No. 19–11

Technological Innovation in Mortgage Underwriting

and the Growth in Credit, 1985–2015

Christopher L. Foote, Lara Loewenstein, and Paul S. Willen

Abstract:

The application of information technology to finance, or “fintech,” is expected to revolutionize many

aspects of borrowing and lending in the future, but technology has been reshaping consumer and mortgage

lending for many years. During the 1990s, computerization allowed mortgage lenders to reduce loan-

processing times and largely replace human-based assessments of credit risk with default predictions

generated by sophisticated empirical models. Debt-to-income ratios at origination add little to the

predictive power of these models, so the new automated underwriting systems allowed higher debt-to-

income ratios than previous underwriting guidelines would have allowed. In this way, technology brought

about an exogenous change in lending standards that was especially relevant for borrowers with low current

incomes relative to their expected future incomes—in particular, young college graduates. By contrast, the

data suggest that the credit expansion during the 2000s housing boom was an endogenous response to

widespread expectations of higher future house prices, as average mortgage sizes rose for borrowers across

the entire income distribution.

Keywords: mortgage underwriting, housing cycle, technological change, credit boom

JEL Classifications: C55, D53, G21, L85, R21, R31

Christopher L. Foote is a senior economist and policy advisor in the research department at the Federal Reserve Bank

of Boston. His email address is chris.foote@bos.frb.org

. Lara Loewenstein is an economist in the research department

at the Federal Reserve Bank of Cleveland. Her email address is lara.loewenstein@clev.frb.org. Paul S. Willen is a

senior economist and policy advisor in the research department at the Federal Reserve Bank of Boston. His email

address is

paul.willen@bos.frb.org.

We thank Ben Couillard and Ryan Kessler for excellent research assistance. For helpful comments we thank (without

implicating) Ted Durant, Benjamin Keys, Robert Armstrong Montgomery, Elizabeth Murry, Ed Pinto, Eric Zwick,

and seminar participants at the Federal Reserve Bank of Cleveland, Freddie Mac, Northwestern University, the 2018

AREUEA Mid-Year Conference, the Southern Finance Association’s 2017 annual conference, the 2018 Federal

Reserve Day-Ahead Conference on Financial Markets and Institutions, and the conference on Financial Stability

Implications of New Technology at the Federal Reserve Bank of Atlanta. Robert Avery also kindly supplied data.

Any errors remain our responsibility.

This paper presents preliminary analysis and results intended to stimulate discussion and critical comment. The views

expressed herein are those of the authors and do not indicate concurrence by the Federal Reserve Bank of Boston, the

Federal Reserve Bank of Cleveland, by the principals of the Board of Governors, or the Federal Reserve System.

This paper, which may be revised, is available on the web site of the Federal Reserve Bank of Boston at

http://www.bostonfed.org/economic/wp/index.htm

.

This version: November, 2019

https://doi.org/10.29412/res.wp.2019.11

At first glance, Louise Beyler of Gainesville, GA, might appear as an unlikely

candidate for a mortgage to buy a $105,500 home. Self-employed and earning

$19,000 a year, Beyler would have to spend nearly 45 percent of her income to

cover the mortgage payments. Given her circumstances, many lenders would

deny Beyler a mortgage. Thanks to automated underwriting, however, Beyler’s

application was approved—in just three days.

—from Peter E. Mahoney and Peter M. Zorn

“The Promise of Automated Underwriting,” (1996), p. 18.

1 Introduction

This paper studies the relationship between borrower income and mortgage debt during

the past three decades. Better-off people tend to have larger homes and take out larger

mortgages to pay for them, so there is a positive relationship between average mortgage

sizes and household income in the data. This cross-sectional pattern is also influenced by

lenders’ underwriting policies: if these policies are exogenously relaxed, so that low-income

households are able to take out larger loans, then the positive cross-sectional relationship

between debt and income will flatten. Researchers are now debating whether an exogenous

loosening of lending standards took place during the 2000s housing boom, and the main

way they have studied this possibility is by measuring changes in the slope of the debt-

income relationship. Unfortunately, progress in this area has been hindered by data-quality

concerns. In this paper, we make some important adjustments to the data previously used

in this literature, and we also develop a new data source that is well-suited to study the

relationship between income and mortgage debt. These data allow us to resolve the debate

over the debt-income relationship during the housing boom. Additionally, because our data

encompass several years before the boom, we can shed light on how changes in financial

technology, or “fintech,” had already transformed the debt-income relationship before the

boom began, in ways that remain relevant for borrowers and lenders today.

An important early paper on the debt-income relationship is Mian and Sufi (2009), which

used data from the Home Mortgage Disclosure Act (HMDA) to claim that mortgage credit

rose disproportionately for low-income borrowers during the 2000s boom. A central finding

of that paper is that the total dollar value of mortgage originations rose disproportionately in

low-income zip codes during the boom. Adelino, Schoar, and Severino (2016) extended this

analysis by splitting the value of mortgage originations into two components: the average

size of each mortgage in a zip code and the total number of mortgages originated there. This

decomposition revealed that Mian and Sufi’s headline finding resulted from a relative increase

1

in the number of mortgages originated in low-income areas, not by a relative increase in the

average size of new mortgages in those areas. This finding undermined Mian and Sufi’s claim

that looser income requirements on the part of lenders drove the housing boom. Mian and

Sufi (2017) responded by raising concerns with the way that Adelino and his co-authors used

the HMDA data, especially their treatment of second liens and their use of borrower-income

data from HMDA, which can be overstated. Our paper addresses these two concerns, and

finds that in practice they are not strong enough to overturn Adelino, Schoar, and Severino’s

main claim: the average size of new mortgages did rise proportionately across the income

distribution during the housing boom. Along with other research highlighting the broad-

based nature of the boom, the proportionate increase in average mortgage sizes suggests that

the housing boom resulted from excessive optimism about future house price appreciation,

not from exogenous changes in underwriting requirements.

1

We also find, however, that the relationship between debt and income did flatten in the

1990s, a period that is recognized as one of intense technological change in mortgage lending

(LaCour-Little 2000; Bogdon 2000; Colton 2002). Below we show that computer technology

allowed mortgage lenders to process loans much more quickly at the end of the 1990s than at

the beginning of the decade. But technology did more than speed up mortgage processing: it

fundamentally transformed it by replacing human evaluation of credit risk with predictions

from data-driven models. Before 1990, loan officers and originators evaluated mortgage

applications by personally applying so-called knockout rules, which specified maximal cutoffs

for variables such as the LTV (loan-to-value) ratio and the DTI (debt-to-income) ratio.

2

This

type of rules-based system would seem to be tailor-made for replacement by computers, which

have transformed the US economy due to their ability to perform routine tasks efficiently

(Levy and Murnane 2004; Acemoglu and Autor 2011). In fact, during the early 1990s many

mortgage lenders tried to use computers in precisely this way, by encoding their lending rules

into formal algorithms that computers could follow. The resulting artificial intelligence (AI)

systems would then be expected to evaluate loan applications in the same way that humans

had, but at a lower cost.

The coders soon discovered that despite the rules-based nature of loan-evaluation pro-

1

As we discuss in Section 4, HMDA covers only mortgage originations, not terminations. Consequently,

HMDA data cannot be used to study a credit expansion along the extensive margin; that is, an increase

in the number of persons approved for new mortgages. Related to this, HMDA’s coverage of only one flow

of debt (originations) means that the HMDA data cannot measure changes in stocks of mortgage debt. As

discussed below, Foote, Loewenstein, and Willen (2019) uses data from the Equifax credit bureau and the

Survey of Consumer Finances to show that—consistent with the proportionate increase in average mortgage

sizes highlighted here—there were no significant cross-sectional differences in debt accumulation along the

extensive margin. Stocks of debt rose proportionately across the income distribution as well.

2

For mortgage lenders, the DTI ratio denotes the ratio of the borrower’s monthly payment to her monthly

income, and does not involve the borrower’s entire stock of debt. Although it is not quite accurate, this DTI

definition is so ingrained in the mortgage industry that we stick with it here.

2

cedures, intuitive human judgment typically came into play. Making decisions was easy

for human underwriters when loan applications cleared all of the relevant hurdles. But for

marginal cases the underwriters had to use their own experience and judgment. Could a

high DTI ratio in a particular loan application be safely offset by a low LTV ratio, or by the

applicant having a particularly strong credit history? The developers of one early AI system

wrote that:

Underwriting is considered an art that is taught from one generation of under-

writers to the next. It takes years of experience to learn to judge and evaluate

the loan information to make an informed decision on the risk of the loan. Un-

derwriters do not follow a systematic, step-by-step approach to evaluate a loan.

Instead, the underwriter must look at the strengths and weaknesses of the indi-

vidual elements in a loan file and evaluate how all the data elements affect one

another. The process is intuitive rather than scientific. The challenge for the

knowledge engineers was to represent the thought process of an underwriter in

a manner that could be implemented as a software system (Talebzadeh, Mandu-

tianu, and Winner 1995, pp. 54–55).

Even if human thought processes could be codified into computer algorithms, a big problem

with basing lending decisions on human judgment is that mortgage defaults are rare. Indi-

vidual underwriters were therefore unlikely to accumulate enough personal experience with

defaults to properly quantify the tradeoffs among the various risk characteristics that were

associated with a mortgage application.

Other firms in the mortgage industry used computers differently. They pulled together

large datasets of loan-level records and estimated empirical models of mortgage default, which

could then be used to augment the underwriters’ evaluations of loan files. The modelers soon

realized that default predictions could be significantly enhanced by using consumer credit

scores, such as the FICO score, which had been developed to predict defaults on unsecured

loans. As credit scores worked their way into mortgage-lending decisions, the housing-finance

industry was transformed by the same technologies that at the same time were revolutionizing

the credit-card industry and other forms of consumer lending (Evans and Schmalensee 2005;

Einav, Jenkins, and Levin 2013; Livshits, MacGee, and Tertilt 2016).

Unlike credit scores, DTI ratios added little to the new mortgage models. As we explain

below, modern theories of mortgage default—which are based on income shocks rather than

initial income levels—are consistent with this lack of predictive power. Indeed, the small

effect that DTI ratios have on default probabilities was foreshadowed by previous, smaller-

scale empirical studies, including those in Home Mortgage Delinquency and Foreclosure,

the ur-study of loan-level default sponsored by the National Bureau of Economic Research

in the late 1960s (Herzog and Earley 1970). In the 1990s, however, the unimportance of

3

DTIs began to influence the allocation of mortgage credit. Informed by their new computer-

driven empirical models, mortgage lenders discounted the relationship between a borrower’s

income and her mortgage obligation by approving larger loans at the lower end of the income

distribution.

By and large, we find that the effects of these exogenous changes on lending patterns

are consistent with economic theory. Relaxing DTI limits should have the largest effects on

individuals whose expected future incomes are high relative to their current incomes. Young

college graduates have relatively steep age-earnings profiles, and we find that the increase in

homeownership after 1994 was particularly large for this group.

Putting the pieces together, the technological changes of the 1990s were exogenous with

respect to the state of the US housing market—these innovations stemmed from increases in

computing power and better data-storage and modeling capabilities, not because the housing

market was particularly hot or cold during that decade. Consequently, the 1990s changes in

mortgage-lending standards flattened the empirical relationship between debt and income,

as borrowers with steeply rising income profiles took advantage of the looser requirements on

current income, and borrowers who were not previously constrained were unaffected by the

changes. In the 2000s, however, the average sizes of new mortgages rose across the income

distribution, a pattern that is consistent with widespread optimism concerning future house

price growth. Such optimism would increase housing demand for borrowers at all income

levels. It would also promote an endogenous loosening of lending constraints that allowed

low-income borrowers to expand mortgage borrowing at the same rate as their higher-income

counterparts.

The rest of the paper is organized as follows. Section 2 discusses the two main data

sources that we use to study the debt-income relationship over time, and section 3 presents

our results. We relate these findings to the current debate on lending standards during the

boom in section 4, and we explain how patterns in the 1990s related to technical change in

section 5. Section 6 traces out the effects of the technical changes on the mortgage market,

and section 7 concludes.

2 Data

2.1 The Home Mortgage Disclosure Act (HMDA)

Our first dataset comes from HMDA, a 1975 law that requires US financial institutions in

metropolitan areas to report individual-level information relating to mortgage applications

and originations. Variables in the public-use version of HMDA include the dollar amount of

each new mortgage; the reported income, race, and gender of the borrower; and the Census

4

tract of the house that serves as collateral for the loan.

Some information is not available in HMDA on a consistent basis because of changes

in reporting guidelines, including some relatively major changes that occurred in 2004.

3

For example, starting in 2004 we can distinguish between first and second liens. During

the 2000s housing boom, first-lien mortgages were often supplemented by second liens at

purchase (“piggyback loans”), so it is important to account for second liens consistently

when making comparisons that span several years. We therefore created an algorithm to

identify second liens made before 2004, and then validated this rule using the reported liens

available starting in 2004. The algorithm makes use of the application and origination dates

of each mortgage, which are available only in a confidential version of the HMDA data to

which we gained access.

4

Even when second liens are identified in HMDA, they are not

matched to their corresponding first liens. Our algorithm both identifies second liens and

matches them to their first liens. We then use the sum total of the first and second liens for

each borrower in our loan-level regressions.

The HMDA data also include a field that distinguishes owner-occupied properties from

investment properties.

5

In the main empirical work below, we remove investors from our

regressions, largely because the relationship between income and mortgage size for investors

is likely to be very different than it is for owner-occupiers. For investment properties, the

income backing a mortgage comes not only from the borrower’s resources, but also from the

rental income that the property is expected to generate.

We then clean the HMDA data along the lines suggested by Avery, Brevoort, and Canner

(2007), who recommend that analysts drop loans that lack information on race and gender

(as these are probably business loans) and combine home improvement loans with refinances.

Additionally, because miscoded outliers can exert a strong effect in our debt-income analysis,

we remove outliers with an algorithm designed to detect inaccurate loan or income entries.

The algorithm calculates the implied monthly payment of each loan (assuming that it is

a 30-year fixed-rate mortgage at the current interest rate), and then divides this implied

payment by the borrower’s income as reported on the HMDA record to generate an implied

DTI ratio. We then drop loans with DTI ratios in the bottom and top 1 percent of this

distribution.

Figure 1 depicts some summary statistics from data on purchase-mortgage originations

in HMDA. The top panel shows the total number of purchase loans originated, along with

3

A good summary of these changes can be found in “HMDA Changes Are On the Way; New Rules

Take Effect in 2004," which appears in Community Dividend, an online publication of the Federal Reserve

Bank of Minneapolis. It is available at https://www.minneapolisfed.org/publications/community-dividend/

hmda-changes-are-on-the-way-new-rules-take-effect-in-2004.

4

Details of the second-liens algorithm appear in Appendix A.1.

5

This field is based on information supplied by the borrower, so someone purchasing an investment

property might intentionally misreport as an owner-occupier in order to get a lower mortgage rate.

5

the fraction of those loans that have associated second liens. The number of purchase

loans originated increases steadily from 1990 until 2005, while the use of piggyback loans

grows dramatically in the mid-2000s, near the end of the housing boom. After 2007, both

series drop sharply. The bottom panel displays the median total loan amount for owner-

occupied purchase mortgages, with this total encompassing both first liens and any associated

piggybacks. The panel also shows the share of purchase mortgages made for owner-occupied

properties, which declines by almost 10 percentage points during the boom. Note also that

there is a hump shape in the median loan amount at the peak of the boom, when the

piggyback share and the investor share were highest.

A potential problem with using income information from HMDA is that the data reflect

only what the mortgage lender verified in order to qualify the borrower for the loan, so

HMDA data may not necessarily reflect the household’s total income. Mortgage lenders have

long favored income that can be documented and reasonably expected to continue into the

future. If the borrower is purchasing a relatively inexpensive property, then the mortgage

broker may not go to the trouble of documenting the stability of any income that is not

needed to approve the loan.

6

Consequently, when house prices rise, the incomes reported on

HMDA records may also rise, because borrowers will need to show more income to qualify for

the larger mortgages. This fact makes individual-level income as reported on HMDA records

potentially endogenous with respect to housing values. Additionally, as pointed out by Mian

and Sufi (2017), borrowers or mortgage brokers may misrepresent income to lenders if they

cannot document enough income to qualify for loans through legitimate means.

7

In light of

the potential discrepancies in incomes reported to HMDA, in our main HMDA regressions

we instrument for income using the median household income by tract from the decennial

Census and the American Community Survey (ACS).

6

Page D-10 of the 2013 Guide to HMDA Reporting states that: “An institution reports the gross annual

income relied on in evaluating the credit worthiness of applicants. For example, if an institution relies on

an applicant’s salary to compute a debt-to-income ratio but also relies on the applicant’s annual bonus to

evaluate creditworthiness, the institution reports the salary and the bonus to the extent relied upon.”

7

Some evidence on the potential endogeneity of incomes reported in the HMDA data comes from a com-

parison of HMDA incomes to Census income data. The decennial US Census and the American Community

Survey (ACS) include data on the incomes of homeowners with mortgages and who have recently moved.

Avery et al. (2012) find that average incomes reported on HMDA records were up to 30 percent higher than

incomes reported in the ACS in 2005 and 2006 in five states: California, Hawaii, Massachusetts, Nevada, and

New York. By comparison, in 2000 reported incomes in HMDA were no more than 10 percent above those

in the 2000 decennial census, and HMDA incomes from 2009 and 2010 were no more than 10 percent above

those in the ACS. These time-series and geographical patterns are consistent with a positive relationship

between house prices and reported HMDA incomes, although it is unclear how much of this correlation comes

from the need to document additional income as opposed to outright fraud.

6

2.2 The American Housing Survey (AHS)

Another source of both income and mortgage-debt data is the American Housing Survey

(AHS), which began in 1973 and has been conducted in every odd-numbered year since

1981. We use AHS data after a significant redesign in 1985.

8

The AHS is a joint project

of the US Department of Housing and Urban Development (HUD) and the Census Bureau

that is designed to measure the size, quality, and composition of the American housing stock.

The survey also measures monthly housing costs for US residents and collects information

on demographics and income of sampled households.

The AHS can be used to analyze the flow of new purchase-mortgage debt because the

survey includes information about the size of any existing mortgages at the time those mort-

gages were originated. Our sample consists of homeowners who moved into their residences

since the last AHS survey, for which the current mortgage is likely to be the purchase mort-

gage. Although the AHS includes no question asking whether the current mortgage on the

house is the actual purchase mortgage, we do know whether the mortgage was taken out in

the same year that the house was purchased, and we only use those mortgages. For income,

the AHS includes both wage income and the household’s total income. We use total income

in our regressions, but our results are essentially identical when only wage income is used.

9

Because the AHS income measures come from surveys, not mortgage applications, they are

much less likely to be influenced by housing prices. Indeed, Blackburn and Vermilyea (2012)

use the AHS to directly measure income overstatement in HMDA from 1995 to 2007; we

discuss that paper in more detail below.

As we do with the HMDA data, we take precautions regarding spurious outliers in the

AHS, where problems can arise for two reasons. First, consider a new homeowner appearing

in the 1991 AHS who moved into his residence in 1990, and then retired or significantly

cut back his working hours in 1991. His 1991 income would be much lower than the 1990

income used to qualify for his mortgage. Some recent homeowners who report only a few

thousand dollars of income in the survey year likely fit this scenario. A second problem arises

from the topcoding of income and debt. Like many household surveys, the AHS reports a

household’s income level only if it falls below some upper limit, which changes across survey

years. Mortgage debt is treated analogously, and income and debt levels above the topcode

limits are replaced with allocated values.

10

By truncating the top and bottom 5 percent of

8

For a general description of the AHS, see US Department of Housing and Urban Development (2017).

For discussions of the AHS as a data source for housing-finance issues, including new mortgage debt, see

Lam and Kaul (2003), Eggers (2007), and Eggers (2008).

9

The similarity of our results using either total or wage income is not surprising in light of the exclusion

of capital gains from the total-income measure. Because capital gains are rarely expected to continue year

after year, this source of income is typically not used to qualify for mortgage loans.

10

Early in the sample, the allocated values are the topcode limits themselves; later in the sample, the

allocated values are the mean values of income or debt above the respective topcode limits.

7

the debt and income distributions, we found that we could exclude all topcoded debt and

income values and also generate reasonable minimum income levels for home purchasers. As

we show in the appendix, however, our results are materially unchanged (albeit somewhat

noisier) when we run our regressions on the non-truncated data instead. Table 1 displays

the unweighted sample counts from the AHS, with the last column showing that our baseline

sample includes about 35,000 households in total.

Figure 2 compares median levels of new mortgage debt and income from HMDA and the

AHS.

11

The top panel shows that the time-series patterns of median mortgage debt line up

well across the two datasets, especially when we subset on metropolitan areas, where HMDA

reporting is concentrated. The lower panel, however, shows that income reported to HMDA

rises relative to AHS income during the height of the housing boom. The income pattern

thus confirms a lesson from Avery et al. (2012), who note that income reported to HMDA

potentially overstates a borrower’s true income in areas or periods where house prices are

rising rapidly. The pattern is also consistent with Blackburn and Vermilyea (2012), who use

the AHS to measure HMDA income overstatement from 1995 to 2007. The authors compare

the incomes of individual home purchasers in the AHS to local averages of reported HMDA

incomes for similarly sized mortgages that have matching borrower and loan characteristics.

They find income overstatement of around 15–20 percent in 2005 and 2006.

3 Income and Mortgage Debt in the 1990s and 2000s

3.1 The Canonical Debt-Income Regression

In the wake of the housing boom, the relationship between mortgage debt and income has

been a focus of much empirical research, most of which is based on some variant of what can

be called the canonical specification for the debt-income relationship:

D

it

= α

t

+ β

t

I

it

+

it

, (1)

where D

it

is the log of the value of a new mortgage originated for individual i in year t, I

it

is

log income, and the coefficients α and β have subscripts because they can change over time.

Empirical estimates of β, the partial correlation between new debt and income, are positive

because higher-income households tend to live in more expensive houses and take out larger

mortgages. Additionally, low-income borrowers might face limits on the amount of mortgage

debt they can take on, via ceilings on permissible DTI ratios. Relaxing these limits allows

low-income households to take out larger mortgages, which increases the amount of debt at

11

Because the median levels are not affected by the truncation rule, the AHS series are generated using

the non-truncated sample of homeowners who recently moved into a new residence.

8

the bottom of the income distribution and causes a decline in the positive cross-sectional

relationship between debt and income that is summarized by β.

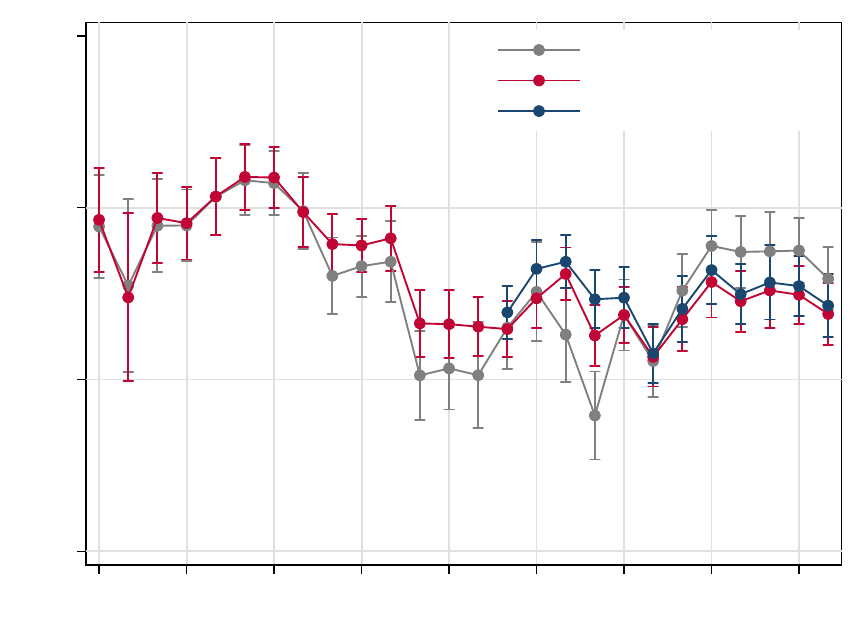

Figure 3 motivates the regression analysis with binned scatter plots of log debt and

income using individual-level data from HMDA and the AHS. In both cases, the cross-

sectional relationship between income and debt is nearly linear in logs. The plots also show

that for both data sources, the positive relationship between debt and income flattens from

the beginning to the end of the sample periods. By running the canonical regression and

examining the yearly βs that result, we can determine precisely when these declines took

place.

3.2 Regression Results

We first use the canonical specification to study the data on individual-level debt and income

obtained from HMDA. Some limited demographic variables are available in that dataset,

and we are also able to include CBSA-year fixed effects to control for local housing market

characteristics, including area-wide fluctuations in housing demand.

12

The CBSA-year fixed

effects also correct for any over-reporting of income that is consistent across a local market

in a given year. We modify Equation 1 to

D

it

= α

ct

+ β

t

I

it

+ γX

it

+

it

, (2)

where the vector X

it

includes dummy variables denoting the borrower’s race and gender,

while c indexes the CBSA. Note that α

ct

is indexed by CBSA as well as by time, so this term

now represents CBSA-year fixed effects.

13

Because income reported in HMDA can potentially

be overstated, as described in Section 2, we instrument for individual-level income reported

to HMDA with median tract-level household income from the decennial Census and the ACS.

The top panel of Figure 4 displays the β

t

s resulting from this regression, which trend

downward from 1990 through the early 2000s. This trend is consistent with a steady decline

in the partial correlation of income and debt until the housing boom begins, at which point

there is an increase in the estimated β

t

s. The bottom panel displays expected mortgage

amounts, which are calculated from a regression that includes only yearly intercepts α

t

rather than CBSA-fixed effects α

ct

. The estimates of these intercepts are added to the

yearly estimates of a β

t

× I

.t

interaction, where I

.t

denotes the mean of income in the entire

sample. These expected amounts increase sharply after 2000, when the well-documented

12

CBSAs, or core-based statistical areas, consist of at least one urbanized core with a population of 10,000

or more, along with adjacent counties that have a high level of social and economic integration. CBSAs have

been the main way that the US government classifies metropolitan areas since 2003.

13

In this regression, we will cluster the standard errors by CBSA, but the results remain robust when

clustering by state.

9

increase in aggregate US mortgage debt to aggregate US income takes place.

14

Figure 5 presents analogous results using the AHS. Recall that in this dataset, there is

no need to instrument for income, which comes from survey data, not loan applications.

Unfortunately, the small sample sizes in the AHS mean that we cannot run regressions with

CBSA-year fixed effects.

15

The top panel in Figure 5 mimics the HMDA results, in that the

debt-income relationship summarized in β

t

declines throughout the 1990s and flattens out in

the 2000s. The bottom panel shows the estimates of expected mortgage amounts. As with

the HMDA data, these amounts increase rapidly during the housing boom.

4 Mortgage Debt and Income in the 2000s

The stability of the debt-income coefficients throughout the 2000s in both the HMDA and

AHS regressions confirm a central finding in Adelino, Schoar, and Severino (2016): the

debt-income relationship remained stable during the 2000s housing boom. Because we have

treated second liens consistently over the sample period, and because we have addressed the

possibility that individual-level income in HMDA can be overstated, our findings are immune

to the criticisms of Adelino, Schoar, and Severino (2016) advanced by Mian and Sufi (2017).

The average-size finding is important because it speaks directly to what caused the 2000s

housing boom. An exogenous expansion of credit would be expected to flatten the cross-

sectional relationship between debt and income, because this expansion would have the

largest effect on the mortgages taken out by the most-constrained borrowers, who are located

at the lower end of the income distribution. The fact that no flattening occurred in the 2000s

argues against this type of exogenous expansion. An alternative explanation for the housing

boom is overly optimistic expectations regarding future house prices, which encouraged both

high- and low-income households to increase their exposure to the housing market (Foote,

Gerardi, and Willen 2012; Gennaioli and Shleifer 2018).

Yet the stability of the 2000s coefficients is only one piece of evidence regarding the source

of the boom. An exogenous credit expansion can occur along the extensive margin, in which

a larger number of low-income borrowers are approved for mortgages.

16

Neither the HMDA

14

Figure A.2 in the appendix contains the results from parallel regressions that do not include CBSA-year

fixed effects and that do not use Census tract-level median household income as an instrument for income

reported to HMDA.

15

We can, however, include yearly fixed effects for the United States’s four Census regions: Northeast,

Midwest, South and West. These results, along with additional robustness checks, are included in Figure

A.3 in the appendix.

16

Indeed, in their 2017 response paper to Adelino, Schoar, and Severino (2016), Mian and Sufi write that

their original 2009 paper was focused on the extensive margin: “As a final note, it is important to note that

[Mian and Sufi (2009)] focused on the extensive margin of mortgage lending, and the key argument in the

study was that credit expanded on the extensive margin toward low-credit-score individuals, defined as those

with a credit score below 660” (Mian and Sufi 2017, p. 1841). Although this quotation references zip codes

10

data nor the AHS can speak to the extensive-margin possibility, because neither dataset

tells us how many mortgages were terminated. For example, the HMDA data shows that

relatively more mortgages were originated in low-income zip codes during the boom. But

the data are silent as to whether the additional mortgages resulted in new homeowners, as

opposed to the new mortgages simply replacing or refinancing existing mortgages. A related

question is whether a change in one flow of mortgage debt (the number of originations)

resulted in a change in relative stocks of debt across the income distribution.

To answer this question, we need other data. In Foote, Loewenstein, and Willen (2019),

we use information from the Equifax credit bureau and the Survey of Consumer Finances

(SCF) to study both the stock of mortgage debt and the extensive margin of credit alloca-

tion.

17

In both datasets, and using several ways of distinguishing households cross-sectionally,

we find that stocks of debt rose proportionately during the boom, just as the average size of

new mortgages did. Stocks of debt behaved in this way because the higher number of mort-

gage originations in low-income zip codes was cancelled out by a higher number of mortgage

terminations so that, on net, there was no relative extensive-margin expansion of credit to

low-income areas.

18

Yet the results above also show that during the 1990s, the debt-income relationship did

flatten, suggesting that an exogenous credit expansion occurred during that decade. What

might have caused this expansion, and what effect did it have on the US housing market?

We take up those questions next.

grouped by credit score, current research focuses on the debt-income relationship, which was also studied in

Mian and Sufi’s original paper. In practice, this makes little difference, because zip codes with low credit

scores tend to have low-income residents as well.

17

Adelino, Schoar, and Severino (2016) also include a graph that uses the SCF, but it displays debt-

to-income ratios of borrowers in different income categories. Thus it does not shed light on the extensive

margin—that is, whether the number of new borrowers expanded differently across the income distribution.

18

In the appendix of Foote, Loewenstein, and Willen (2019), we show how these findings are consistent

with the purported “negative correlation” between mortgage credit and income during the boom discussed

in Mian and Sufi (2009). First, as we have noted, the mortgage credit referred to in Mian and Sufi (2009) is

mortgage credit originated, not the stock of mortgage debt. Second, the regression used to show a negative

correlation projects the growth in mortgage credit originated in a zip code on the growth of income. But this

growth specification is appropriate only if the correlation under study remains stable across years; the proper

regression to study a potential change in a correlation is in levels. Taking these two factors into account

overturns the negative-correlation finding, as the zip-code level income is always positively correlated with

both flows and stocks of debt. The positive correlations of income with the two flows decline during the

boom, reflecting a relative increase in both mortgage originations and terminations in low-income areas.

But because the increases in the two debt flows offset one another, the increases do not result in a relative

increase in the stock of debt in poorer areas.

11

5 Mortgage Debt and Income in the 1990s

5.1 Interest Rates and Government Policy

Two related factors affecting the US mortgage market during the 1990s were the long decline

in nominal interest rates and the emergence of a truly national mortgage market. The top-

left panel of Figure 6 shows the mean and median nominal interest rate paid by movers in

the AHS, along with the conventional 30-year rate for US mortgages published by Freddie

Mac. The top-right panel shows that the dispersion in interest rates began to decline in

1985, a finding that is consistent with the increased geographic competition among lenders

that took place during this period.

19

But the lower left panel shows that the β

t

s estimated by

our canonical regression display the same pattern even after controlling for individual-level

interest rates, by allowing for yearly interest-rate effects as well as yearly income effects (the

interest-rate coefficients themselves appear in the lower right panel).

The 1990s also saw a series of policy decisions intended to ensure that low-income house-

holds had access to mortgage credit (Wallison and Pinto 2012; Morgenson and Rosner 2011;

Rajan 2010). Research in this area often cites the Clinton administration’s National Home-

ownership Strategy of 1995, a policy initiative that encouraged housing-market participants

from the private and public sectors to increase the number of US homeowners by 8 million

by 2000. The varied nature of the 100 action items in this strategy make it difficult to

assess this effort’s direct effects. These items ranged from building-code reform (item 8),

home mortgage loan-to-value flexibility (item 35), subsidies to reduce down payment and

mortgage costs (item 36), flexible mortgage underwriting criteria (item 44), and education

on alternative forms of homeownership (item 88).

Other regulations designed to increase US homeownership included the Community Rein-

vestment Act (CRA), which was passed in 1977 but strengthened in the 1990s, and a 1992 act

that encouraged the government-sponsored enterprises (GSEs) to increase credit availability

in low-income or underserved areas. Part of the GSE’s efforts to expand mortgage credit

to underserved borrowers were conducted through affordability programs, such as Freddie

Mac’s Affordable Gold program, which began in 1992. Among other things, the Affordable

Gold program relaxed front-end and back-end DTI limits to 33 and 38 percent, respectively,

and also allowed smaller down payments.

20

19

There is a long literature on the integration of the mortgage market with national capital markets,

which limits the dispersion in mortgage interest rates paid by US households. A classic reference is Rudolph

and Griffith (1997) and a more recent paper is Hurst et al. (2016).

20

In some cases, the back-end ratio could rise to 42 percent. The normal limits for these ratios was 28

and 36 percent. The program also allowed borrowers to contribute less than the full 5 percent down payment

from their own funds, and required participants to take a financial counseling course before purchasing a

home. Fannie Mae had a similar program, called the Community Homebuyer Program, that began in 1990.

See US Department of Housing and Urban Development (1996, p. 90) for details.

12

Could the shift in government and GSE policies during the 1990s be responsible for the

decline in the debt-income coefficients we find for those years? Government policies that

rewarded lenders for making loans to underserved areas have been subject to a number of

empirical tests, but regression-discontinuity studies fail to show that either the CRA or the

1992 GSE act had much of an effect (Bhutta 2011, 2012; Avery and Brevoort 2015). For our

part, we believe that while the GSE policy changes during the 1990s might explain some of

our results, particularly in the early 1990s, the policy changes are not the whole story. The

main reason why is that the debt-income coefficients from the regressions have remained low,

even after the housing boom of the 2000s ended and GSE policy goals shifted. This stability

points to a more fundamental and longer-lasting change in the evaluation of mortgage-credit

risk during the 1990s that was separate from, but perhaps complimentary to, the GSE’s

goals at the time.

5.2 Decline in Mortgage-Processing Timelines

The best explanation for a longer-term change in credit allocation during the 1990s is that it

stemmed from technology-augmented innovation. As noted earlier, significant technological

advances in mortgage lending occurred during the 1990s (LaCour-Little 2000; Bogdon 2000;

Colton 2002). We provide some new evidence on those advances by illustrating the decline in

the time required to originate a new mortgage that occurred during the 1990s. Our analysis

of mortgage-origination timelines is made possible by the use of the confidential HMDA data;

as noted in the data section, these data include both the application date of each mortgage

as well as its so-called action date, when either the application is denied or a mortgage is

originated. The mortgage timeline is simply the number of business days between the appli-

cation and origination dates. A number of factors determine these timelines, including the

volume of applications processed by the lender, the lender’s size, and whether the borrower

is applying alone or with a co-applicant. To account for as many of these determinants as

possible, we run loan-level regressions that project the time required to process a loan on

the assets of the lender (in logs), the lender type (credit union, thrift, mortgage company,

and so on), the race and gender of the borrower, whether the borrower has a co-applicant,

and a concurrent measure of mortgage application volume.

21

Figure 7 depicts the results of these regressions. Between 1995 and 1998, there is a

dramatic decline in the average processing time for refinances, which then continues to drift

lower until 2005. The timeline increases after 2007, but on average it remains about 10

business days faster today compared to before 1995. There is no such pattern for purchase

21

Our measure of lending volume is the average number of mortgage applications per business day in each

month using the HMDA data. To account for seasonality, we only consider loans originated in the second

and third quarter of each year; other methods of accounting for seasonality give similar results.

13

loans. This is not surprising, because the closing dates for purchase loans are often chosen

to accommodate the borrower and seller as they move to new residences. Consequently,

the time between a purchase-loan application and the closing date can be lengthy, even if

the borrower has been pre-approved and has provided much of the necessary documentation

before making an offer on the house.

After the US housing boom ended, refinance timelines increase sharply as various lender

and governmental policies changed. One of the most significant policy changes involved the

repurchase policies of the GSEs. Fannie Mae and Freddie Mac occasionally require mortgage

originators to repurchase loans that do not meet the agencies’ underwriting guidelines. After

housing prices fell, both Fannie and Freddie increased their repurchase requests to originators

that had incorrectly underwritten loans. This prompted originators to follow GSE policies

more carefully, which likely lengthened origination timelines. The post-crisis period also

saw new disclosure rules for mortgage originators.

22

One goal of the new rules was to give

borrowers more information about mortgage offers at the start of the origination process, so

that they could better shop around for the best deal. Additional disclosures near the end

of the process were intended to ensure that borrowers were not surprised at the loan closing

about any features of the mortgages they ultimately chose.

The new disclosure regulations may well be a net plus for the housing market, because

they provide potential borrowers with important information about their loans. Additionally,

any effects of the new regulations or GSE practices on origination costs and timelines may

fade as lenders adapt to them and the rules themselves evolve. Indeed, as discussed in

Goodman (2017), the GSEs began instituting new policies for loan repurchases in September

2012; these policies include time limits on repurchase requests for newly originated loans and

additional guidance on the types of defects that might prompt a repurchase.

23

Although

further research is needed, our main point is that rule changes in the wake of the crisis may

well explain the recent increase in origination timelines.

5.3 Credit Scores versus Artificial Intelligence (AI)

The decline in mortgage timelines during the 1990s provide a good summary statistic for

the rapid technological progress then tranforming mortgage markets. But the specific tech-

nological innovation that most affected the debt-income relationship was the use of com-

puters to evaluate credit risk. As discussed in the introduction, computerization in the

22

The Dodd-Frank Act of 2010 instructed the new Consumer Finance Protection Bureau to propose rules

that would combine and integrate mortgage disclosures under the Truth in Lending Act (TILA) and the Real

Estate Settlement Procedures Act (RESPA). The final rule, called the TILA-RESPA Integrated Disclosure

(TRID) Rule, became effective in 2013.

23

See also the Housing Wire story titled “Fannie Mae, Freddie Mac Announce New Mortgage Buyback

Rules,” by Ben Lane, Oct. 7, 2015.

14

mortgage-lending industry was initially expected to take the form of artificial-intelligence

algorithms that would replicate mortgage underwriters’ decisions. But the intuitive decision

rules employed by human underwriters proved difficult to code into formal algorithms, and

the development of AI systems in the early 1990s eventually turned out to be a dead end.

As one industry professional wrote, these algorithms “gave speed and consistency to the

underwriting process, [but] by 1995 their accuracy was seriously questioned. These systems

were built to reproduce manual underwriting without much consideration of whether the

manual-underwriting thought process was optimal” (Makuch 1998, p. 4).

At the opposite end of the spectrum was a method that would prove much more accurate:

numerical credit-scoring algorithms. An example of such an algorithm is a linear default re-

gression that projects binary default indicators on variables derived from borrowers’ credit

histories and the risk characteristics of their loan applications. A more complicated algo-

rithm to predict default risk might be estimated via machine learning, using nonlinear or

hierarchical relationships among the relevant variables. In either case, the resulting default

model could be used to construct predicted probabilities of default, which would then inform

a mortgage lender’s decision regarding whether to make a loan and the interest rate that

should be charged. Credit-scoring algorithms have been used in one form or another at least

since the 1970s; the first modern version of the FICO score appeared in 1989. Previous re-

searchers have shown that the distillation of high-dimensional information from credit records

into a single score had a substantial impact on many types of consumer loans, particularly

credit cards (Evans and Schmalensee 2005).

Yet even as credit scoring transformed consumer lending in the 1990s, many lenders

doubted that credit scores could help them predict mortgage-default risk. Unlike consumer

debt, mortgages are secured loans, and the borrower’s equity stake in the property plays

a critical role in the default decision. In fact, the central project for academic economists

studying mortgage default in the 1980s and 1990s was building the so-called frictionless

option model (FOM), in which borrower-specific variables, including credit scores, play no

role in the default decision. In the FOM, the borrower’s default decision is fully characterized

by the level of negative equity at which the borrower should “ruthlessly” or “strategically”

default. This threshold equity level is a complex and time-varying function of borrower

equity, house prices, and interest rates. Individual-level adverse life events such as job loss

and illness do not lead to default in the FOM, because the model assumes that borrowers

can ride out these problems by obtaining unsecured loans at the risk-free rate.

In reality, many borrowers are liquidity constrained, so adverse shocks can lead to default

when borrowers are underwater on their mortgages. The mortgage-default literature is now

attempting to blend insights from the FOM with those of the “double-trigger” model, which

15

links default to the simultaneous occurrence of negative equity and an adverse life event.

24

In these models, borrowers who suffer adverse life events often lack the liquid funds needed

to remain current on their mortgages and are unable to take take out unsecured loans to

tide themselves over. Those borrowers who also have negative equity are unable to sell their

homes at a price that is high enough to discharge their obligations, so default occurs.

Another relevant finding from the mortgage-default literature concerns those negative-

equity borrowers who do not suffer adverse life events. For these unconstrained borrowers,

most calibrations of the FOM generate optimal default triggers in the neighborhood of 10–25

percent negative equity (Kau, Keenan, and Kim 1994; Bhutta, Dokko, and Shan 2017). In

empirical data, however, negative equity typically exceeds this level without the borrower

defaulting. This result is relevant for mortgage-default modeling because it suggests that

empirical models do not have to predict the relevant negative-equity default thresholds in a

way that is consistent with the FOM.

The overall characterization of the default decision that emerges from this research sug-

gests that initial LTV ratios and credit scores should be included in any empirical default

model. Low initial LTV ratios (that is, high down payments) reduce the probability of fu-

ture negative equity, so low LTV ratios reduce the probability of both double-trigger and

strategic defaults. Borrowers with high credit scores should also be less likely to experience

double-trigger defaults if these scores reflect low probabilities of experiencing a liquidity

shock, either because the borrower has a stable job, or because he has ample liquid wealth.

25

Although borrower income is critical in the new generation of default models, the role

of future income shocks, as opposed to initial income levels, suggests that DTI ratios at

origination should not affect default very much. In the double-trigger model, default occurs

when an income shock raises the borrower’s current DTI ratio to very high levels. Origination

DTI ratios should matter only to the extent that low DTI ratios make it less likely that a

borrower will experience a shock large enough to trigger default. The variance of income

shocks at the individual level is so high that setting a low DTI ratio at origination may not

offer the lender much insurance in that regard (Foote et al. 2009). After all, in the case of a

job loss that halts income completely, the borrower’s DTI rises to an infinite level no matter

how low the origination DTI ratio had been.

24

Examples of this work include Corradin (2014), Campbell and Cocco (2015), Laufer (2018), and Schelkle

(2018). For a survey of recent research in this area, see Foote and Willen (2018).

25

High credit scores may also indicate that the borrower assigns a high “stigma” cost to any type of

default. This possibility also supports the inclusion of credit scores in mortgage-default models.

16

5.4 Integrating Credit Scores into Mortgage Lending Decisions

Empirical models estimated with individual mortgages confirm these theoretical predictions.

In a very early study sponsored by the NBER, Herzog and Earley (1970) used data from

13,000 individual loans and found that initial LTV ratios were good default predictors; in

the following decades, subsequent studies confirmed this result. Later researchers found

that the new credit scores developed in the 1990s also entered mortgage-default regressions

significantly. Mahoney and Zorn (1997) discuss Freddie Mac’s modeling work in the early-

to-mid 1990s, noting that borrowers with FICO scores less than 620 were found to be more

than 18 times more likely to experience foreclosure than borrowers with scores greater than

660. Yet DTI ratios proved to be much weaker default predictors. An influential Federal

Reserve study (Avery et al. 1996) summarized the existing consensus in both industry and

academia by noting that “[p]erhaps surprisingly, after controlling for other factors, the initial

ratio of debt payment to income has been found to be, at best, only weakly related to the

likelihood of default” (p. 624). The Fed study also presented original research showing that

credit scores were good predictors of default and could be used to improve lending decisions:

“[t]he data consistently show that credit scores are useful in gauging the relative levels of

risk posed by both prospective mortgage borrowers and those with existing mortgages” (p.

647).

Armed with this information, the GSEs began encouraging loan originators to use credit

scores in their lending decisions. In July 1995, Freddie Mac’s executive vice president for risk

management, Michael K. Stamper, sent a letter to Freddie’s sellers and servicers encouraging

them to use credit-score cutoffs when underwriting loans. Loans with FICO scores over 660

should be underwritten with a “basic” review, while borrowers with scores between 620 and

660 should get a more “comprehensive” review. For borrowers with FICO scores below 620,

underwriters should be “cautious,” in that they should:

[P]erform a particularly detailed review of all aspects of the borrower’s credit his-

tory to ensure that you have satisfactorily established the borrowers’ willingness

to repay as agreed. Unless there are extenuating circumstances, a credit score

in this range should be viewed as a strong indicator that the borrower does not

show sufficient willingness to repay as agreed. (Stamper 1995, p. 2)

The letter also explicitly permitted lenders to use high credit scores to offset high DTI

ratios: “A FICO bureau score of 720 or higher. . . will generally imply a good-to-excellent

credit reputation. If your underwriter confirms that the borrower’s credit reputation is

indeed excellent, then it could be used a compensating factor for debt-to-income ratios that

are somewhat higher than our traditional guidelines . . . ” (Stamper 1995, p. 13). Within a

few months, Fannie Mae followed suit by encouraging lenders to use credit-score cutoffs that

17

were identical to the ones recommended by Freddie Mac.

26

In addition to supporting the general use of credit scores, the empirical default models

were used to develop numerical scorecards that could weigh all the data in a loan applica-

tion. One scorecard produced by Freddie Mac was the Gold Measure Worksheet, which was

designed to assist underwriters in evaluating applications for the Affordable Gold program.

This worksheet, which also appeared in Avery et al. (1996) and which we reprint as Figure

8, allocated risk units to a loan application based on the borrower’s LTV ratio, DTI ratio,

credit score, and other credit information. If a loan had 15 or fewer total risk units, then

the loan met Freddie’s underwriting standards.

The implicit weights in the worksheet reflect the lessons about the determinants of mort-

gage defaults that had been learned from empirical default models. Most importantly, the

worksheet assigns a high importance to equity and credit scores and a low importance to

origination DTIs. The table below illustrates this pattern by using the worksheet to evaluate

three hypothetical loans. Loan A has an LTV of 90 percent, a FICO score of more than 790,

and a DTI ratio exceeding 50.5 percent.

27

Although the DTI ratio is very high, the high

FICO score offsets this penalty by enough to reduce the total risk-unit score to 14, which is

one unit below Freddie’s approval cutoff. The application for Loan B is generated by a hy-

pothetical borrower with a low credit score and carries a much smaller DTI ratio. This loan

turns out to be too risky, as its 17 risk units are two units above Freddie’s cutoff. Finally,

Loan C has very high LTV and DTI ratios (99.5 percent and 50.5 percent, respectively), as

well as an adjustable interest rate. But the borrower also has a credit score of more than 790

and five months of liquid financial reserves. Because the latter factors are enough to offset

the high DTI and LTV ratios, the loan just makes the risk-unit cutoff.

Although the Gold Measure Worksheet fit on a single page and took only minutes to

complete, it proved to be far more accurate in predicting default than human underwriters,

who also took much longer to evaluate each loan file. The superior speed and accuracy of

scorecard-based evaluations were illustrated powerfully in a head-to-head comparison be-

tween human underwriters and the computer-based scorecard that is described in Straka

(2000). Sometime after 1994 Freddie Mac purchased about 1,000 loans from a major lender

through the Affordable Gold program. After Freddie Mac received these loans, the agency’s

quality-control investigators indicated that the loans’ risk characteristics fell outside of Fred-

die Mac’s guidelines, so a sample of 700 loans was scored using the Gold Measure Worksheet.

This exercise, which took only a few hours, indicated that only about half of the loans were

“investment quality” and thus eligible for purchase by Freddie Mac. At that point, human

underwriters then re-evaluated all 1,000 mortgages, a process that took six months. The

26

See Poon (2009, p. 663) and Dallas (1996) for details of Fannie Mae’s instructions.

27

This DTI ratio is the back-end ratio, so it encompasses not only the borrower’s mortgage payment but

also car loans and other regular installment payments.

18

Fixed or Total

LTV FICO DTI Months of Adjustable Risk

Ratio Score Ratio Reserves Rate Units

Loan A 90% Over 790 Over 50.5% 2–3 Fixed

Risk Unit Increment 0 –16 +30 0 0 14

Loan B 90% 640 Below 32.6% 2–3 Fixed

Risk Unit Increment 0 +17 0 0 0 17

Loan C 99.5% Over 790 50.5% 5 Adj.

Risk Unit Increment +13 –16 +18 –6 +6 15

Maximum Number of Risk Units

Suggested by Freddie Mac for Loan Acceptance 15

Evaluating Alternative Loans Using the Gold Measure Worksheet

Note: These calculations correspond to single-family, 30-year mortgages for which no special cases apply

(for example, the borrower is not self-employed). The adjustable-rate mortgage in Loan C is a rate-capped

ARM (not a payment-capped ARM).

Source: Authors’ calculations using the Gold Measure Worksheet in Figure 8.

underwriters also found that about half of the loans were good enough to be purchased

by Freddie Mac. Yet while there was some overlap between the two assessment exercises,

the underwriters and the worksheet delivered substantially different results on the set of

mortgages that met Freddie Mac’s standards.

By following these mortgages over time, Freddie Mac could conduct a horse race between

the worksheet and human underwriters regarding their respective abilities to predict mort-

gage default. As Straka writes, “the race was not very close.” During the first three years

after origination—a period when underwriting differences tend to have the strongest effect

on default outcomes—the worksheet ratings proved to be powerful predictors of mortgage

distress. The foreclosure rate on loans placed in the worksheet’s noninvestment category

was almost three times higher than the foreclosure rate for loans in the investment category;

the 30-day delinquency rate was nine times higher. But loans determined to be below in-

vestment quality by the underwriters performed almost exactly the same as the loans that

the underwriters approved, despite the higher extra cost of the human evaluations: “[r]eview

underwriting ratings that took six months to complete performed not much better (if better)

than flipping coins” (Straka 2000, p. 219).

5.5 The Growth of Automated Underwriting

The next step was for the GSEs to leverage their central place in the US mortgage industry

(and their substantial financial resources) by developing software that incorporated their

19

default-prediction scorecards and that could be distributed directly to loan originators.

28

By

1995, both GSEs had developed automated underwriting (AU) systems: Loan Prospector at

Freddie Mac and Desktop Underwriter at Fannie Mae. These proprietary software packages

allowed loan originators to enter borrower and loan characteristics into a desktop computer,

which would then report how the GSEs would treat the loan. For example, an “accept”

rating from Loan Prospector meant that Freddie Mac would purchase the loan without

conducting additional analysis. Ratings of “caution” or “refer” required the originator to

perform additional screening before submitting the mortgage to the GSE for purchase.

As the GSEs gained more confidence with the ability of their AU systems to evaluate

risk, they began to expand the credit box. Evidence on this point comes from data in Gates,

Perry, and Zorn (2002), which we use to construct Table 2. The table reports the results

of two additional horse races that also use the set of Affordable Gold mortgages referenced

above. The two contests pit the human underwriters against the 1995 and 2000 calibrations

of Freddie Mac’s Loan Prospector AU system. The bracketed numbers in the table report

the 90-day delinquency rate for each group of loans, relative to the delinquency rate for the

entire sample; a rate of 1.00 indicates that the group defaulted at the same rate as the entire

sample. The non-bracketed numbers in the table refer to group shares, as percentages of the

entire sample of evaluated loans.

The first column reports the results from loans as they were classified by the human

underwriters. As noted above, the underwriters took six months to designate about half

of the loans as acceptable for purchase by Freddie Mac, although this group ultimately

performed about the same as the noninvestment-quality half did.

29

The next two columns

show how Freddie Mac’s 1995 model evaluated the sample. The bottom row of the 1995

accept column indicates that with only 44.8 percent of the mortgages labeled as acceptable,

the 1995 AU model was slightly more conservative than the human underwriters. But the

1995 AU model accepted many of the mortgages that the human underwriters rejected (a

group comprising 20.8 percent of the sample), while it rejected many mortgages that the

human underwriters accepted (27.5 percent). And the AU model appeared to pick the right

mortgages on which to disagree, as its accepted mortgages defaulted at only about one-fifth

the rate of the sample as a whole.

Gates, Perry, and Zorn (2002) observe that over time, “Freddie Mac rapidly expanded

accept rates as the tool became more accurate and the company gained experience with and

confidence in the new technology” (p. 380). This expansion is shown in the last two columns,

28

Freddie Mac was generally ahead of Fannie Mae in this effort. In fact, Fannie Mae started out as a leader

in developing computerized AI algorithms to mimic human decisions. But Fannie Mae officials eventually

realized that it was critical to incorporate lessons from empirical default models into any computerized

underwriting system. See McDonald et al. (1997) for details.

29

Indeed, the underwriters’ “accept” group had a relative default rate of 1.04, a bit higher than the default

rate for rejected half (0.96).

20

which depict accept rates and relative performance according to the 2000 version of Loan

Prospector. The model now accepts more than 87 percent of the sample, but the relative

delinquency rate of this group is still better than the 51.6 percent accepted by the humans

(0.70 vs. 1.04).

How much of this credit-box expansion involved an increase in permissible DTI ratios?

Once lending policies have been encoded into a proprietary automated underwriting system,

we can no longer evaluate them with comparisons of hypothetical loans, as we did for the

Gold Measure Worksheet. But relaxed DTI standards were no doubt an important part of

the credit expansion. As the use of AU systems grew in the late 1990s, some borrowers and

lenders became frustrated by their black-box nature, so the GSEs provided limited infor-

mation about their underlying scorecards in mid-2000. Freddie Mac, for example, reported

that DTI ratios (both front-end and back-end) were one of 14 factors that its algorithm

considered. But this ratio was not one of the three most important factors, which were

the borrower’s total equity, loan type, and credit scores. As for Fannie Mae, a well-known

syndicated real estate journalist wrote in mid-2000 that the most critical component of the

Desktop Underwriter system was the credit score, and the last of 10 factors listed was the

“payment shock.” This shock was not the DTI ratio itself, but the difference between the

new monthly mortgage payment and the amount that the homeowner was already paying

for housing. And mortgage brokers did not view this weaker income test as a “major tripper-

upper.”

30

6 Consequences of the 1990s Credit Expansion

A relaxation of current-income constraints should have the largest effect on borrowers with

low current incomes relative to their expected future incomes. Young college graduates have

relatively steep age-earnings profiles (Tamborini, Kim, and Sakamoto 2015), so we would

expect the credit expansion described above to have relatively large effects on that group.

The official homeownership rate is generated by the Current Population Survey/Housing

Vacancy Survey (CPS/HVS), so it is straightforward to test this prediction by disaggregating

the CPS/HVS microdata by age and education. Figure 9 shows that the post-1994 increase

in the homeownership rate was particularly large for younger persons with at least some years

of college (that is, for college graduates and for persons with some college attendance but no

degrees). The middle panel of the top row shows that among households headed by a 25–29

year-old, homeownership rates rose sharply among the more educated households, but barely

moved for less-educated households. Qualitatively similar but less pronounced patterns are

30

See “Building Blocks of Automated Underwriting,” by Lew Sichelman, United Feature Syndicate, June

4, 2000.

21

evident for older households as well.

31

For all but the youngest age groups, homeownership

rates for the college-educated are substantially higher than for the less-educated. Looking at

all the evidence, we see that the credit expansion of the 1990s essentially allowed younger and

better-educated households to purchase houses sooner than otherwise would have otherwise

been the case. These households had expectations of relatively high permanent incomes

(because of their educational attainment) but low current incomes (because of their ages).

32

In allowing some young people to buy homes sooner than they otherwise would have, the

credit expansion of the 1990s played out as a miniature version of the much larger credit

expansion that took place immediately after World War II. In the 20 years after 1940, the

introduction of zero-down-payment Veterans Administration loans and relaxed lending stan-

dards for mortgages insured by the Federal Housing Administration helped increase home-

ownership by nearly 20 percentage points.

33

Figure 10 uses data from the decennial Census

and the American Community Survey (ACS) to provide a more detailed look at homeown-

ership changes during various periods. The use of Census and ACS data rather than the

CPS/HVS allows us to disaggregate these changes in homeownership rates sorted by four

educational groups, rather than two, and also permits analysis by single-year-of-age rather

than five-year age groups. The top panel of Figure 10 depicts ownership changes by single-

year-of-age and education over the 1940–1960 period. As Fetter (2013) has shown, the main

effect of underwriting changes immediately after World War II was to raise homeownership

rates for younger adults, who were otherwise likely to purchase homes later in life. Eligibility

for the mid-century lending programs was broadly distributed across the population with

respect to education, so it is not surprising that young persons in all educational classes,

except high school dropouts, saw their homeownership rates increase dramatically. Using

the 1990 and 2000 Censuses and the 2005 ACS, the lower panels depict changes in ownership

between 1990 and 2000 (bottom left panel) and 2000 and 2005 (lower left panel). Although

the 1990–2000 panel shows little within-group increases, those in the 2000–2005 panel show

that younger college graduates were most affected by the changes in mortgage-lending re-

quirements, consistent with the above results from the HVS/CPS above. Homeownership

rates for persons with no college education did not change during this period.

31

For household heads under 25 years of age, homeownership rates rise for both higher- and lower-educated

households. But ownership rates for both groups remain small throughout the sample period.

32

The better-educated groups would also be less likely to experience income disruptions, because the prob-

ability that a worker transitions from employment to unemployment is an inverse function of his education

level (Mincer 1991; Mukoyama and Şahin 2006).

33

The homeownership rate rose from 43.9 percent in 1940 to 61.9 percent in 1960. See https://www.

census.gov/hhes/www/housing/census/historic/owner.html for ownership rates based on decennial Census

data.

22

7 Conclusion

During the last three decades, improvements in information technology have transformed

numerous aspects of American life, including mortgage lending practices. During the 1990s,

both mortgage and consumer lending were enhanced by technologies that not only processed

data more rapidly, but could also evaluate risk more efficiently and accurately than humans

could. For the mortgage industry, the new empirical models downplayed the role of current

income in future mortgage default, so the 1990s saw mortgage credit expand exogenously

with respect to income, a fact that makes the 1990s a particularly valuable period to consider

when studying how changes in lending standards affect the housing market. By and large,

the modest effects of this exogenous change on the overall US mortgage market are in line

with economic theory, but the effects run counter to the claim that an exogenous change in

lending standards during the 2000s was responsible for the period’s aggregate housing boom.

A close look at the data and the historical record indicates that DTI ratios at origination

became less important in lending decisions during the 1990s, consistent with modern theories

of mortgage default as well as the debt-income analysis presented in section 3. Data also

show that downplaying the importance of human judgment in default decisions improved the

evaluation of credit risk, which explains why numerical methods continue to be developed

today, via machine learning and other methods. To the extent that the information used in

these methods is racially neutral, the models also deliver racially unbiased lending decisions,

something that could not be taken for granted at the start of the 1990s (Munnell et al. 1996).

The decreased cost, increased accuracy, and unbiased nature of AU systems help explain why

they were embraced so quickly by mortgage lenders.

A deeper point is that the computerization of mortgage lending during the 1990s has