are now more likely to end up in foreclosure if they

experience an adverse event that interrupts their ability to make mortgage payments.

So, in short, we have seen similar foreclosure numbers this time around without a

technical recession, and with a more modest fall in home prices. Boston Fed researchers

attribute that to the prevalence of riskier loans and higher combined loan-to-value ratios

in general.

Figures 8 and 9 provide some background on the foreclosure experience by house

type. Several interesting patterns are apparent. In the early 1990s, foreclosures rose

rapidly for all types of homes as the economy deteriorated. While foreclosures peaked in

1992, they remained quite elevated through much of the decade, despite the eventual

rebounding of the economy. In addition, that period’s speculative fervor in New England

real estate markets had a particularly large impact on the condo market, where a

disproportionate share of the foreclosures occurred.

Today, problems appear most pronounced in the multifamily market. The two-

and three-family houses that are prevalent in low- and moderate-income neighborhoods

in Massachusetts have experienced very elevated foreclosure rates. Specifically, multi-

9

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

family units accounted for 28.4 percent of the foreclosures in 2006-2007, but have

constituted only 10.8 percent of residential purchases since 1990

9

(Figure 9).

The impact on particular communities can be seen in Figure 10,

10

which shows

foreclosure petitions by property type in given cities and towns in Massachusetts. In

Boston, 47 percent of foreclosure petitions between January and August 2007 were multi-

family properties. Many of the cities with high concentrations of low- and moderate-

income borrowers have also seen particularly high rates of foreclosure petitions

11

on

multi-family properties. Our researchers suggest that one explanation for the higher

foreclosure rate on multi-family properties is found in higher combined loan to value

(CLTV) ratios, which make them more vulnerable when prices are falling.

12

States like Massachusetts and Rhode Island have a much larger concentration of

multi-family homes than do many other regions of the country

13

. Streets with a large

concentration of foreclosures in major New England cities frequently are dominated by

multi-family units. Recently both Boston and Chelsea have begun programs to purchase

foreclosed multi-family units, to try to prevent these properties from becoming vacant

and slipping into disrepair, which would bring broader collateral problems for the

affected neighborhoods.

Because many of these properties are investor owned – or the current owner

occupies one of the units and has limited financial means to deploy should the property

require major capital improvements – programs focused on owner-occupied single-family

properties will not address these problems. One area that will need focus going forward

involves strategies to prevent streets of foreclosed multi-unit properties from leading to

broader sections of urban decay.

10

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

Several lessons from the historical comparison can be highlighted. First, should

the economy worsen and suffer a period of significant job losses, the housing problem

could become much more severe. Second, past episodes of elevated foreclosures lingered

well after the peak in foreclosures had passed, indicating that the duration of today’s

situation may be longer than some are anticipating. Third, because the current problems

have been concentrated in vulnerable low- and moderate-income areas with a prevalence

of multi-unit properties, such multi-unit properties will be a more important public policy

issue in the current situation.

III. Issues Complicating the Resolution of Housing Problems

As I have noted, a major change in the U.S. housing sector in recent years has

been the emergence of the ability to buy homes with little or no down payment and the

increased prevalence of such purchases. Many of these purchases are structured with a

first loan that covers 80 percent of the value of the house and a second loan, sometimes

called a “piggyback” loan, which is taken out at the same time as the first. The

piggyback loan tends to be at a higher interest rate reflecting the greater risk of the loan,

but the interest is tax deductible and allows the borrower to avoid purchasing private

mortgage insurance (which lenders require if the borrower is paying less than 20 percent

in down payment).

As can be seen in Figure 11, until recently, an increasing percentage of homes

were being financed with these piggyback loans. In Massachusetts, piggyback loans

were used with 26 percent of subprime mortgages in the second quarter of 2003 but that

percentage increased to 65 percent of subprime mortgages in the third quarter of 2005.

11

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

Piggyback loans were about twice as prevalent for subprime borrowers as prime

borrowers, and were particularly prevalent in multi-family purchases. In fact, 75 percent

of subprime multi-family purchases in the third quarter of 2005 involved a piggyback

loan.

At the time of purchase, subprime borrowers frequently used the same lender to

acquire both the first loan and the piggyback loan. The complicating factor is that these

loans were frequently then securitized, with the first mortgage and the piggyback loan

often sold into separate portfolios of loans to be securitized. Thus, even while piggyback

loans were becoming more abundant, many mortgage-backed securities contained no

piggyback loans, implying that the borrower’s loans were frequently packaged in separate

securitizations.

The combination of piggyback loans, securitization, and legal complexities makes

it much more difficult to modify loans, particularly if the first and second mortgages have

been packaged into separate securitizations. Dealing with two different lenders or

servicers, as well as different securitizations, can significantly complicate efforts to

restructure loans. Also, loan servicing agreements are not identical and indeed include a

variety of forms of authorization (of the servicer) to modify loans. Frequently the only

leverage the owner of the piggyback loan can and does exercise with a distressed

borrower is demanding compensation should the borrower seek to modify both loans.

In short, while a variety of programs and policies are being considered in order to

improve the loan modification process for distressed borrowers and their lenders, a key

consideration involves figuring out how to modify loans when the interests of the primary

loan holder may be different than those of the holder of the piggyback loan.

12

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

A second complication involves targeting the modifications to the homeowners

who really need them. We have seen that falling house prices tend to raise foreclosures

by causing a negative equity situation which limits homeowners’ options (e.g., to

refinance or sell and pay off the loan) if their financial situation deteriorates.

The rising share of homeowners with negative equity in their house – meaning

their home is now worth less than their loan(s) – might seem to suggest a large group for

whom loan modifications would be a “slam dunk.” Principal write-downs to bring

“underwater” mortgages above water may well be the appropriate solution for some

troubled borrowers

14

, but lenders and loan servicers continue to be reluctant to provide

modifications in a wholesale manner. Negative equity does not imply foreclosure with

certainty – in fact, most people with negative equity situations continue to make their

mortgage payments. Lenders and loan servicers who are aware of this fact may be

reluctant to offer a modification if they believe that the homeowner has the capacity to

continue making payments, no matter the hardship.

To “unpack” this a bit, I want to spend a moment looking at the history of

negative-equity borrowers over the past two decades, drawing on a new working paper

just produced by Boston Fed researchers

15

.

In the late 1980s, house-price declines in New England meant a large number of

borrowers had negative equity in their house. The Registry of Deeds data allow us to

study the historical relationship between negative equity and foreclosures for a limited set

of borrowers – specifically, people who purchased homes in Massachusetts on or after

January 1987, when the Warren Group data begin. Using these data to calculate a rough

proxy for housing equity, Foote, Gerardi and Willen calculate that 100,288 of these post-

13

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

1987 purchasers, or 36 percent, were in a position of negative equity as of the fourth

quarter of 1991 (a high fraction because January 1987 came just before the peak of the

housing cycle).

16

Yet of this negative-equity group, only 6,453 (or just 6.4 percent)

defaulted on their mortgages within the following three years.

What about today? Using the same rough method to approximate home equity for

the same subset of homeowners, the data imply that about 10 percent of post-1987

purchasers were in a position of negative equity as of the fourth quarter of 2007.

Assuming that the unemployment rate and benchmark interest rate (the 6-month London

Interbank Offered Rate or LIBOR) stay at their fourth-quarter 2007 levels, the statistical

default model of Gerardi, Shapiro and Willen predicts that less than 10 percent of these

homeowners with negative equity will default.

Continued declines in house prices, higher unemployment, and possibly a greater

willingness to default on home mortgages might raise this estimate of future defaults.

Even so, many lenders will not be inclined to make concessions unless borrowers clearly

lack the ability to pay. This is one reason that workouts or distressed borrowers’

mortgages continue to proceed loan by loan, rather than through wholesale changes in

mortgage terms. Lenders want borrowers with the capacity to pay to continue to uphold

their legal obligation to do so – and any wholesale change in mortgage terms could

benefit borrowers that are still able to fulfill the original agreement. To avoid this

problem, some policy proposals

17

maintain the legal obligation for the full loan for the

borrower, but involve significantly reduced payments in return for the lender sharing in

any future appreciation of the house.

14

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

Another impediment to restructuring loans that have been packaged into

securitizations involves the legal restrictions imposed on many securitization

agreements

18

. These agreements allow the servicer to pass through payments by

borrowers without incurring any tax liability, as long as certain conditions are met. One

of the conditions is usually that modifications cannot be made to the loans unless the loan

is either in default or default is reasonably foreseeable. This determination is generally

made loan by loan, with wholesale modifications being interpreted by some servicers as

possibly violating the service agreement and the legal framework used in many

securitizations and thus potentially imposing tax liability.

Despite some promising proposals, these factors – the presence of piggyback

loans, the desire of lenders to continue to get paid unless the borrower does not have the

capacity to make payments, and the legal restrictions and tax-liability concerns

surrounding securitization agreements – make any across-the-board modification of loan

terms challenging.

As long as loan modifications are taking place on a loan-by-loan basis (a time-

consuming and labor-intensive process), to significantly increase the number of loan

modifications and avoid significant numbers of foreclosures, many servicers will need to

quickly expand the pool of staff capable of making these evaluations.

IV. Implications for Policymakers

To reiterate, falling housing prices continue to be a significant source of down-

side risk to the economy. Previous periods of real estate problems have taken significant

time to be worked out, with foreclosures remaining elevated well after their peak. The

15

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

current foreclosure problem has been exacerbated by the difficulties related to many of

the problem loans being held in securities.

To help mitigate the current situation it is important for servicers to have the

capacity and the incentive to make loan modifications where appropriate. A challenge

continues to arise around getting borrowers and servicers together to determine if loan

modifications are appropriate.

In addition, it is clear that servicers were not set up for the spate of elevated

foreclosures we have already experienced, and further increases in foreclosures would

certainly test the capacity of servicers to have sufficient staff with the expertise to make

loan modification determinations. Nonetheless, I am hopeful that the many mortgage

forums that are being organized around the country to try to get servicers and borrowers

together to work with problem loans will help some borrowers.

The large number of multi-family dwellings entering foreclosure presents a

serious challenge to cities. Already there are streets in some cities with a high

concentration of foreclosed multi-family properties, putting at risk many of the

socioeconomic advances made in the last decade in some of these neighborhoods. Cities,

working together and with community organizations and state officials,

19

will need to

find ways to make sure these low- and moderate-income neighborhoods do not regress as

a result of the current wave of foreclosures. One promising tactic is rigorous municipal-

code enforcement that ensures foreclosed properties are maintained. Furthermore,

servicers must have a process for maintaining foreclosed properties and they must do

more to ensure that these properties do not remain vacant for long periods of time.

16

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

17

Finally, the legal structure for securitizations and mortgage-servicing agreements

clearly did not foresee the widespread emergence of distressed borrowers, delinquencies,

and foreclosures that are being experienced. Changes to servicing agreements and

securitization structures that allow more flexibility during times of duress and also

address servicers’ liability concerns are necessary. Since different investors in a

mortgage-backed security have different incentives, more clearly defining the governance

of these securities would make it easier during difficult times to make modifications that

are in the borrower’s, servicer’s, and investor’s interests.

The extent of eventual housing problems is highly dependent on the outlook for

the economy and the future path of housing prices. Fortunately, aggressive monetary and

fiscal policy actions have been taken to help mitigate some of the downside risk. These

policies will likely result in some pick up in economic activity in the second half of this

year, which should help to stabilize the housing market.

NOTES:

1

Of course, the views I express today are my own, not necessarily those of my

colleagues on the Board of Governors or the Federal Open Market Committee (the

FOMC).

2

A comprehensive description of the Bear Stearns situation is available in “Actions

by the New York Fed in Response to Liquidity Pressures in Financial Markets” –

Testimony before the U.S. Senate Committee on Banking, Housing and Urban Affairs by

Timothy F. Geithner, President and Chief Executive Officer of the Federal Reserve Bank

of New York (April 3, 2008).

3

GDP is essentially the value of goods and services put in place during a time

period, and residential investment is the housing component of GDP. “The main

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

18

indicator of the quantity of new housing supplied to the economy is the residential fixed

investment series from the national income and product accounts. Residential investment

is made up of new construction put in place, expenditures on maintenance and home

improvement, equipment purchased for use in residential structures (e.g., washers and

dryers purchased by landlords and rented out to tenants), and brokerage commissions.”

(Source: “Residential Investment over the Real Estate Cycle” by John Krainer, in the

Federal Reserve Bank of San Francisco’s Economic Letter #2006-15; June 30, 2006).

"Brokers’ commissions…are part of the cost of acquiring a house and, therefore, a capital

expenditure." (Source: "National and Regional Housing Patterns" by Lynn Elaine

Browne in the New England Economic Review, July/August 2000, published by the

Federal Reserve Bank of Boston).

4

In essence “subprime” loans refer to mortgages that have a higher risk of default

than prime loans, often because of the borrowers’ credit history. Certain lenders

specialize in subprime loans, which carry higher interest rates reflecting the higher risk.

Certain lenders, typically mortgage banks, may specialize in subprime loans. Banks,

especially smaller community banks, generally do not make subprime loans, although a

few large banking organizations are active through mortgage banking subsidiaries.

According to interagency guidance issued, in 2001, “The term ‘subprime’ refers

to the credit characteristics of individual borrowers. Subprime borrowers typically have

weakened credit histories that include payment delinquencies and possibly more severe

problems such as charge-offs, judgments, and bankruptcies. They may also display

reduced repayment capacity as measured by credit scores, debt-to-income ratios, or other

criteria that may encompass borrowers with incomplete credit histories. Subprime loans

are loans to borrowers displaying one or more of these characteristics at the time of

origination or purchase. Such loans have a higher risk of default than loans to prime

borrowers. Generally, subprime borrowers will display a range of credit risk

characteristics that may include one or more of the following: Two or more 30-day

delinquencies in the last 12 months, or one or more 60-day delinquencies in the last 24

months; Judgment, foreclosure, repossession, or charge-off in the prior 24 months;

Bankruptcy in the last 5 years; Relatively high default probability as evidenced by, for

example, a credit bureau risk score (FICO) of 660 or below (depending on the

product/collateral), or other bureau or proprietary scores with an equivalent default

probability likelihood; and/or Debt service-to-income ratio of 50 percent or greater, or

otherwise limited ability to cover family living expenses after deducting total monthly

debt-service requirements from monthly income.”

5

The amount outstanding of revolving, open-ended loans secured by 1-4 family

residential properties and extended under lines of credit.

6

Closed-end loans secured by junior (i.e., other than first) liens on 1-4 family

residential properties.

7

Delinquencies on first mortgage loans and junior liens were not reported

separately by banks until 2002.

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

19

8

“Subprime Facts: What (we think) we know about the subprime crisis and what

we don’t” by Christopher Foote, Lorenz Goette, Paul Willen, and Kristopher Gerardi

(forthcoming).

9

During the earlier wave of foreclosures in 1991 and 1992, multi-family residences

accounted for 20.4 percent of foreclosures.

10

From Kai-Yan Lee, forthcoming Boston Fed Public and Community Affairs

Discussion Paper.

11

Foreclosure petitions differ from foreclosure deeds.

12

Also, investors make up 16 percent of subprime borrowers who purchased or re-

financed multifamily structures, compared to only 2.3 percent of those who purchased

single family homes and 6.3 percent of condos being financed by investors.

13

According to the 2000 Census of Housing, 9.1 percent of housing units were

in 2- to 4-unit buildings Rhode Island has the most multi-family units (25.2%) while for

Massachusetts had 23.0% multi-family units. A table that provides the composition of

housing units by state can be found at

http://www.census.gov/hhes/www/housing/census/historic/units.html

14

Federal Reserve Board Chairman Ben Bernanke is one of a number of

policymakers urging lenders to consider principal writedowns, for example in speeches

given on March 4 and May 5

(http://www.federalreserve.gov/newsevents/speech/bernanke20080304a.htm and

http://www.federalreserve.gov/newsevents/speech/Bernanke20080505a.htm).

15

“Negative Equity and Foreclosure: Theory and Evidence” by Paul S. Willen,

Kristopher Gerardi, and Chris Foote (forthcoming).

16

For this calculation, equity is estimated as the sum of initial equity at purchase

(that is, the downpayment) plus an estimate of cumulative house price appreciation for

that particular home. This estimate is a rough measure for two reasons. First, the data do

not allow an estimate of the principal that has been paid down during the life of the

mortgage. Second, there is no allowance for cash-out refinancing or other types of equity

withdrawal. The first of these influences would cause the estimate of home equity to be

too small, while the second would cause the equity estimate to be too large. It is unclear

which factor is quantitatively more important.

17

Such as the proposed “Appreciating America” approach, which would have the

following characteristics (see Refinance.com):

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

20

The homeowner would refinance the outstanding mortgage(s) with an approved

"Appreciating America Lender," in accordance with established FHA guidelines (i.e.

with respect to loan to value and debt to income ratios).

The first mortgage would be set at some percentage of the current market value of the

home (e.g., 85 percent) and would be insured by FHA.

A second mortgage would be formed to cover the difference between the original

mortgage balance and the FHA-insured new mortgage, and would be held by the

current mortgage servicer. Payments and interest (6 percent) on this new second

mortgage would be deferred for five years or until the home is sold (whichever comes

first).

To the extent that the value of the home at that point is greater than the FHA first

mortgage amount, the homeowner would first receive an amount equal to all capital

improvements made to the property since the Appreciating America Mortgage closed;

then the homeowner would receive 30 percent of the appreciation, and the second

mortgage holder would receive the lesser of 70 percent of the appreciation or the

principal and accrued interest on the Appreciating America Second Mortgage. All

appreciation in excess of the second mortgage balance including accrued interest

would belong to the homeowner.

18

The legal vehicle used for securitized mortgages is a Real Estate Mortgage

Investment Conduit (REMIC), which is a pass-through tax entity and investment vehicle

that holds a pool of commercial and residential mortgages in trust and issues securities

(often in multiple classes based on maturity and risk) that represent an undivided interest

in those mortgages. Major issuers of REMICs include the Federal Home Loan Mortgage

Company (Freddie Mac) and the Federal National Mortgage Association (Fannie Mae).

REMICs are governed by the sections 860A through 860G of the Internal Revenue Code.

In order to qualify as a REMIC, all of the interests must consist of one or more classes of

regular interest and one (only one) class of residual interest.

An entity that initially qualifies as a REMIC may cease to qualify if a sufficiently

large portion of its qualified mortgages are “significantly modified” and the modified

obligations are not qualified mortgages. A qualified mortgage is usually treated as having

been significantly modified if the change in terms would be treated as an exchange of

obligations under section 1001 and its regulations. However, certain changes to the terms

of an obligation are not considered signification modifications for this purpose,

notwithstanding the fact that they may be significant modifications under section 1001

and § 1.1001-3. The four permitted modifications are (1) Changes in the terms of the

obligation occasioned by default or a reasonably foreseeable default; (2) Assumption of

the obligation; (3) Waiver of a due-on-sale clause or a due on encumbrance clause; and

(4) Conversion of an interest rate by a mortgagor pursuant to the terms of a convertible

mortgage.

As echoed in many Servicing Agreements, the most pertinent modification is one

induced by either default or impending default. The problem lies in ascertaining with

some certainty whether default is “reasonably foreseeable” and thus servicers have been

reticent to go forward with modifications based on this shaky standard when the potential

consequences are so dire.

EMBARGOED until Friday, May 30, 2008,

12:45 P.M. Eastern Time or upon delivery

21

19

In Massachusetts, two separate task forces organized by the Division of Banks

and by community groups have been grappling with neighborhood stabilization. They

have both brought together community groups, cities, quasi-governmental and state

agencies.

Figure 1

Continuous Declines of Three Quarters or More in

Single-Family Housing Starts

Number of

Quarters

2006:Q2 - 2008:Q1 8 -58.4

1959:Q4 - 1960:Q4 5 -27.2

1969:Q1 - 1970:Q1 5 -25.0

1979:Q3 - 1980:Q2* 4 -46.6

1981:Q1 - 1981:Q4* 4 -44.7

1966:Q1 - 1966:Q4 4 -36.1

1990:Q2 - 1991:Q1 4 -33.5

1994:Q3 - 1995:Q2 4 -16.0

1973:Q2 - 1973:Q4* 3 -31.3

1974:Q3 - 1975:Q1* 3 -23.9

2000:Q1 - 2000:Q3 3 -10.9

*Declines interrupted by just two quarters of growth in single-family housing starts.

Dates

Cumulative

Decline

(

%

)

Source: Census Bureau / Haver Analytics

1959:Q2 - 2008:Q1

Figure 2

Home Equity Lending at

Commercial and Savings Banks

Source: Commercial and Savings Bank Call Reports

1991:Q1 - 2008:Q1

0

200

400

600

800

91:Q1 93:Q1 95:Q1 97:Q1 99:Q1 01:Q1 03:Q1 05:Q1 07:Q1

Home Equity Loans

Home Equity Lines of Credit (Amount Drawn)

Billion Dollars

Figure 3

Delinquency Rates on 1-4 Family Mortgage

Loans at Commercial and Savings Banks

1991:Q1 - 2008:Q1

0.0

0.5

1.0

1.5

2.0

2.5

91:Q1 93:Q1 95:Q1 97:Q1 99:Q1 01:Q1 03:Q1 05:Q1 07:Q1

Note: Delinquent loans include loans 90 or more days past due and loans in nonaccrual status.

Delinquencies on first mortgage loans and home equity loans were first reported separately in 2002.

1-4 Family Mortgage Loans (Aggregate)

First Mortgage Loans

Home Equity Loans

Home Equity Lines of Credit

Percent Delinquent

Source: Commercial and Savings Bank Call Reports

Figure 4

Figure 5

Figure 6

Figure 7

Figure 8

Foreclosures in Massachusetts by House Type

Source: The Warren Group

1990:Q1 - 2008:Q1

0

400

800

1,200

1,600

90:Q1 92:Q1 94:Q1 96:Q1 98:Q1 00:Q1 02:Q1 04:Q1 06:Q1 08:Q1

Foreclosures

Single-FamilyCondo

Multi-Family

Figure 9

Massachusetts Home Purchases by House Type

1987 - 2008:Q1

Source: The Warren Group

0

20

40

60

80

100

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007

Percent of Total

Single-Family

Condo

Multi-Family

2008:Q1

Figure 10

Foreclosure Petitions by Property Type

(Jan-Aug 2007, includes towns with 60+ foreclosure petitions in this period)

Source: The Warren Group

0

200

400

600

800

1,000

1,200

1,400

1,600

Boston

Springfield

Worcester

Brockton

Lynn

Lawrence

Lowell

New Bedford

Revere

Fitchburg

Haverhill

Fall River

Taunton

Quincy

Malden

Attleboro

Everett

Methuen

Peabody

Chelsea

Chicopee

Salem

Leominster

Medford

Somerville

Holyoke

Pittsfield

Multi-Family

Single-Family and Condo

47%

39%

35%

31%

47%

67%

Percentages are proportion of foreclosure

petitions involving multi-family properties.

Figure 11

Percentage of Purchase Mortgages with Piggyback

1987:Q1 - 2008:Q1

Source: The Warren Group

0

10

20

30

40

50

60

70

87:Q1 89:Q1 91:Q1 93:Q1 95:Q1 97:Q1 99:Q1 01:Q1 03:Q1 05:Q1 07:Q1

Percent

Subprime Purchase Mortgages

Prime Purchase Mortgages