In order to be considered for commission eligibility under the Walt Disney World® Resort Commission Policy, the Aulani, a Disney

Resort & Spa, Ko Olina, Hawai'i Commission Policy, the Adventures by Disney Commissions Policy, the Disney Cruise Line

Commission Program and the Disneyland® Resort Commissions Policy, please submit the following requirements. This application is

for new travel agencies wishing to become eligible to receive commission payments and existing travel agencies that wish to modify

their profile.

For New Applicants, complete ALL of the following steps:

1. You MUST complete and return parts A & B of the U.S. Supplier Information Kit (see attached). The federal tax form and SS-4

or 147C are used to report commissions paid at the end of the year. If answering yes to any question regarding California on

the Disney substitute W-9 form, then a California 590 form (see attached) must also be submitted.

2. A cover letter on agency letterhead with all of the following in the body of the letter:

- Agency ID number (such as an IATA, CLIA, ARC and/or True number)

- Agency Name

- Physical Street Address (Express couriers

- will not deliver package documents to a post office box)

- City, State, and Zip Code

- Business Phone Number

- Agency Owner or Manager’s First and Last Name

- Agency Owner or Manager’s Email

- GDS system utilized by the Agency and Pseudo City Code (if available)

3. A completed Disney Destinations Travel Agency Profile Form (see attached)

4. Photocopy of business license and one of the following:

- Photocopy of a valid CLIA certificate and/or a valid IATA list or IATA certificate of appointment

5. A completed ACH Authorization Form (Part C of the U.S. Supplier Information Kit) for direct deposit for commission (see

attached)

For your security, a representative from Disney Worldwide Shared Services will be reaching out to you in order to validate the

addition of a new bank account or any changes to any existing bank account that you may currently have on file.

Banking account validation will be required and could cause a delay to your application completion if you cannot be reached

through the contact number you have provided.

All documents must be signed by the agency owner/manager and sent to both offices below to request setup for all

Disney Destinations (Note: no electronic signatures accepted):

Disney Reservation Center for Walt Disney World Resort, Aulani

Resort, Hawaii, and Disneyland Resort

Fax: 407-938-4115 or

Email: WDW[email protected]

Disney Cruise Line/Adventures by Disney

Fax: 407-566-3760 or

Email: TA.Maintenance@DisneyCruise.com

Contact: 407-939-7945 for additional assistance

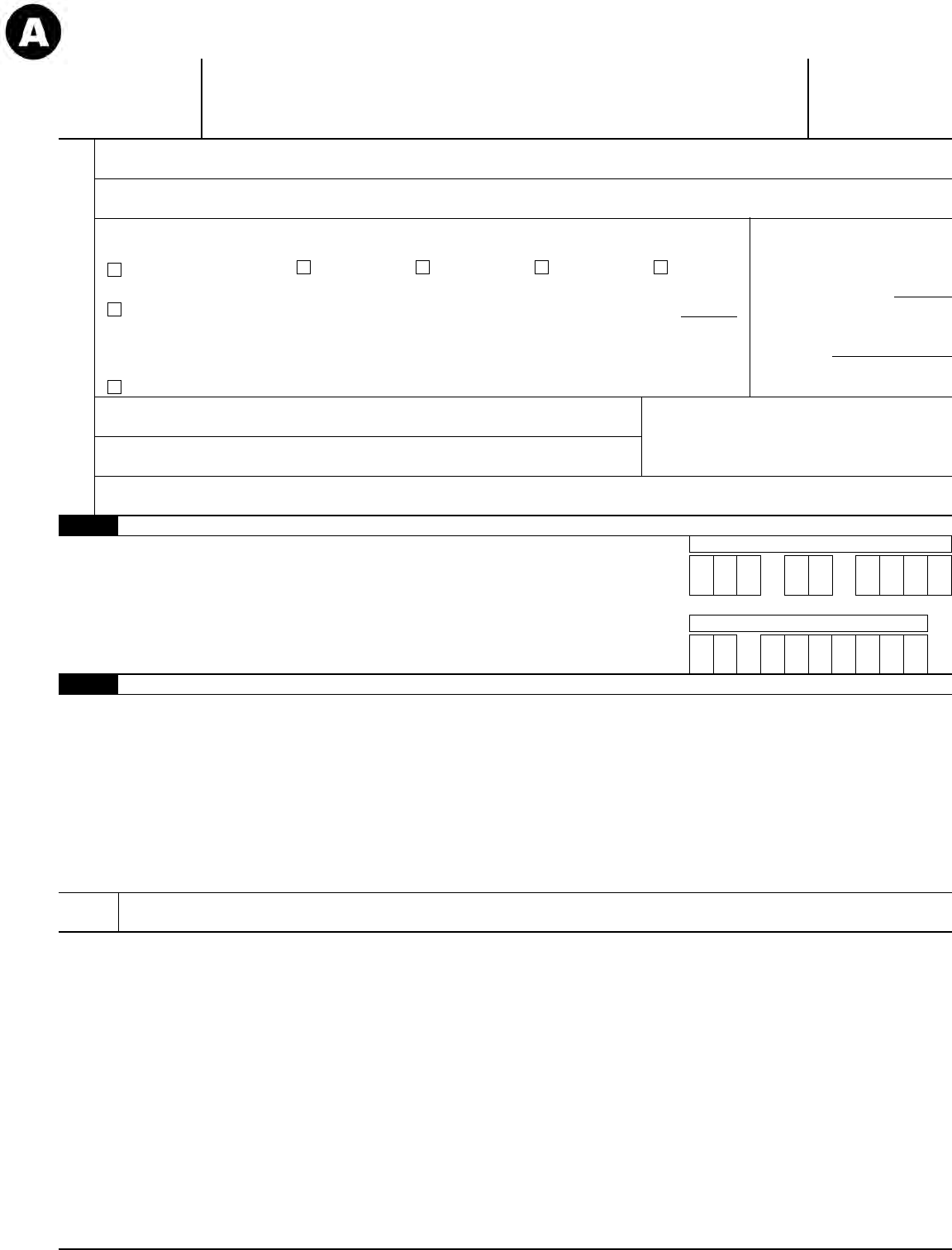

Travel Agency Commission Eligibility Application

TRAVEL AGENCY

PROFILE

1. Your Travel Agency’s legal name, exactly as it appears on business

registration and W9.

1a. Your Travel Agency’s brand name(s) if different than legal name.

1b. What is the address for the legal entity as stated on W9? (city, state,

zip, country)

1c. Will you be booking under your brand name(s) or legal name?

Brand name(s) Legal name

If multiple brand names, which ones you will be booking under:

1d. What year was your Travel Agency established?

1e. How many offices do you have using the same IATA and/or CLIA #?

1f

. Is this agency a headquarters or branch?

2. Name of Owner:

Name:

Title:

E-Mail:

Telephone:

3. Name of Manager:

Name:

Title:

E-Mail:

Telephone:

4. Physical Address:

Telephone:

Fax:

5. Are you a Home Based Agency? Yes No

6. Accounting information:

Billing Address: (If different from physical address)

Contact Name:

Title:

Telephone:

E-Mail:

6a. IATA #________________CLIA # __________________

ARC # _______________ TRUE#_______________________

6b. Has your agency been given a Pseudo IATA# in the past?

Yes No If yes, what was that number:

7. Your Travel Agency Website Address:

8. What % of business is done through your website? ________%

9. How will the Disney Product be promoted?

Website Newsletter Other (specify)

10. What Disney destinations do you plan to sell?

Walt Disney World® Resort ________

Disneyland® Resort ________

Disney Cruise Line® ________

Aulani ________

Adventures by Disney ________

11. How many agents do you have?

11a. How many agents are home based?

12. Ability to service clients in the following languages (check all that

apply):

English _______ Spanish ______ Portuguese ______

Japanese _______ Other _______

13. Are the agents experienced in selling Disney Product?

Yes No

14. How many agents are current with the College of Disney Knowledge

courses?

15. Does your Travel Agency bring group business to Orlando?

Yes No

If Yes, Leisure Incentive

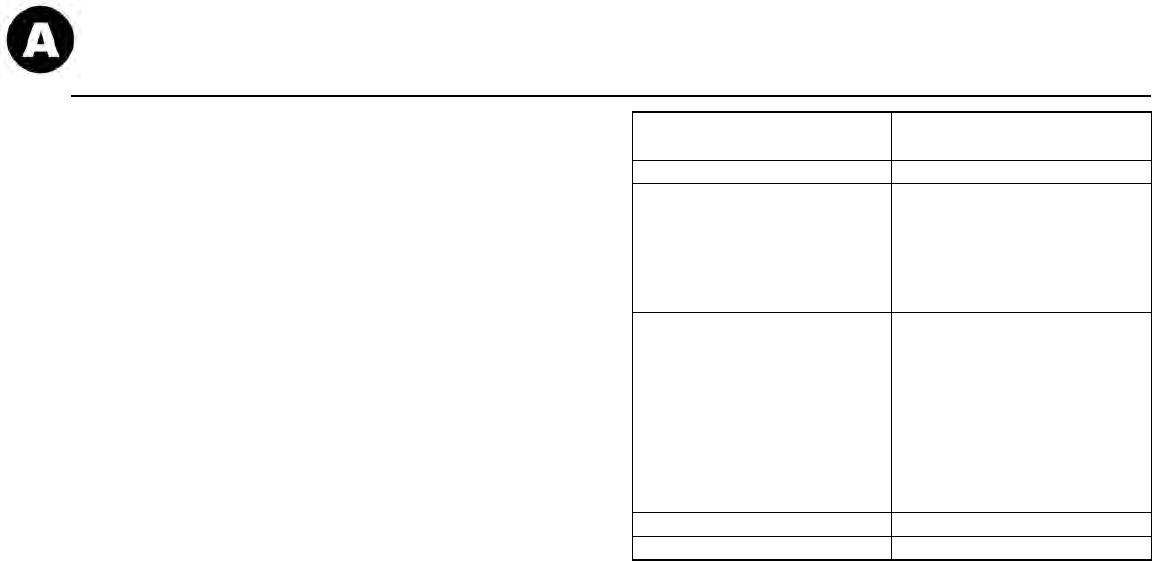

16. Has your Travel Agency previously been registered with Disney

under any other name(s)? [If “yes,” specify name(s)]

Yes No

17.

Has your Travel Agency previously done business under or used any

other name(s)?

Yes No

If “yes”, please list all names:

18.

Has any owner or manager of your Travel Agency owned all or part

of, worked for or with or managed any other travel agency that has

done business with Disney?

Yes No

If “yes”, list all such agencies:

19. Has any owner, manager, agent, employee or contractor of your

Travel Agency owned all or part of, worked for or with or managed

any other travel agency that (i) Disney made ineligible to receive

commissions from Disney or terminated any commission

arrangement with or (ii) Disney ceased to accept bookings, orders or

reservations from or (iii) Disney notified may no longer book

vacations or other product of Disney or (iv) received any notice from

Disney of early termination of any contract or of any default or

violation of any contract or policy?

Yes No

If “yes”, please give details:

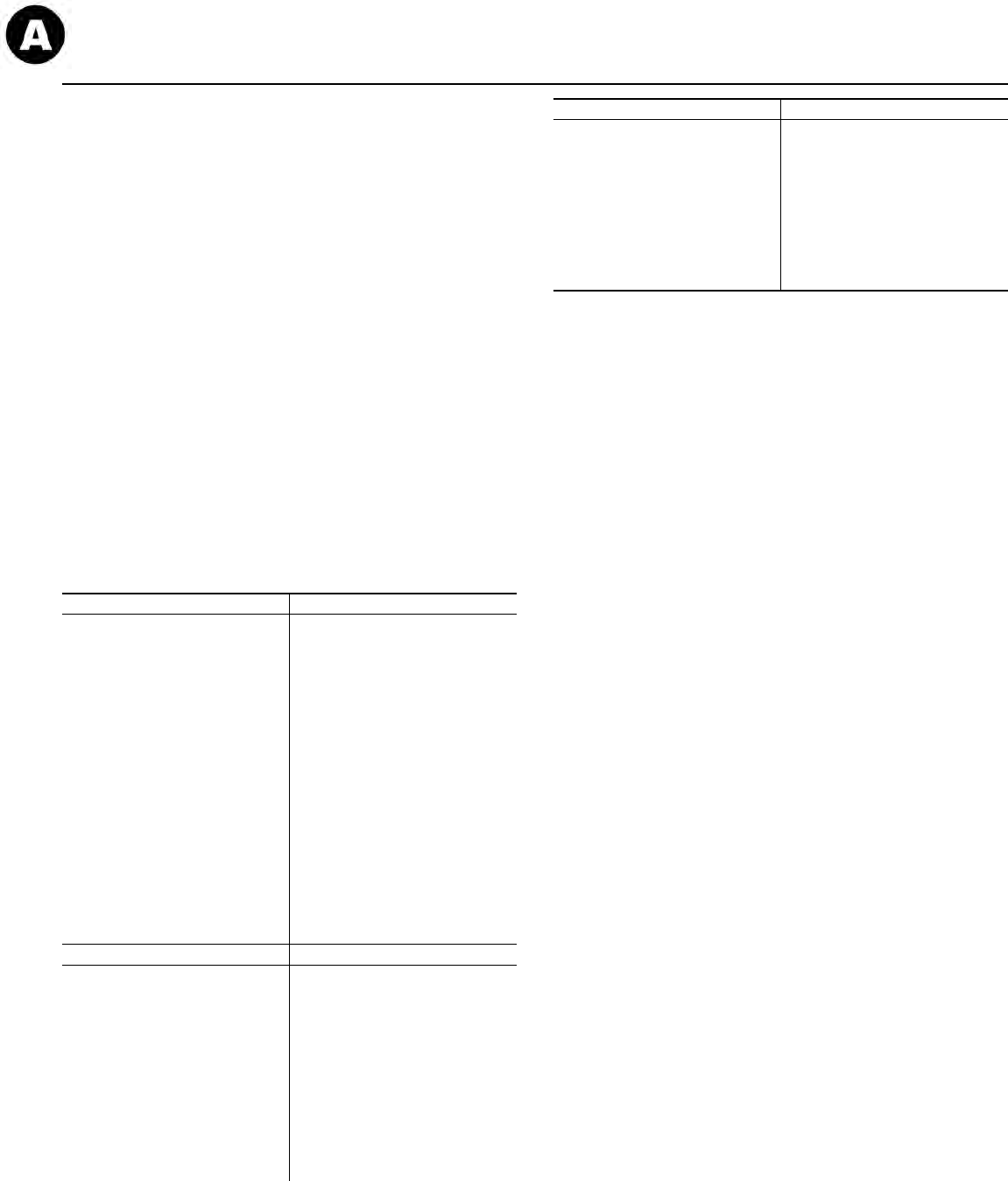

“Disney Intellectual Property” shall mean the names “Walt Disney

World® Resort,” “Disneyland® Resort,” “Disney,” “Pixar,” “ABC,” “ESPN,”

“Lucas” and “Marvel” (either alone or in conjunction with or as part of any

other word or name), and all fanciful characters, designs, trademarks,

copyrighted works and other intellectual property rights of The Walt

Disney Company and its affiliates (including, without limitation, Lucasfilm

Ltd. and Marvel Enterprises, Inc.).

Travel Agency shall neither acquire nor assert any proprietary right in any

Disney Intellectual Property, or in any derivation, adaptation or variation

thereof.

Travel Agency shall not apply to register or claim ownership of any Disney

Intellectual Property. Travel Agency shall not oppose or seek to cancel or

challenge any intellectual property ownership, application or registration of

Disney or its designee regarding any Disney Intellectual Property. Disney

or its designee shall have the right to enforce intellectual property rights

with respect to Disney Intellectual Property, and Travel Agency shall not

attempt to assert any such rights.

Any ideas, business proposals or suggestions provided by your Travel

Agency to Disney shall be deemed non-confidential and non-proprietary

and may be used or disclosed by Disney without liability or compensation,

unless otherwise expressly agreed to the contrary in writing by Disney.

Your Travel Agency acknowledges that all discussions and

communications shall be non-binding and no agreement or approval for

commission eligibility shall be deemed entered into or given unless and

until a formal, written notification, specifically identified as such, is

executed by Disney and delivered to your Travel Agency.

_________________________________________________

Legal Name of Travel Agency

By: __________________________ Date: _______________

Signature

Print Name: _______________________________________

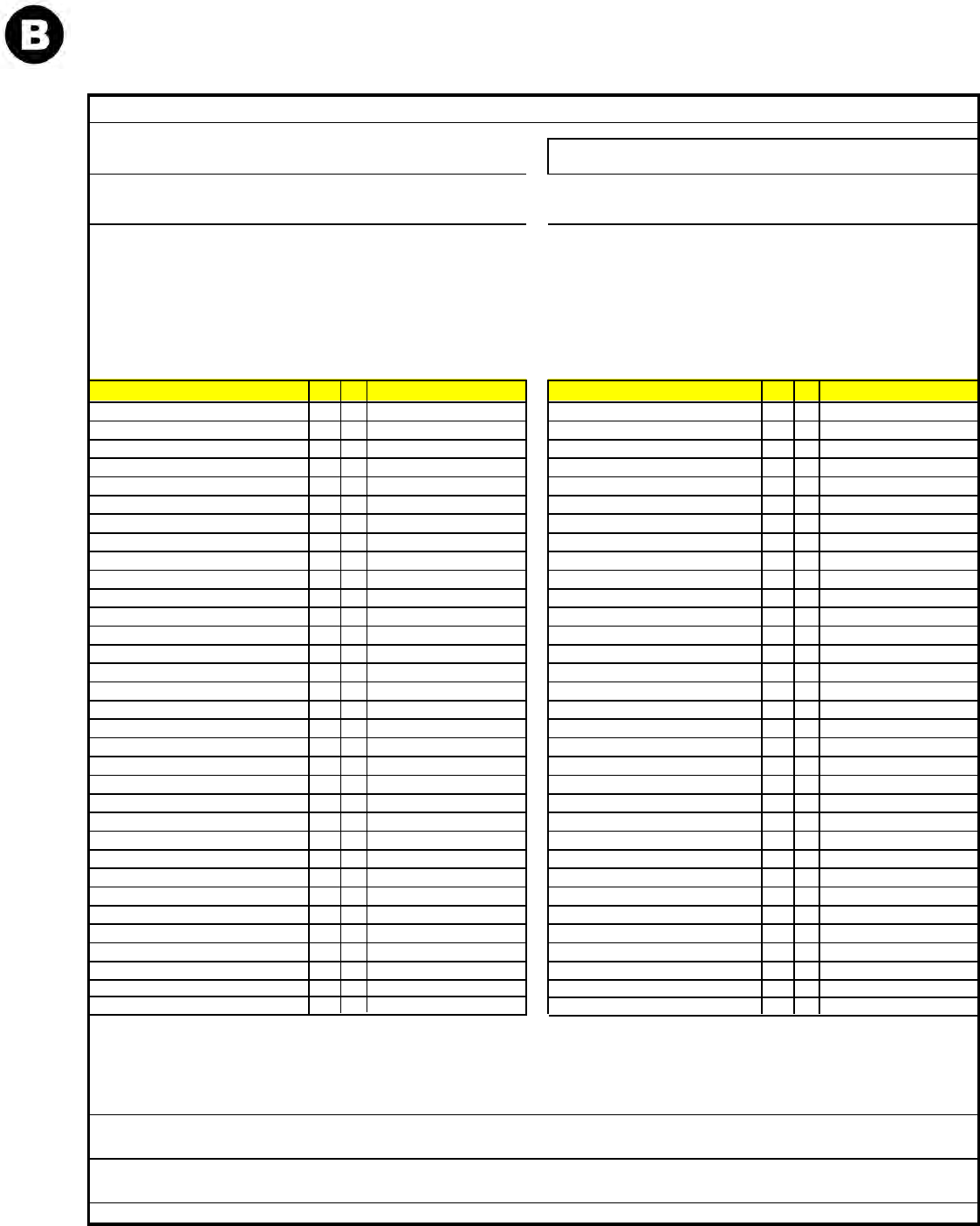

U.S. Supplier Information Kit

As a Disney Supplier, we require several pieces of information about your company. We

have simplified the process by splitting the information we need into four parts–A,B,C and

D. Forms to collect information in all four parts are attached in this kit.

New Suppliers—Please complete and return all four parts.

Please Fax or Email your completed Kit to your Disney representative:

Fax Number ________________________ Attn:________________________________

Please complete the Information Required for Proxy Setup form.

Part A also includes a W-9 form and a California Form 590. Note: The Form

590 may not be applicable to all Suppliers. If none of the selections apply to your company, note

N/A on the Form 590.

Disney’s SAP system calculates sales tax due. Part B is a form collecting

Supplier sales and use tax information for each state.

Disney supports electronic POs, invoicing and payment distribution. Part C is

a form collecting information about your company’s electronic transaction and

direct deposit ACH (Automated Clearing House) capabilities.

Disney is committed to Supplier diversity. Part D is a form that collects

ownership information about your company, so we can track our eligible

women- and minority-owned businesses.

A

C

D

When you receive the completed Kit from your Supplier, please log in to the Disney Supplier

Management Portal as a proxy and input the information.

B

Disney Casual Buyers/Requestors Use Only

U.S. Supplier Information Kit – Information Required for Proxy Setup

Name- _______________________________________________________________________________________

Title- ________________________________________________________________________________________

Phone Number- _______________________________________________________________________________

Fax Number (if using Purchase Orders)- ____________________________________________________________

Email Address- ________________________________________________________________________________

If you o

r your company have an existing vendor number with TWDC that is “no longer valid” due to tax number and/or tax status

changes or have undergone name and/or ownership changes please provide your current vendor name(s) and number(s) below.

This will help ensure that any invalid payable record(s) are closed according to TWDC policy.

__________________________________________________________________________________________

If you or your company utilizes a separate “Remit to Address” other than the “business address” noted on the W-9 (Form A),

please input here:

Address (number, street, and apt. or suite no.) -____________________________________________

City, state, and ZIP code - ______________________________________________________________

If you or your company utilizes a separate “Purchase Order Address”, please input the address or addresses below:

Address (number, street, and apt. or suite no.) -____________________________________________

City, state, and ZIP code - ______________________________________________________________

Address (number, street, and apt. or suite no.) -____________________________________________

City, state, and ZIP code - ______________________________________________________________

If you or your company utilizes a “Factoring Company” or an “Agency” to manage your payments, please include their

information below:

Name -____________________________________________________________________________

Address (number, street, and apt. or suite no.) -____________________________________________

City, state, and ZIP code - ______________________________________________________________

Tax Payer Information - (EIN, TIN, etc.) - ___________________________________________________

Note – Please be advised that if you are a “Factoring Company” or an “Agency” representing one of TWDC’s payable suppliers with an address

located within the United States, the tax payer information provided above is not furnished to the IRS. It is strictly used for compliance

purposes as a tax i.d. must be on file. By furnishing the requested tax payer information above, will help keep payable accounts from being

blocked during the TWDC audit process.

Form W-9

(Rev. October 2018)

Department of the Treasury

Internal Revenue Service

Request for Taxpayer

Identification Number and Certification

▶

Go to www.irs.gov/FormW9 for instructions and the latest information.

Give Form to the

requester. Do not

send to the IRS.

Print or type.

See Specific Instructions on page 3.

1 Name (as shown on your income tax return). Name is required on this line; do not leave this line blank.

2 Business name/disregarded entity name, if different from above

3 Check appropriate box for federal tax classification of the person whose name is entered on line 1. Check only one of the

following seven boxes.

Individual/sole proprietor or

single-member LLC

C Corporation S Corporation Partnership Trust/estate

Limited liability company. Enter the tax classification (C=C corporation, S=S corporation, P=Partnership)

▶

Note: Check the appropriate box in the line above for the tax classification of the single-member owner. Do not check

LLC if the LLC is classified as a single-member LLC that is disregarded from the owner unless the owner of the LLC is

another LLC that is not disregarded from the owner for U.S. federal tax purposes. Otherwise, a single-member LLC that

is disregarded from the owner should check the appropriate box for the tax classification of its owner.

Other (see instructions)

▶

4 Exemptions (codes apply only to

certain entities, not individuals; see

instructions on page 3):

Exempt payee code (if any)

Exemption from FATCA reporting

code (if any)

(Applies to accounts maintained outside the U.S.)

5 Address (number, street, and apt. or suite no.) See instructions.

6 City, state, and ZIP code

Requester’s name and address (optional)

7 List account number(s) here (optional)

Part I Taxpayer Identification Number (TIN)

Enter your TIN in the appropriate box. The TIN provided must match the name given on line 1 to avoid

backup withholding. For individuals, this is generally your social security number (SSN). However, for a

resident alien, sole proprietor, or disregarded entity, see the instructions for Part I, later. For other

entities, it is your employer identification number (EIN). If you do not have a number, see How to get a

TIN, later.

Note: If the account is in more than one name, see the instructions for line 1. Also see What Name and

Number To Give the Requester for guidelines on whose number to enter.

Social security number

– –

or

Employer identification number

–

Part II Certification

Under penalties of perjury, I certify that:

1. The number shown on this form is my correct taxpayer identification number (or I am waiting for a number to be issued to me); and

2. I am not subject to backup withholding because: (a) I am exempt from backup withholding, or (b) I have not been notified by the Internal Revenue

Service (IRS) that I am subject to backup withholding as a result of a failure to report all interest or dividends, or (c) the IRS has notified me that I am

no longer subject to backup withholding; and

3. I am a U.S. citizen or other U.S. person (defined below); and

4. The FATCA code(s) entered on this form (if any) indicating that I am exempt from FATCA reporting is correct.

Certification instructions. You must cross out item 2 above if you have been notified by the IRS that you are currently subject to backup withholding because

you have failed to report all interest and dividends on your tax return. For real estate transactions, item 2 does not apply. For mortgage interest paid,

acquisition or abandonment of secured property, cancellation of debt, contributions to an individual retirement arrangement (IRA), and generally, payments

other than interest and dividends, you are not required to sign the certification, but you must provide your correct TIN. See the instructions for Part II, later.

Sign

Here

Signature of

U.S. person

▶

Date

▶

General Instructions

Section references are to the Internal Revenue Code unless otherwise

noted.

Future developments. For the latest information about developments

related to Form W-9 and its instructions, such as legislation enacted

after they were published, go to www.irs.gov/FormW9.

Purpose of Form

An individual or entity (Form W-9 requester) who is required to file an

information return with the IRS must obtain your correct taxpayer

identification number (TIN) which may be your social security number

(SSN), individual taxpayer identification number (ITIN), adoption

taxpayer identification number (ATIN), or employer identification number

(EIN), to report on an information return the amount paid to you, or other

amount reportable on an information return. Examples of information

returns include, but are not limited to, the following.

• Form 1099-INT (interest earned or paid)

• Form 1099-DIV (dividends, including those from stocks or mutual

funds)

• Form 1099-MISC (various types of income, prizes, awards, or gross

proceeds)

• Form 1099-B (stock or mutual fund sales and certain other

transactions by brokers)

• Form 1099-S (proceeds from real estate transactions)

• Form 1099-K (merchant card and third party network transactions)

• Form 1098 (home mortgage interest), 1098-E (student loan interest),

1098-T (tuition)

• Form 1099-C (canceled debt)

• Form 1099-A (acquisition or abandonment of secured property)

Use Form W-9 only if you are a U.S. person (including a resident

alien), to provide your correct TIN.

If you do not return Form W-9 to the requester with a TIN, you might

be subject to backup withholding. See What is backup withholding,

later.

Cat. No. 10231X

Form W-9 (Rev. 10-2018)

1) Have you or will you provide services rendered in California?

2) Have you or will you receive rent for property located in California?

3) Have you or will you receive royalties for services originally rendered in California?

4) Have you or will you provide rentals of tangible personal property to be used in California?

If you answer YES or OCCASIONALLY

to 1), 2), 3) or 4), submit a completed California Form 590 or you will be subject to California Nonresident Withholding.

Please check:

OTHER INFORMATION (REQUIRED)

Yes No Occasionally

Yes

No

Occasionally

Yes

No Occasionally

Yes

No

Occasionally

© Disney

Form W-9 (Rev. 10-2018)

Page 2

By signing the filled-out form, you:

1. Certify that the TIN you are giving is correct (or you are waiting for a

number to be issued),

2. Certify that you are not subject to backup withholding, or

3. Claim exemption from backup withholding if you are a U.S. exempt

payee. If applicable, you are also certifying that as a U.S. person, your

allocable share of any partnership income from a U.S. trade or business

is not subject to the withholding tax on foreign partners' share of

effectively connected income, and

4. Certify that FATCA code(s) entered on this form (if any) indicating

that you are exempt from the FATCA reporting, is correct. See What is

FATCA reporting, later, for further information.

Note: If you are a U.S. person and a requester gives you a form other

than Form W-9 to request your TIN, you must use the requester’s form if

it is substantially similar to this Form W-9.

Definition of a U.S. person. For federal tax purposes, you are

considered a U.S. person if you are:

• An individual who is a U.S. citizen or U.S. resident alien;

• A partnership, corporation, company, or association created or

organized in the United States or under the laws of the United States;

• An estate (other than a foreign estate); or

• A domestic trust (as defined in Regulations section 301.7701-7).

Special rules for partnerships. Partnerships that conduct a trade or

business in the United States are generally required to pay a withholding

tax under section 1446 on any foreign partners’ share of effectively

connected taxable income from such business. Further, in certain cases

where a Form W-9 has not been received, the rules under section 1446

require a partnership to presume that a partner is a foreign person, and

pay the section 1446 withholding tax. Therefore, if you are a U.S. person

that is a partner in a partnership conducting a trade or business in the

United States, provide Form W-9 to the partnership to establish your

U.S. status and avoid section 1446 withholding on your share of

partnership income.

In the cases below, the following person must give Form W-9 to the

partnership for purposes of establishing its U.S. status and avoiding

withholding on its allocable share of net income from the partnership

conducting a trade or business in the United States.

• In the case of a disregarded entity with a U.S. owner, the U.S. owner

of the disregarded entity and not the entity;

• In the case of a grantor trust with a U.S. grantor or other U.S. owner,

generally, the U.S. grantor or other U.S. owner of the grantor trust and

not the trust; and

• In the case of a U.S. trust (other than a grantor trust), the U.S. trust

(other than a grantor trust) and not the beneficiaries of the trust.

Foreign person. If you are a foreign person or the U.S. branch of a

foreign bank that has elected to be treated as a U.S. person, do not use

Form W-9. Instead, use the appropriate Form W-8 or Form 8233 (see

Pub. 515, Withholding of Tax on Nonresident Aliens and Foreign

Entities).

Nonresident alien who becomes a resident alien. Generally, only a

nonresident alien individual may use the terms of a tax treaty to reduce

or eliminate U.S. tax on certain types of income. However, most tax

treaties contain a provision known as a “saving clause.” Exceptions

specified in the saving clause may permit an exemption from tax to

continue for certain types of income even after the payee has otherwise

become a U.S. resident alien for tax purposes.

If you are a U.S. resident alien who is relying on an exception

contained in the saving clause of a tax treaty to claim an exemption

from U.S. tax on certain types of income, you must attach a statement

to Form W-9 that specifies the following five items.

1. The treaty country. Generally, this must be the same treaty under

which you claimed exemption from tax as a nonresident alien.

2. The treaty article addressing the income.

3. The article number (or location) in the tax treaty that contains the

saving clause and its exceptions.

4. The type and amount of income that qualifies for the exemption

from tax.

5. Sufficient facts to justify the exemption from tax under the terms of

the treaty article.

Example. Article 20 of the U.S.-China income tax treaty allows an

exemption from tax for scholarship income received by a Chinese

student temporarily present in the United States. Under U.S. law, this

student will become a resident alien for tax purposes if his or her stay in

the United States exceeds 5 calendar years. However, paragraph 2 of

the first Protocol to the U.S.-China treaty (dated April 30, 1984) allows

the provisions of Article 20 to continue to apply even after the Chinese

student becomes a resident alien of the United States. A Chinese

student who qualifies for this exception (under paragraph 2 of the first

protocol) and is relying on this exception to claim an exemption from tax

on his or her scholarship or fellowship income would attach to Form

W-9 a statement that includes the information described above to

support that exemption.

If you are a nonresident alien or a foreign entity, give the requester the

appropriate completed Form W-8 or Form 8233.

Backup Withholding

What is backup withholding? Persons making certain payments to you

must under certain conditions withhold and pay to the IRS 24% of such

payments. This is called “backup withholding.” Payments that may be

subject to backup withholding include interest, tax-exempt interest,

dividends, broker and barter exchange transactions, rents, royalties,

nonemployee pay, payments made in settlement of payment card and

third party network transactions, and certain payments from fishing boat

operators. Real estate transactions are not subject to backup

withholding.

You will not be subject to backup withholding on payments you

receive if you give the requester your correct TIN, make the proper

certifications, and report all your taxable interest and dividends on your

tax return.

Payments you receive will be subject to backup withholding if:

1. You do not furnish your TIN to the requester,

2. You do not certify your TIN when required (see the instructions for

Part II for details),

3. The IRS tells the requester that you furnished an incorrect TIN,

4. The IRS tells you that you are subject to backup withholding

because you did not report all your interest and dividends on your tax

return (for reportable interest and dividends only), or

5. You do not certify to the requester that you are not subject to

backup withholding under 4 above (for reportable interest and dividend

accounts opened after 1983 only).

Certain payees and payments are exempt from backup withholding.

See Exempt payee code, later, and the separate Instructions for the

Requester of Form W-9 for more information.

Also see Special rules for partnerships, earlier.

What is FATCA Reporting?

The Foreign Account Tax Compliance Act (FATCA) requires a

participating foreign financial institution to report all United States

account holders that are specified United States persons. Certain

payees are exempt from FATCA reporting. See Exemption from FATCA

reporting code, later, and the Instructions for the Requester of Form

W-9 for more information.

Updating Your Information

You must provide updated information to any person to whom you

claimed to be an exempt payee if you are no longer an exempt payee

and anticipate receiving reportable payments in the future from this

person. For example, you may need to provide updated information if

you are a C corporation that elects to be an S corporation, or if you no

longer are tax exempt. In addition, you must furnish a new Form W-9 if

the name or TIN changes for the account; for example, if the grantor of a

grantor trust dies.

Penalties

Failure to furnish TIN. If you fail to furnish your correct TIN to a

requester, you are subject to a penalty of $50 for each such failure

unless your failure is due to reasonable cause and not to willful neglect.

Civil penalty for false information with respect to withholding. If you

make a false statement with no reasonable basis that results in no

backup withholding, you are subject to a $500 penalty.

Form W-9 (Rev. 10-2018)

Page 3

Criminal penalty for falsifying information. Willfully falsifying

certifications or affirmations may subject you to criminal penalties

including fines and/or imprisonment.

Misuse of TINs. If the requester discloses or uses TINs in violation of

federal law, the requester may be subject to civil and criminal penalties.

Specific Instructions

Line 1

You must enter one of the following on this line; do not leave this line

blank. The name should match the name on your tax return.

If this Form W-9 is for a joint account (other than an account

maintained by a foreign financial institution (FFI)), list first, and then

circle, the name of the person or entity whose number you entered in

Part I of Form W-9. If you are providing Form W-9 to an FFI to document

a joint account, each holder of the account that is a U.S. person must

provide a Form W-9.

a. Individual. Generally, enter the name shown on your tax return. If

you have changed your last name without informing the Social Security

Administration (SSA) of the name change, enter your first name, the last

name as shown on your social security card, and your new last name.

Note: ITIN applicant: Enter your individual name as it was entered on

your Form W-7 application, line 1a. This should also be the same as the

name you entered on the Form 1040/1040A/1040EZ you filed with your

application.

b. Sole proprietor or single-member LLC. Enter your individual

name as shown on your 1040/1040A/1040EZ on line 1. You may enter

your business, trade, or “doing business as” (DBA) name on line 2.

c. Partnership, LLC that is not a single-member LLC, C

corporation, or S corporation. Enter the entity's name as shown on the

entity's tax return on line 1 and any business, trade, or DBA name on

line 2.

d. Other entities. Enter your name as shown on required U.S. federal

tax documents on line 1. This name should match the name shown on the

charter or other legal document creating the entity. You may enter any

business, trade, or DBA name on line 2.

e. Disregarded entity. For U.S. federal tax purposes, an entity that is

disregarded as an entity separate from its owner is treated as a

“disregarded entity.” See Regulations section 301.7701-2(c)(2)(iii). Enter

the owner's name on line 1. The name of the entity entered on line 1

should never be a disregarded entity. The name on line 1 should be the

name shown on the income tax return on which the income should be

reported. For example, if a foreign LLC that is treated as a disregarded

entity for U.S. federal tax purposes has a single owner that is a U.S.

person, the U.S. owner's name is required to be provided on line 1. If

the direct owner of the entity is also a disregarded entity, enter the first

owner that is not disregarded for federal tax purposes. Enter the

disregarded entity's name on line 2, “Business name/disregarded entity

name.” If the owner of the disregarded entity is a foreign person, the

owner must complete an appropriate Form W-8 instead of a Form W-9.

This is the case even if the foreign person has a U.S. TIN.

Line 2

If you have a business name, trade name, DBA name, or disregarded

entity name, you may enter it on line 2.

Line 3

Check the appropriate box on line 3 for the U.S. federal tax

classification of the person whose name is entered on line 1. Check only

one box on line 3.

IF the entity/person on line 1 is

a(n) . . .

THEN check the box for . . .

• Corporation Corporation

• Individual

• Sole proprietorship, or

• Single-member limited liability

company (LLC) owned by an

individual and disregarded for U.S.

federal tax purposes.

Individual/sole proprietor or single-

member LLC

• LLC treated as a partnership for

U.S. federal tax purposes,

• LLC that has filed Form 8832 or

2553 to be taxed as a corporation,

or

• LLC that is disregarded as an

entity separate from its owner but

the owner is another LLC that is

not disregarded for U.S. federal tax

purposes.

Limited liability company and enter

the appropriate tax classification.

(P= Partnership; C= C corporation;

or S= S corporation)

• Partnership Partnership

• Trust/estate Trust/estate

Line 4, Exemptions

If you are exempt from backup withholding and/or FATCA reporting,

enter in the appropriate space on line 4 any code(s) that may apply to

you.

Exempt payee code.

• Generally, individuals (including sole proprietors) are not exempt from

backup withholding.

• Except as provided below, corporations are exempt from backup

withholding for certain payments, including interest and dividends.

• Corporations are not exempt from backup withholding for payments

made in settlement of payment card or third party network transactions.

• Corporations are not exempt from backup withholding with respect to

attorneys’ fees or gross proceeds paid to attorneys, and corporations

that provide medical or health care services are not exempt with respect

to payments reportable on Form 1099-MISC.

The following codes identify payees that are exempt from backup

withholding. Enter the appropriate code in the space in line 4.

1—An organization exempt from tax under section 501(a), any IRA, or

a custodial account under section 403(b)(7) if the account satisfies the

requirements of section 401(f)(2)

2—The United States or any of its agencies or instrumentalities

3—A state, the District of Columbia, a U.S. commonwealth or

possession, or any of their political subdivisions or instrumentalities

4—A foreign government or any of its political subdivisions, agencies,

or instrumentalities

5—A corporation

6—A dealer in securities or commodities required to register in the

United States, the District of Columbia, or a U.S. commonwealth or

possession

7—A futures commission merchant registered with the Commodity

Futures Trading Commission

8—A real estate investment trust

9—An entity registered at all times during the tax year under the

Investment Company Act of 1940

10—A common trust fund operated by a bank under section 584(a)

11—A financial institution

12—A middleman known in the investment community as a nominee or

custodian

13—A trust exempt from tax under section 664 or described in section

4947

Form W-9 (Rev. 10-2018)

Page 4

The following chart shows types of payments that may be exempt

from backup withholding. The chart applies to the exempt payees listed

above, 1 through 13.

IF the payment is for . . . THEN the payment is exempt

for . . .

Interest and dividend payments All exempt payees except

for 7

Broker transactions Exempt payees 1 through 4 and 6

through 11 and all C corporations.

S corporations must not enter an

exempt payee code because they

are exempt only for sales of

noncovered securities acquired

prior to 2012.

Barter exchange transactions and

patronage dividends

Exempt payees 1 through 4

Payments over $600 required to be

reported and direct sales over

$5,000

1

Generally, exempt payees

1 through 5

2

Payments made in settlement of

payment card or third party network

transactions

Exempt payees 1 through 4

1

See Form 1099-MISC, Miscellaneous Income, and its instructions.

2

However, the following payments made to a corporation and

reportable on Form 1099-MISC are not exempt from backup

withholding: medical and health care payments, attorneys’ fees, gross

proceeds paid to an attorney reportable under section 6045(f), and

payments for services paid by a federal executive agency.

Exemption from FATCA reporting code. The following codes identify

payees that are exempt from reporting under FATCA. These codes

apply to persons submitting this form for accounts maintained outside

of the United States by certain foreign financial institutions. Therefore, if

you are only submitting this form for an account you hold in the United

States, you may leave this field blank. Consult with the person

requesting this form if you are uncertain if the financial institution is

subject to these requirements. A requester may indicate that a code is

not required by providing you with a Form W-9 with “Not Applicable” (or

any similar indication) written or printed on the line for a FATCA

exemption code.

A—An organization exempt from tax under section 501(a) or any

individual retirement plan as defined in section 7701(a)(37)

B—The United States or any of its agencies or instrumentalities

C—A state, the District of Columbia, a U.S. commonwealth or

possession, or any of their political subdivisions or instrumentalities

D—A corporation the stock of which is regularly traded on one or

more established securities markets, as described in Regulations

section 1.1472-1(c)(1)(i)

E—A corporation that is a member of the same expanded affiliated

group as a corporation described in Regulations section 1.1472-1(c)(1)(i)

F—A dealer in securities, commodities, or derivative financial

instruments (including notional principal contracts, futures, forwards,

and options) that is registered as such under the laws of the United

States or any state

G—A real estate investment trust

H—A regulated investment company as defined in section 851 or an

entity registered at all times during the tax year under the Investment

Company Act of 1940

I—A common trust fund as defined in section 584(a)

J—A bank as defined in section 581

K—A broker

L—A trust exempt from tax under section 664 or described in section

4947(a)(1)

M—A tax exempt trust under a section 403(b) plan or section 457(g)

plan

Note: You may wish to consult with the financial institution requesting

this form to determine whether the FATCA code and/or exempt payee

code should be completed.

Line 5

Enter your address (number, street, and apartment or suite number).

This is where the requester of this Form W-9 will mail your information

returns. If this address differs from the one the requester already has on

file, write NEW at the top. If a new address is provided, there is still a

chance the old address will be used until the payor changes your

address in their records.

Line 6

Enter your city, state, and ZIP code.

Part I. Taxpayer Identification Number (TIN)

Enter your TIN in the appropriate box. If you are a resident alien and

you do not have and are not eligible to get an SSN, your TIN is your IRS

individual taxpayer identification number (ITIN). Enter it in the social

security number box. If you do not have an ITIN, see How to get a TIN

below.

If you are a sole proprietor and you have an EIN, you may enter either

your SSN or EIN.

If you are a single-member LLC that is disregarded as an entity

separate from its owner, enter the owner’s SSN (or EIN, if the owner has

one). Do not enter the disregarded entity’s EIN. If the LLC is classified as

a corporation or partnership, enter the entity’s EIN.

Note: See What Name and Number To Give the Requester, later, for

further clarification of name and TIN combinations.

How to get a TIN. If you do not have a TIN, apply for one immediately.

To apply for an SSN, get Form SS-5, Application for a Social Security

Card, from your local SSA office or get this form online at

www.SSA.gov. You may also get this form by calling 1-800-772-1213.

Use Form W-7, Application for IRS Individual Taxpayer Identification

Number, to apply for an ITIN, or Form SS-4, Application for Employer

Identification Number, to apply for an EIN. You can apply for an EIN

online by accessing the IRS website at www.irs.gov/Businesses and

clicking on Employer Identification Number (EIN) under Starting a

Business. Go to www.irs.gov/Forms to view, download, or print Form

W-7 and/or Form SS-4. Or, you can go to www.irs.gov/OrderForms to

place an order and have Form W-7 and/or SS-4 mailed to you within 10

business days.

If you are asked to complete Form W-9 but do not have a TIN, apply

for a TIN and write “Applied For” in the space for the TIN, sign and date

the form, and give it to the requester. For interest and dividend

payments, and certain payments made with respect to readily tradable

instruments, generally you will have 60 days to get a TIN and give it to

the requester before you are subject to backup withholding on

payments. The 60-day rule does not apply to other types of payments.

You will be subject to backup withholding on all such payments until

you provide your TIN to the requester.

Note: Entering “Applied For” means that you have already applied for a

TIN or that you intend to apply for one soon.

Caution: A disregarded U.S. entity that has a foreign owner must use

the appropriate Form W-8.

Part II. Certification

To establish to the withholding agent that you are a U.S. person, or

resident alien, sign Form W-9. You may be requested to sign by the

withholding agent even if item 1, 4, or 5 below indicates otherwise.

For a joint account, only the person whose TIN is shown in Part I

should sign (when required). In the case of a disregarded entity, the

person identified on line 1 must sign. Exempt payees, see

Exempt payee

code,

earlier.

Signature requirements. Complete the certification as indicated in

items 1 through 5 below.

Form W-9 (Rev. 10-2018)

Page 5

1. Interest, dividend, and barter exchange accounts opened

before 1984 and broker accounts considered active during 1983.

You must give your correct TIN, but you do not have to sign the

certification.

2. Interest, dividend, broker, and barter exchange accounts

opened after 1983 and broker accounts considered inactive during

1983. You must sign the certification or backup withholding will apply. If

you are subject to backup withholding and you are merely providing

your correct TIN to the requester, you must cross out item 2 in the

certification before signing the form.

3. Real estate transactions. You must sign the certification. You may

cross out item 2 of the certification.

4. Other payments. You must give your correct TIN, but you do not

have to sign the certification unless you have been notified that you

have previously given an incorrect TIN. “Other payments” include

payments made in the course of the requester’s trade or business for

rents, royalties, goods (other than bills for merchandise), medical and

health care services (including payments to corporations), payments to

a nonemployee for services, payments made in settlement of payment

card and third party network transactions, payments to certain fishing

boat crew members and fishermen, and gross proceeds paid to

attorneys (including payments to corporations).

5. Mortgage interest paid by you, acquisition or abandonment of

secured property, cancellation of debt, qualified tuition program

payments (under section 529), ABLE accounts (under section 529A),

IRA, Coverdell ESA, Archer MSA or HSA contributions or

distributions, and pension distributions. You must give your correct

TIN, but you do not have to sign the certification.

What Name and Number To Give the Requester

For this type of account: Give name and SSN of:

1. Individual The individual

2. Two or more individuals (joint

account) other than an account

maintained by an FFI

The actual owner of the account or, if

combined funds, the first individual on

the account

1

3. Two or more U.S. persons

(joint account maintained by an FFI)

Each holder of the account

4. Custodial account of a minor

(Uniform Gift to Minors Act)

The minor

2

5. a. The usual revocable savings trust

(grantor is also trustee)

b. So-called trust account that is not

a legal or valid trust under state law

The grantor-trustee

1

The actual owner

1

6. Sole proprietorship or disregarded

entity owned by an individual

The owner

3

7. Grantor trust filing under Optional

Form 1099 Filing Method 1 (see

Regulations section 1.671-4(b)(2)(i)

(A))

The grantor*

For this type of account: Give name and EIN of:

8. Disregarded entity not owned by an

individual

The owner

9. A valid trust, estate, or pension trust

Legal entity

4

10. Corporation or LLC electing

corporate status on Form 8832 or

Form 2553

The corporation

11. Association, club, religious,

charitable, educational, or other tax-

exempt organization

The organization

12. Partnership or multi-member LLC

The partnership

13. A broker or registered nominee

The broker or nominee

For this type of account: Give name and EIN of:

14. Account with the Department of

Agriculture in the name of a public

entity (such as a state or local

government, school district, or

prison) that receives agricultural

program payments

The public entity

15.

Grantor trust filing under the Form

1041 Filing Method or the Optional

Form 1099 Filing Method 2 (see

Regulations section 1.671-4(b)(2)(i)(B))

The trust

1

List first and circle the name of the person whose number you furnish.

If only one person on a joint account has an SSN, that person’s number

must be furnished.

2

Circle the minor’s name and furnish the minor’s SSN.

3

You must show your individual name and you may also enter your

business or DBA name on the “Business name/disregarded entity”

name line. You may use either your SSN or EIN (if you have one), but the

IRS encourages you to use your SSN.

4

List first and circle the name of the trust, estate, or pension trust. (Do

not furnish the TIN of the personal representative or trustee unless the

legal entity itself is not designated in the account title.) Also see Special

rules for partnerships, earlier.

*Note: The grantor also must provide a Form W-9 to trustee of trust.

Note: If no name is circled when more than one name is listed, the

number will be considered to be that of the first name listed.

Secure Your Tax Records From Identity Theft

Identity theft occurs when someone uses your personal information

such as your name, SSN, or other identifying information, without your

permission, to commit fraud or other crimes. An identity thief may use

your SSN to get a job or may file a tax return using your SSN to receive

a refund.

To reduce your risk:

• Protect your SSN,

• Ensure your employer is protecting your SSN, and

• Be careful when choosing a tax preparer.

If your tax records are affected by identity theft and you receive a

notice from the IRS, respond right away to the name and phone number

printed on the IRS notice or letter.

If your tax records are not currently affected by identity theft but you

think you are at risk due to a lost or stolen purse or wallet, questionable

credit card activity or credit report, contact the IRS Identity Theft Hotline

at 1-800-908-4490 or submit Form 14039.

For more information, see Pub. 5027, Identity Theft Information for

Taxpayers.

Victims of identity theft who are experiencing economic harm or a

systemic problem, or are seeking help in resolving tax problems that

have not been resolved through normal channels, may be eligible for

Taxpayer Advocate Service (TAS) assistance. You can reach TAS by

calling the TAS toll-free case intake line at 1-877-777-4778 or TTY/TDD

1-800-829-4059.

Protect yourself from suspicious emails or phishing schemes.

Phishing is the creation and use of email and websites designed to

mimic legitimate business emails and websites. The most common act

is sending an email to a user falsely claiming to be an established

legitimate enterprise in an attempt to scam the user into surrendering

private information that will be used for identity theft.

Form W-9 (Rev. 10-2018)

Page 6

The IRS does not initiate contacts with taxpayers via emails. Also, the

IRS does not request personal detailed information through email or ask

taxpayers for the PIN numbers, passwords, or similar secret access

information for their credit card, bank, or other financial accounts.

If you receive an unsolicited email claiming to be from the IRS,

forward this message to [email protected]. You may also report misuse

of the IRS name, logo, or other IRS property to the Treasury Inspector

General for Tax Administration (TIGTA) at 1-800-366-4484. You can

forward suspicious emails to the Federal Trade Commission at

contact the FTC at www.ftc.gov/idtheft or 877-IDTHEFT (877-438-4338).

If you have been the victim of identity theft, see www.IdentityTheft.gov

and Pub. 5027.

Visit www.irs.gov/IdentityTheft to learn more about identity theft and

how to reduce your risk.

Privacy Act Notice

Section 6109 of the Internal Revenue Code requires you to provide your

correct TIN to persons (including federal agencies) who are required to

file information returns with the IRS to report interest, dividends, or

certain other income paid to you; mortgage interest you paid; the

acquisition or abandonment of secured property; the cancellation of

debt; or contributions you made to an IRA, Archer MSA, or HSA. The

person collecting this form uses the information on the form to file

information returns with the IRS, reporting the above information.

Routine uses of this information include giving it to the Department of

Justice for civil and criminal litigation and to cities, states, the District of

Columbia, and U.S. commonwealths and possessions for use in

administering their laws. The information also may be disclosed to other

countries under a treaty, to federal and state agencies to enforce civil

and criminal laws, or to federal law enforcement and intelligence

agencies to combat terrorism. You must provide your TIN whether or

not you are required to file a tax return. Under section 3406, payers

must generally withhold a percentage of taxable interest, dividend, and

certain other payments to a payee who does not give a TIN to the payer.

Certain penalties may also apply for providing false or fraudulent

information.

Form 590 2018

Name

Name

SSN or ITIN FEIN CA Corp no. CA SOS file no.

Address (apt./ste., room, PO box, or PMB no.)

City (If you have a foreign address, see instructions.) State ZIP code

TAXABLE YEAR

2019

Withholding Exemption Certificate

CALIFORNIA FORM

590

The payee completes this form and submits it to the withholding agent. The withholding agent keeps this form with their records.

Withholding Agent Information

Payee Information

Exemption Reason

Check only one box.

By checking the appropriate box below, the payee certifies the reason for the exemption from the California income tax withholding

requirements on payment(s) made to the entity or individual.

Individuals — Certification of Residency:

I am a resident of California and I reside at the address shown above. If I become a nonresident at any time, I will promptly

notify the withholding agent. See instructions for General Information D, Definitions.

Corporations:

The corporation has a permanent place of business in California at the address shown above or is qualified through the

California Secretary of State (SOS) to do business in California. The corporation will file a California tax return. If this

corporation ceases to have a permanent place of business in California or ceases to do any of the above, I will promptly notify

the withholding agent. See instructions for General Information D, Definitions.

Partnerships or Limited Liability Companies (LLCs):

The partnership or LLC has a permanent place of business in California at the address shown above or is registered with the

California SOS, and is subject to the laws of California. The partnership or LLC will file a California tax return. If the partnership

or LLC ceases to do any of the above, I will promptly inform the withholding agent. For withholding purposes, a limited liability

partnership (LLP) is treated like any other partnership.

Tax-Exempt Entities:

The entity is exempt from tax under California Revenue and Taxation Code (R&TC) Section 23701 ______ (insert letter) or

Internal Revenue Code Section 501(c) _____ (insert number). If this entity ceases to be exempt from tax, I will promptly notify

the withholding agent.

Individuals cannot be tax-exempt entities.

Insurance Companies, Individual Retirement Arrangements (IRAs), or Qualified Pension/Profit-Sharing Plans:

The entity is an insurance company, IRA, or a federally qualified pension or profit-sharing plan.

California Trusts:

At least one trustee and one noncontingent beneficiary of the above-named trust is a California resident. The trust will file a

California fiduciary tax return. If the trustee or noncontingent beneficiary becomes a nonresident at any time, I will promptly

notify the withholding agent.

Estates — Certification of Residency of Deceased Person:

I am the executor of the above-named person’s estate or trust. The decedent was a California resident at the time of death.

The estate will file a California fiduciary tax return.

Nonmilitary Spouse of a Military Servicemember:

I am a nonmilitary spouse of a military servicemember and I meet the Military Spouse Residency Relief Act (MSRRA)

requirements. See instructions for General Information E, MSRRA.

CERTIFICATE OF PAYEE: Payee must complete and sign below.

To learn about your privacy rights, how we may use your information, and the consequences for not providing the requested information,

go to ftb.ca.gov/forms and search for 1131. To request this notice by mail, call 800.852.5711.

Under penalties of perjury, I declare that I have examined the information on this form, including accompanying schedules and

statements, and to the best of my knowledge and belief, it is true, correct, and complete. I further declare under penalties of perjury that

if the facts upon which this form are based change, I will promptly notify the withholding agent.

Type or print payee’s name and title

___________________________________________________ Telephone (_____)___________

Payee’s signature

7061193

Date ______________________

Form 590 Instructions 2018 Page 1

2019 Instructions for Form 590

Withholding Exemption Certificate

References in these instructions are to the California Revenue and Taxation Code (R&TC).

General Information

California Revenue and Taxation Code (R&TC)

Section 18662 requires withholding of income

or franchise tax on payments of California

source income made to nonresidents of

California. For more information, See General

Information B, Income Subject to Withholding.

Registered Domestic Partners (RDP) – For

purposes of California income tax, references

to a spouse, husband, or wife also refer to a

California RDP unless otherwise specified. For

more information on RDPs, get FTB Pub. 737,

Tax Information for Registered Domestic

Partners.

A Purpose

Use Form 590, Withholding Exemption

Certificate, to certify an exemption from

nonresident withholding.

Form 590 does not apply to payments of

backup withholding. For more information,

go to ftb.ca.gov and search for backup

withholding.

Form 590 does not apply to payments for

wages to employees. Wage withholding is

administered by the California Employment

Development Department (EDD). For more

information, go to edd.ca.gov or call

888.745.3886.

Do not use Form 590 to certify an exemption

from withholding if you are a seller of

California real estate. Sellers of California

real estate use Form 593-C, Real Estate

Withholding Certificate, to claim an exemption

from the real estate withholding requirement.

The following are excluded from withholding

and completing this form:

• The United States and any of its agencies or

instrumentalities.

• A state, a possession of the United States,

the District of Columbia, or any of its

political subdivisions or instrumentalities.

• A foreign government or any of its political

subdivisions, agencies, or instrumentalities.

B Income Subject to

Withholding

Withholding is required on the following, but is

not limited to:

• Payments to nonresidents for services

rendered in California.

• Distributions of California source income

made to domestic nonresident partners,

members, and S corporation shareholders

and allocations of California source income

made to foreign partners and members.

• Payments to nonresidents for rents if the

payments are made in the course of the

withholding agent’s business.

• Payments to nonresidents for royalties

from activities sourced to California.

• Distributions of California source income

to nonresident beneficiaries from an estate

or trust.

• Endorsement payments received for

services performed in California.

• Prizes and winnings received by

nonresidents for contests in California.

However, withholding is optional if the total

payments of California source income are

$1,500 or less during the calendar year.

For more information on withholding, get

FTB Pub. 1017, Resident and Nonresident

Withholding Guidelines. To get a withholding

publication, see Additional Information.

C Who Certifies this Form

Form 590 is certified (completed and signed)

by the payee. California residents or entities

exempt from the withholding requirement

should complete Form 590 and submit it

to the withholding agent before payment is

made. The withholding agent is then relieved

of the withholding requirements if the agent

relies in good faith on a completed and signed

Form 590 unless notified by the Franchise Tax

Board (FTB) that the form should not be relied

upon.

An incomplete certificate is invalid and the

withholding agent should not accept it. If the

withholding agent receives an incomplete

certificate, the withholding agent is required

to withhold tax on payments made to the

payee until a valid certificate is received. In

lieu of a completed exemption certificate, the

withholding agent may accept a letter from

the payee as a substitute explaining why they

are not subject to withholding. The letter must

contain all the information required on the

certificate in similar language, including the

under penalty of perjury statement and the

payee’s taxpayer identification number (TIN).

The certification does not need to be renewed

annually. The certification on Form 590

remains valid until the payee’s status changes.

The withholding agent must retain a copy

of the certification or substitute for at least

five years after the last payment to which the

certification applies. The agent must provide it

to the FTB upon request.

If an entertainer (or the entertainer’s business

entity) is paid for a performance, the

entertainer’s information must be provided.

Do not submit the entertainer’s agent or

promoter information.

The grantor of a grantor trust shall be treated

as the payee for withholding purposes.

Therefore, if the payee is a grantor trust and

one or more of the grantors is a nonresident,

withholding is required. If all of the grantors

on the trust are residents, no withholding is

required. Resident grantors can check the

box on Form 590 labeled “Individuals —

Certification of Residency.”

D Definitions

For California nonwage withholding purposes,

nonresident includes all of the following:

• Individuals who are not residents of

California.

• Corporations not qualified through the

California Secretary of State (CA SOS)

to do business in California or having no

permanent place of business in California.

• Partnerships or limited liability companies

(LLCs) with no permanent place of

business in California.

• Any trust without a resident grantor,

beneficiary, or trustee, or estates where the

decedent was not a California resident.

Foreign refers to non-U.S.

For more information about determining

resident status, get FTB Pub. 1031, Guidelines

for Determining Resident Status. Military

servicemembers have special rules for

residency. For more information see General

Information E, Military Spouse Residency

Relief Act (MSRRA), and FTB Pub. 1032, Tax

Information for Military Personnel.

Permanent Place of Business:

A corporation has a permanent place of

business in California if it is organized and

existing under the laws of California or it has

qualified through the CA SOS to transact

intrastate business. A corporation that has

not qualified to transact intrastate business

(e.g., a corporation engaged exclusively in

interstate commerce) will be considered as

having a permanent place of business in

California only if it maintains a permanent

office in California that is permanently staffed

by its employees.

E Military Spouse Residency

Relief Act (MSRRA)

Generally, for tax purposes you are considered

to maintain your existing residence or domicile.

If a military servicemember and nonmilitary

spouse have the same state of domicile, the

MSRRA provides:

• A spouse shall not be deemed to have lost

a residence or domicile in any state solely

by reason of being absent to be with the

servicemember serving in compliance with

military orders.

• A spouse shall not be deemed to have

acquired a residence or domicile in any

other state solely by reason of being there

to be with the servicemember serving in

compliance with military orders.

Domicile is defined as the one place:

• Where you maintain a true, fixed, and

permanent home.

• To which you intend to return whenever you

are absent.

Page 2 Form 590 Instructions 2018

The payee must notify the withholding agent if

any of the following situations occur:

• The individual payee becomes a

nonresident.

• The corporation ceases to have a

permanent place of business in California

or ceases to be qualified to do business

in California.

• The partnership ceases to have a

permanent place of business in California.

• The LLC ceases to have a permanent place

of business in California.

• The tax-exempt entity loses its tax-exempt

status.

If any of these situations occur, then

withholding may be required. For more

information, get Form 592, Resident and

Nonresident Withholding Statement,

Form 592-B, Resident and Nonresident

Withholding Tax Statement, and Form 592-V,

Payment Voucher for Resident and

Nonresident Withholding.

Additional Information

Website: For more information, go to

ftb.ca.gov and search for

nonwage.

MyFTB offers secure online tax

account information and services.

For more information, go to

ftb.ca.gov and login or register

for MyFTB.

Telephone: 888.792.4900 or 916.845.4900,

Withholding Services and

Compliance phone service

Fax: 916.845.9512

Mail: WITHHOLDING SERVICES AND

COMPLIANCE MS F182

FRANCHISE TAX BOARD

PO BOX 942867

SACRAMENTO CA 94267-0651

For questions unrelated to withholding, or

to download, view, and print California tax

forms and publications, or to access the TTY/

TDD numbers, see the Internet and Telephone

Assistance section.

A military servicemember’s nonmilitary spouse

is considered a nonresident for tax purposes

if the servicemember and spouse have the

same domicile outside of California and the

spouse is in California solely to be with the

servicemember who is serving in compliance

with Permanent Change of Station orders.

California may require nonmilitary spouses

of military servicemembers to provide proof

that they meet the criteria for California

personal income tax exemption as set forth in

the MSRRA.

Income of a military servicemember’s

nonmilitary spouse for services performed

in California is not California source income

subject to state tax if the spouse is in California

to be with the servicemember serving in

compliance with military orders, and the

servicemember and spouse have the same

domicile in a state other than California.

For additional information or assistance in

determining whether the applicant meets the

MSRRA requirements, get FTB Pub. 1032.

Specific Instructions

Payee Instructions

Enter the withholding agent’s name.

Enter the payee’s information, including the

TIN and check the appropriate TIN box.

You must provide a valid TIN as requested

on this form. The following are acceptable

TINs: social security number (SSN); individual

taxpayer identification number (ITIN); federal

employer identification number (FEIN);

California corporation number (CA Corp no.);

or CA SOS file number.

Private Mail Box (PMB) – Include the PMB

in the address field. Write “PMB” first, then

the box number. Example: 111 Main Street

PMB 123.

Foreign Address – Follow the country’s

practice for entering the city, county, province,

state, country, and postal code, as applicable,

in the appropriate boxes. Do not abbreviate the

country name.

Exemption Reason – Check the box that

reflects the reason why the payee is exempt

from the California income tax withholding

requirement.

Withholding Agent Instructions

Do not send this form to the FTB. The

certification on Form 590 remains valid until

the payee’s status changes. The withholding

agent must retain a copy of the certificate or

substitute for at least five years after the last

payment to which the certificate applies. The

agent must provide it to the FTB upon request.

Internet and Telephone Assistance

Website: ftb.ca.gov

Telephone: 800.852.5711 from within the

United States

916.845.6500 from outside the

United States

TTY/TDD: 800.822.6268 for persons with

hearing or speech disability

711 or 800.735.2929 California

relay service

Asistencia Por Internet y Teléfono

Sitio web: ftb.ca.gov

Teléfono: 800.852.5711 dentro de los

Estados Unidos

916.845.6500 fuera de los

Estados Unidos

TTY/TDD: 800.822.6268 para personas con

discapacidades auditivas

o de habla

711 ó 800.735.2929 servicio de

relevo de California

Tax Identification Number:

ID#:

Supplier Name: Date:

State Registration # State Registration #

Alabama AL

New Jersey

NJ

Alaska AK

New Mexico

NM

Arizona AZ

New York

NY

Arkansas AR

North Carolina NC

California CA

North Dakota ND

Colorado CO

Ohio OH

Connecticut CT

Oklahoma OK

Delaware DE

Oregon OR

District of Columbia DC

Pennsylvania PA

Florida FL

Rhode Island RI

Georgia GA

South Carolina SC

Hawaii HI

South Dakota SD

Idaho ID

Tennessee TN

Illinois IL

Texas TX

Indiana IN

Utah UT

Iowa IA

Vermont VT

Kansas KS

Virginia VA

Kentucky KY

Washington WA

Louisiana LA

West Virginia WV

Maine ME

Wisconsin WI

Maryland MD

Wyoming WY

Massachusetts MA

Michigan MI

Minnesota MN

Puerto Rico

Mississippi MS

Missouri MO

Montana MT

Nebraska NE

Nevada NV

PR

New Hampshire NH

Canada

British Columbia

Saskatchewan

Quebec

Not Registered in any State

Under

p

enalties of

p

erjury,

I

certify that the information on this form is true and correct.

Printed Name:

Signature:

X

Title:

Phone:

Fax: E-Mail:

Supplier Sales/Use Tax Status

Disney Use Only

Phone:

Date:

CA

BC

QC

SK

Manitoba MB

POHDVHLQGLFDWHZKLFKVWDWHV\RXUFRPSDQ\LVGRLQJEXVLQHVVandLVregistered to collect state sales/use tax

•

If you indicate your company is registered i

n a particular state where you ship product to or perform services

in—and taxes are appropriately charged, our policy is to pay the appropriate tax

to your company

•

If you indicate your company is QRWregistered in a particular state where you ship product to or perform services

in—and taxes are QRWcharged by your company, our policy is to accrue and remit the taxes, if appropriate

Alberta

AB

New Brunswick

NB

New Foundland

NF

Northwest Territories

NT

Nova Scotia

NS

Ontario

ON

Prince Edward Island

PE

Yukon Territory

YT

A1 Revised 06.14

©Disney

✔

✔

'LVQH\8VH2QO\

(OHFWURQLF7UDQVDFWLRQV

Disney has contracted with Ariba (NASDAQ: ARBA—www.ariba.com) to provide a technology solution for electronic

transactions—Purchase Orders and Invoices—that integrate directly with Disney’s SAP system. These electronic

transactions utilize the Ariba Supplier Network (ASN) to connect Disney with its Suppliers. The use of the ASN is at

Disney’s discretion, based on the types of transactions we do with your company.

Registration on the Ariba Network is not required. Registering does not assure your use of the Network or com

plete

y

our Disney setup. If your company is chosen to use the ASN, you will receive e-Mail notification once your account is activated.

(OHFWURQLFWUDQVDFWLRQVDUHEHQHILFLDOWRERWK'LVQH\DQGLWV6XSSOLHUV

• Purchase Orders—Suppliers select the method they wish to use to receive Purchase Orders—via a website, Fax, e-Mail, or

integrated with an order entry system

• Invoicing—Purchase Orders can be “flipped” into Invoices or Invoices can be created and sent to Disney electronically—

eliminating paper documents and associated handling/postage costs

• Status—Suppliers have online visibility to current Invoice and payment status and remittance information

• Dynamic Discounting—An optional arrangement where a Supplier receives accelerated payments in exchange for providing

Disney a negotiated discount

• Consistency—One way to do business across all Disney Business Units

7RVHOIUHJLVWHUIRUDQ$ULED1HWZRUNDFFRXQW

• Go to

https://supplier.ariba.com

• Click on the “Register as New Supplier” Link

• Complete the information required, and click on the “Submit” button

Ariba Network ID (ANID) _______________________________________ New Account Existing Account

Company Name ______________________________________________________________________________

7UDQVDFWLRQ$XWRPDWLRQ

ID#

'LUHFW'HSRVLW$&+

ACH payment distribution is required unless contractual obligations specify check payment.

&RPSOHWLQJWKHLQIRUPDWLRQEHORZDXWKRUL]HV'LVQH\:RUOGZLGH6KDUHG6HUYLFHVWRPDNH$&+3D\PHQWV

Supplier Name: ______________________________________ Bank Name:________________________________________

Bank Address: ________________________________________ City: _____________________State: ______ Zip: _______

___

ABA Routing #: _______________________ Account #: _________________________________________________

After a Supplier is created in the Disney Supplier Management Portal, the Supplier is responsible for making any

changes/updates to the following information: address, telephone number, fax number, email address, contact name

and any bank account related information.

We do not have the capability for Direct Deposit.

The above ACH Payment instructions are authorized (unless declined above) and the terms and conditions stated in

this agreement are accepted by:

Signature ;__________________________________ Title:____________________________________ Date _______________

Printed Name: ________________________________Remit e-Mail Address:___________________________________________

If the Ariba Supplier Network will not be an effective solution, please indicate an alternative and the reason:

Solution: Front of House/ISTRAT ERS Upload Other _________________________________________________

Reason: Retainage/Deposit Required Multiple Delivery Address

Limit POs w

/ Unknown Acct. Assignment

'LVQH\%XVLQHVV8QLW8VH2QO\

Note: A yearly Supplier membership fee may be

associated with ASN use. The fee structure is

based on annual Invoice volume.

Complete details and requirements of the ASN Supplier membership

program may be found at: http://ariba.com/suppliermembership.

(As it appears on the Ariba Network)

Checking

Savings

9-Digit

The Walt Disney Company, its affiliates and subsidiaries are committed to making diverse business enterprises an

important part of our sourcing and procurement activities.

The information collected below allows us to track our certified (or “qualified”) diverse Suppliers.

Supplier Name_________________________________________________ Date ________________________

Diverse (Rev. 10-08) © Disne

y

Is the company a publicly-owned business in which at least 51% of the stock is owned by:

Minority Group Members

Yes No Women Yes No Decline to Answer

Is the company a subsidiary which is wholly owned by a parent corporation, but only if at least 51% of the voting

stock of the parent corporation is owned by:

Minority Group Members

Yes No Women Yes No Decline to Answer

Is the company a joint venture in which at least 51% of the joint venture's management and control ("management"

means those persons actively involved in the day-to-day management of the business and not merely holding the

designation of officers or directors, and "control" means exercising the power to make policy decisions) and

earnings are held by:

Minority Group Members

Yes No Women Yes No Decline to Answer

Is the company a business in which the management and control the daily operations is done by:

Minority Group Members

Yes No Women Yes No Decline to Answer

Is the company a sole proprietorship at least 51% owned by:

Minority Group Members

Yes No Women Yes No Decline to Answer

Please indicate Minority Group Members:

Asian Pacific American—A person with origins in Burma, Thailand, Malaysia, Indonesia, Singapore, Brunei,

Japan, China, Taiwan, Laos, Cambodia, Vietnam, Korea, The Philippines,

U.S. Territory of the

Pacific

Islands (Republic of Palau), Republic of the Marshall Islands, Federated State of Micronesia,

the

Comm

onwealth of the North Mariana Islands, Guam, Samoa, Macao, Fiji, Tonga, Kiribati, Tuvalu, or Nauru

Subcontinent Asian American—A person with origins in India, Pakistan, Bangladesh, Sri Lanka,

Bhutan, the Maldives Islands, or Nepal

Hispanic or Latino American—A person of Cuban, Mexican, Puerto Rican, South or

Central American, or other Spanish culture or origin regardless of ra

ce

Native Hawaiian or Other Pacific Islander—A person having origins in any of the peoples