Finance and Economics Discussion Series

Divisions of Research & Statistics and Monetary Affairs

Federal Reserve Board, Washington, D.C.

The Macroeconomic Effects of the Federal Reserve’s

Unconventional Monetary Policies

Eric M. Engen, Thomas Laubach, and David Reifschneider

2015-005

Please cite this pap er as:

Engen, Eric M., Thomas Laubach, and David Reifschneider (2015). “The Macroeconomic

Effects of the Federal Reserve’s Unconventional Monetary Policies,” Finance and Economics

Discussion Series 2015-005. Washington: Board of Governors of the Federal Reserve System,

http://dx.doi.org/10.17016/FEDS.2015.005.

NOTE: Staff working papers in the Finance and Economics Discussion Series (FEDS) are preliminary

materials circulated to stimulate discussion and critical comment. The analysis and conclusions set forth

are those of the authors and do not indicate concurrence by other members of the research staff or the

Board of Governors. References in publications to the Finance and Economics Discussion Series (other than

acknowledgement) should be cleared with the author(s) to protect the tentative character of these papers.

Page1of54

TheMacroeconomicEffectsoftheFederalReserve’s

UnconventionalMonetaryPolicies*

EricEngen,ThomasLaubach,andDaveReifschneider

FederalReserveBoard

January14,2015

Abstract

Afterreachingtheeffectivelowerboundforthefederalfundsrateinlate2008,theFederalReserve

turnedtotwounconventionalpolicytools—quantitativeeasingandincreasinglyexplicitandforward‐

leaningguidanceforthefuturepathofthefederalfundsrate—inordertoprovideadditionalmonetary

policyaccommodation.Weuse

surveydatafromtheBlueChipEconomicIndicatorstoinferchangesin

private‐sectorperceptionsoftheimplicitinterestraterulethattheFederalReservewouldusefollowing

liftofffromtheeffectivelowerbound.Usingourestimatesofthechangesovertimeinprivate

expectationsfortheimplicitpolicyrule,

andestimatesoftheeffectsoftheFede ral Reserve’s

quantitativeeasingprogramsontermpremiumsderivedfromotherstudies,wesimulatetheFRB/US

modeltoassesstheactualeconomicstimulusprovided byunconventionalpolicysinceearly2009.Our

analysissuggeststhatthenetstimulustorealactivityandinflation waslimited

bythegradualnatureof

thechangesinpolicyexpectationsandtermpremiumeffects,aswellasbyapersistentbeliefonthe

partofthepublicthatthepaceofreco verywouldbemuchfasterthanprovedtobethecase.Our

analysisimpliesthatthepeakunemploymenteffect—subtracting

1¼percentagepointsfromthe

unemploymentraterelativetowhatwouldhaveoccurredintheabsenceoftheunconventionalpolicy

actions—doesnotoccuruntilearly201 5,whilethepeakinflationeffect—adding½percentagepointto

theinflationrate—isnotanticipateduntilearly2016.

JELclassification:E5

Keywords:federalfundsrate,

forwardguidance,large‐scaleassetpurchases,monetarypolicyreaction

function,zerolowerbound

____________________________

*Theviewsexpressedinthispaperarethoseoftheauthorsanddonotnecessarilyreflecttheviewsof

othersattheFederalReserveBoardorintheFederalReserveSystem.WethankJim

Clouse,BillEnglish,

RefetGürkaynak,MikeKiley,DavidLebow,EdNelson,andseminarparticipantsattheEuropeanCentral

BankandtheBankofFranceforhelpfulcomments.

Page2of54

I. Introduction

Bytheendof2008,theFederalReserve’sconventionalmonetarypolicytool,thefederalfundsrate,was

atitseffectivelowerboundastheeconomywasinthemidstofafinancialcrisisanddeeprecession.In

thesecircumstances,theFederalOpenMarketCommittee

(FOMC)turnedtotwounconventionalpolicy

tools—quantitativeeasingprogramsandincreasinglyexplicitand forward‐leaningguidanceforthe

futurepathofthefederalfundsrate—inordertoprovideadditionalmonetarypolicyaccommodationto

helpendtherecessionandstrengthentheeconomicrecovery.

1

Theseunconventionalpolicyactions

wereintendedtoputdownwardpressureonreallonger‐terminterestratesandmoregenerallyto

improveoverallfinancialconditions,includingbolsteringpricesforcorporateequitiesandresidential

properties.Morefavorablefinancialconditionswould,inturn,helpboostaggregatedemandandcheck

undesirabledisinflationarypressuresby

providingincreasedsupportforconsumerspending,

construction,businessinvestment,andnetexports.

AsizablenumberofstudieshaveinvestigatedthefinancialmarketeffectsoftheFOMC’sunconventional

actions,especiallywithregardtotheFederalReserve’sassetpurchases,andfoundnoticeableeffects,

onbalance,onlong‐terminterestrates.

2

Bycontrast,therehavebeenrelativelyfewstudiesofthe

effectsoftheseactionsonrealactivityandinflation,andthisworkhasfocusedalmostexclusivelyon

macroeconomiceffectsarisingonlyfromthereductionsintermpremiumscausedbylarge‐scaleasset

purchases.

3

Forthesereasons,relativelylittleisknownaboutthemacroeconomicstimulusprovidedby

theeffectsoftheFOMC’spost‐crisisforwardguidanceandassetpurchasesonexpectationsforthe

futurepathofshort‐terminterestrates,norhowthoseexpectationaleffectsmayhaveinteractedwith

termpremiumshifts.Acentral

themeofthispaperisthatthetwotypesofpolicyactionsarehighly

interdependent,andthattheirmacroeconomiceffectsthusneedtobeevaluatedjointly.Intryingto

gaugethemacroeconomiceffectsofunconventionalmonetarypoliciessincelate2008,wetakeinto

accountthemarkedevolutionovertimeofthe

public’sexpectationsforbothfuturemonetar ypolicy

andtheoveralleconomy;thesefactors,asouranalysiswillshow,haveanimportantbearingonthe

actualmonetarypolicystimulusprovidedbyforwardguidanceandquantitativeeasinginrecentyears.

Thenextsectionofourpaperprovidesasummaryoftheunconventional

monetarypolicyactionstaken

bytheFederalReservesincelate2008.Thethirdsectionpresentsourmethodologyandassessmentof

howprivate‐sectorexpectationsaboutmonetarypolicyevolvedfromearly2009throughlate2013.In

particular,weusesurveydatafromtheBlueChipEconomicIndicatorstoinferthegradualchanges

that

havetakenplacesinceearly2009inprivate‐sectorperceptionsoftheFOMC’simplicitpolicyrule—that

is,thewayinwhichshort‐terminterestrateswouldbeadjustedinresponsetomovementsinreal

activityandinflation.ThefourthsectiondiscussestheotherchanneloftheFOMC’sunconventional

policy

actions,theestimatedeffectsoftheFederalReserve’squantitativeeasingprogramsonthe

trajectoriesofthetermpremiumsembeddedinlonger‐terminterestrates.Withtheseestimatesof

expectationaleffectsandtermpremiumshiftsinhand,weareinapositiontoscoretheactualstimulus

1

Althoughforwardguidanceforthefederalfundsratehadbeenusedinthepast,policymakersstillconsideredthe

natureofitsrecentusetobeunconventionalornontraditional;seeBernanke(2012),forexample.

2

ThesestudiesincludeBauerandRudebusch(2012),D’Amico,English,Lopez‐SalidoandNelson(2013),D’Amico

andKing(2013),Gagnonetal(2011),HamiltonandWu(2012),JoyceandTong(2013),KrishnamurthyandVissing‐

Jorgensen(2011),LiandWei(2013),MeaningandZhu(2011),Neely(2010),Rosa(2012),Rogers,Scottiand

Wright

(2014),andSwanson(2011).

3

ThesestudiesincludeChen,Curdia,andFerrero(2011),Chungetal(2012),BaumeisterandBenati(2013),Gertler

andKaradi(2013),andWealeandWieladek(2014).

Page3of54

torealactivityandinflationprovidedbyunconventionalpolicysinceearly2009,conditionalonsome

modelofthemacroeconomy.ForthispurposeweusetheFRB/USmodel,whoseproperties are

discussedinthefifthsection.Thesixthsectionthensummarizesresultsfromcounterfactualsimulations

ofFRB/US

designedtoscoretheactualmacroeconomicstimulusprovidedbytheFOMC’spost‐crisis

forwardguidanceandassetpurchases;animportantfeatureofthisexerciseistheuseofalternative

specificationsofthemodelinordertoaddressimportantuncertaintiesaboutthecurrentdynamicsof

theeconomy.Weconcludewithsomeobservations

aboutthepotentialimplicationsofouranalysisfor

theefficacyofmonetarypolicyintheeventtheeconomyweretoagainexperienceadeep and

prolongedslump.

Severalkeyfindingsemergefromouranalysis.Intheyearsfollowingtherecessionandfinancialcrisis,

wefindthatprivate‐sectorforecastersgradually

cametoperceivethattheFOMCinthefuturewould

pursueasignificantlymoreaccommodativepolicythantheyhadanticipatedatthestartofthecrisis,in

thesensethattheyrevisedupmarkedlyovertimetheirestimateoftheFOMC’sresponsivenessto

economicslack.Thischangeinpublicperceptionsof

theFOMC’simplicitpolicyrule—whichwe

estimateputconsiderabledownwardpressureonreallong‐terminterestratesovertime,overand

aboveanyeffectsassociatedwithchangesintheunderlyingoutlookforrealactivityandinf lation—

presumablyoccurredinresponsetotheFederalReserve’squantitativeeasingandincreasinglyforceful

forwardguidance

forthefederalfundsrate.Togetherwiththedownwardpressureontermpremiums

associatedwithassetpurchases,theseexpectationaleffectsappeartohaveeasedfinancialconditions

appreciablyrelativetowhattheyotherwisewouldhavebeen,therebyprovidingappreciablesupportto

theeconomicrecoveryovertime.However,ouranalysisalsoshows

thatthenetstimulustorealactivity

andinflationwaslimitedbythegradualnatureofthechangesinpolicyexpectationsandtermpremium

effects,aswellasbyapersistentbeliefonthepartofthepublicthatthepaceofrecoverywouldbe

muchfasterthanprovedtobe

thecase.Partlyforthesereasons,andpartlybecauseoftheinherent

lagsinthemonetarytransmissionmechanism,ouranalysisimpliesthatthemacroeconomiceffectsof

theFOMC’spastunconventionalpolicyactionshaveprobablyyettomanifestthemselvesinfull.In

particular,weestimatethatthepeakunemploymenteffect—subtracting1.2

percentagepointsfromthe

unemploymentraterelativetowhatwouldhaveoccurredintheabsenceoftheunconventionalpolicy

actions—doesnotoccuruntilearly201 5,whilethepeakinflationeffect—adding0.5percentagepointto

theinflationrate—isnotanticipateduntilearly2016.

II. TheFederalReserve’sUnconventionalMonetaryPolicies

After

thefederalfundsratereacheditseffectivelowerbound,theFOMCturnedtotheunconventional

strategyofusingbothquantitativeeasing(QE)alongwithincreasinglyexplicitandforward‐leaning

guidanceaboutthefederalfundsratetoprovideadditionalpolicyaccommodation.

4

Inthefirstpartof

thissection,weprovideabriefsummaryofhowbothapproachesevolvedovertime.Afterthat,we

reviewthegeneralimplicationsoftheseactionsforfinancialmarketexpectationsandotherfactors.

4

OtherunconventionalactionstakenbytheFederalReserveduringthisperiodincludedseveralspecialcredit

programsthatwereintendedtoimprovethefunctioningoffinancialmarkets,alongwiththeintroductionof

macroeconomic“stresstests”forthelargestbankstoverifythattheyhadsufficientcapital.Bothprograms

probablyhelpedto

supporteconomicactivityduring2009andearly2010tosomedegreebyenhancingtheflowof

creditandbyincreasingthepublic’sconfidenceinthebankingsystemandthebroadereconomy.Wehavenot

triedtoincorporatetheseprogramsintoouranalysis,however,becauseofthedifficultiesinaccessingtheireffects

usingmacroeconometricmodels.

Page4of54

Summaryofunconventionalpolicyactionssincelate2008

TheFOMC’sQEprogramsweremostlycomprisedoflarge‐scaleassetpurchases(LSAPs)oflonger‐term

Treasuryandagencymortgage‐backedsecurities(MBS),butalsoincludedthematurityextension

program(MEP);thevariousstagesoftheseQEpolicy

actionsaresummarizedinTable1.Cumulatively,

theFederalReserve’sholdingsofTreasurynotesandbondsalongwithagencyMBSandagencydebt

rosefromaround$500billionpriortothefinancialcrisistoover$4trillionwhenthemost‐recentLSAP

programconcludedinOctober2014.Thecounterpartonthe

liabilitysideoftheFederalReserve’s

balancesheetwasasubstantialincreaseinitsshort‐termliabilities(primarilybankreserves).

5

TheLSAPs

andMEPsmateriallylengthenedtheaveragedurationofthesecuritiesheldbytheFederalReserve,and

thusreducedtheaveragedurationofTreasuryandagencysecuritiesheldbythepublic,relativetowhat

otherwisewouldhaveoccurred.

6

AssummarizedinTable2,theFOMCalsobeganprovidingforwardguidanceforthefuturepathofthe

federalfundsrateinlate2008.However,theinitialguidanceonlyadvisedthat“weakeconomic

conditionsarelikelytowarrantexceptionallylowlevelsofthefederalfundsrateforsometime;”such

limitedguidancewasnotmarkedlydifferentfromthatemployedbytheFOMCin2003and2004.

Althoughthewords“sometime”werereplacedby“anextendedperiod”inearly2009,neitherphrase

providedtheprivatesectorwithmuchspecificityabouteitherthelikelydateofliftoffofthefederal

funds

rateortheeconomicconditionsthatwouldtriggerit.Asaresult,thepublicmighthave

reasonablyinterpretedtheguidanceasconsistentwiththeFOMC’saveragehistoricalbehavior,given

theseverityoftherecessionandtheprojectionsoffuturerealactivityandinflationmadeatthetime,

ratherthanassignaling

anyintentionoftheFOMCtodepartfromitsusualpolicyreactionfunction.

Thespecificityofforwardguidancechangedwith thereleaseoftheAugust2011statementbythe

FOMC,inwhichtheCommitteenotedthateconomicconditionswouldlikely“warrantexceptionallylow

levelsofthefederalfundsrateat

leastthroughmid‐2013”.

7

TheFOMCcontinuedtoissuesimilar

calendar‐basedguidanceforroughlythenextyearandahalf,althoughtheciteddateswererevisedto

“late‐2014”attheJanuary2012meetingandto“mid‐2015”attheSeptember2012meeting.Suchdate‐

basedguidancehelpedfinancialmarketparticipantsandothers

comparetheirexpectationsforthe

liftoffofthefederalfundsratedirectlytothoseoftheFOMC,andsohadthepotentialtoprompt

revisionsinthepublic’sexpectationsregardingthetimingofliftoffandpossiblythelonger‐runconduct

ofmonetarypolicyaswell.Thatsaid,suchdate‐basedforward

guidancewasprobablydifficultforthe

5

TheFederalReservedidnotholdanyagency‐relateddebtandMBSasoflate2008andheldmorethan$200

billioninshort‐termTreasurybillsjustbeforetherecession.Bylate2014,theFederalReservedidnotholdany

Treasurybillsandhadabout$1.75trillioninagency‐

relatedsecuritiesandalmost$2.5trillioninTreasurynotes

andbonds.TheFederalReservehadacquiredabout19percentoftotalfederalTreasurydebtheldbythepublic

whenthemost‐recentLSAPprogramconcluded,onlysomewhatlargerthanthe15percentshareitheldjustprior

tothelastrecession.

TheFederalReserve’sbalancesheetexpandedsignificantlybecauseoftheLSAPprograms,

buttotalfederaldebtheldbythepublicalsoincreasedsubstantiallyfromabout35percentofGDPin2007to

almost75percentofGDPin2014.

6

TheaveragedurationofthesecuritiesheldintheFederalReserve’sportfolioincreasedfrom1.6yearsjustprior

tothemost‐recentrecessionto6.9yearsneartheendof2014.

7

Thisguidanceappearedtohavebeenasurprisetofinancialmarketparticipants.TheeventstudybyFemia,

Friedman,andSack(2013),forexample,foundthatbothlonger‐terminterestratesandtheforeignexchangevalue

ofthedollardeclined,whileabroadindexofU.S.equityvaluesrose,immediatelyfollowing

thisannouncementof

calendar‐basedforwardguidancebytheFOMC.

Page5of54

publictointerpretbecauseanydifferencesbetweentheFOMC’sliftoffguidanceandprivateforecastsof

liftoffcouldhavereflected,atleastinpart,differencesinforecastsforeconomicactivityandinflation.

TheFOMCeventuallyshiftedawayfromcalendar‐basedguidanceandadoptedamorestate‐contingent

approachattheDecember2012meeting.Inthatmeeting’sstatement,theFOMCannouncedthatit

wouldkeepthefederalfundsrateatitseffectivelowerbound“atleastaslongastheunemployment

rateremainsabove6½percent,inflationbe tweenoneandtwoyearsaheadisprojectedtobeno

more

thanahalfpercentagepointabovetheCommittee’s2percentlonger‐rungoal,andlonger‐terminflation

expectationscontinuetobewellanchored.”SubsequentFOMCstatements releasedthroughlate2013

reiteratedthisguidanceaboutthethresholdsthatwouldneedtobecrossedbeforetheCommittee

wouldconsiderraisinginterestrates,

whileaddingthatthedecisiontotightenwouldalsotakeaccount

ofbroaderlabormarketconditionsandfinancialdevelopments.Anothernoteworthychangeinforward

guidancewasmadeattheDecember2013meeting,whentheCommitteeemphasizedthatthefederal

fundsratewaslikelytoremainatitseffectivelowerbound

wellpastthetimethattheunemployment

ratefellbelow6½percent,especiallyifinflationweretocontinuetorunbelowitslonger‐runtarget

levelof2percentandlonger‐runinflationexpectationsremainedstable.

8

Ofcourse,theforwardguidanceissuedinFOMCstatementswasnottheonlywaytheFederalReserve

mayhaveinfluencedpolicyexpectationsthroughitscommunications.Amongothercommunications

thatprobablyinfluencedtheviewsoffinancialmarketparticipantsandothersintheprivatesectorover

thepastfewyearswerecomments

aboutthefactorslikelytoinf luence future policydecisionsmadeby

individualFOMCparticipantsinspeeches,testimony,pressconferences,andotherforums;theFOMC’s

regularly‐publishedSummaryofEconomicProjectionswithforecastsofthefederalfundsrate,economic

activity,andinflationmadebyindividualFOMCparticipantswithoutattributionsinceJanuary2012;

and

theannualstatementsissuedbytheFOMCsinceJanuary2012aboutitslonger‐rungoalsandpolicy

strategy.Inthisregard,severalspeechesbyYellen(2012a,b,c)areworthhighlightingbecausethey

emphasizedthattheFOMC’sguidanceatthetimeaboutthelikelydateofliftoffwasbroadlyconsistent

with

theprescriptionsofpoliciesthatweremoreaccommodativethanastandardTaylor‐typepolicy

rule.Indeed,Bernanke(2012)notedthatchangestoprivate‐sectorforecastsappearedtoreflect“a

growingappreciationofhowforcefultheFOMCintendstobeinsupportingasustainablerecovery.”

Potentialeffectsofunconventionalpolicyactions

BoththeQEprogramsandtheforwardguidanceoftheFOMCwereintendedtofurtherhelpsupport

economicactivityandcheckundesirabledisinflationarypressuresafterthefederalfundsratehadbeen

loweredtoitseffectivelowerbound.TheQEpolicieswerethoughttoputdownwardpressureonthe

generallevelof

longer‐terminterestratesprimarilybecausetheyreducedtheaveragedurationofthe

TreasurysecuritiesandagencyMBSheldbythepublic,whichinturnwouldcausethepricechargedby

investorsforlendingoverthelongerrun—thetermpremium—todecline .

9

Asaresult,borrowingcosts

8

Asaconvenientcutoffpointforouranalysis,weconsidertheeffectsofFOMCunconventionalpolicyactions

takenthroughtheendof2013only.Ourfocusisonthemacroeconomiceffectsofprovidingadditional

accommodationthroughunconventionalpolicies.WiththeannouncementaftertheDecember2013FOMC

meetingofthefirst

reductioninthepaceofassetpurchases—implying,amongotherthings,thatdownward

pressureontermpremiumswouldstabilizeasthestockoftheFederalReserve’slong‐termsecuritiesholdings

leveledout—weconsideritunlikelythatsubsequentcommunicationshavesoughttoprovideadditional

accommodation.

9

SeeKrishnamurthyandVissing‐Jorgenson(2011),D’Amico,English,Lopez‐Salido,andNelson(2012),andLiand

Wei(2013)fordiscussionsofthismechanism.

Page6of54

forresidentialmortgages,autoloans,businessborrowing,andothertypesoflonger‐termlendingwould

decline,allelseequal;inaddition,arbitrageeffectsimplythatcorporateequitypricesandhomevalues

wouldriseandtherealforeignexchangevalueoftheU.S.dollarwoulddecline.

By

itself,forwardguidanceaboutfuturemonetarypolicyneed notprovidemonetarypolicystimulusto

theeconomy,especiallyifitmerelyconfirmsthepublic’sexistingexpectationsforthecentralbank’s

likelyresponsetomovementsin economicactivityandinflationovertime.

10

Rather,significant

economicstimuluswouldrequirethatfinancialmarketparticipantsandothersrespondtotheguidance

bymarkedlyalteringtheirbeliefsaboutfuturemonetarypolicyinamoreaccommodativedirection.At

issue,then,iswhetherthepublicinterpretedtheguidanceprovidedbytheFOMCsincelate2008asa

credible

signalthat,astheeconomyrecovered,theFederalReserveintendedtokeepthefederalfunds

ratelowerforlongerthanwouldotherwisebeexpectedgiventheFOMC’shistoricalresponsesto

movementsinresourceutilizationandinflation.

11

IfsuchashiftinpublicperceptionsoftheFederal

Reserve’simplicitpolicyreactionfunctiondidinfactoccur,thenitshouldhavecausedexpectationsfor

thefuturepathofshort‐terminterestratestoshif tdownandexpectationsforfutureinflationtomove

up,therebyputtingdownwardpressureon

reallonger‐runinterestratesin the nearterm evenasthe

nominalfederalfundsrateremainedstuckatitseffectivelowerbound.Allowing forarbitrageand

spillovereffectstootherassetmarkets,thischangeinexpectationscouldhavehelpedtoincreasethe

valueofcorporateequities,realestate,andother

formsofwealth,lowertherealforeignexchange

valueofthedollar,andimprovefinancialconditionsmoregeneral ly.

TheFederalReserve’sassetpurchasesalsocouldhavepromptedshiftsinpolicyexpectationsthat

stimulatedtheeconomybeyondwhatlowertermpremiumsbythemselves directlyprovided.

12

Given

theunprecedentedmagnitudeofitsquantitativeeasi ngprograms, suchassetpurchasesmayhave

concretelyanddramaticallydemonstratedtheFOMC’sdesiretoprovideadditionalaccommodation,

despiteaccompanyingconcernsbysomeabouttheeffectivenessandpotentialcostsofexpandingthe

FederalReserve’sbalancesheet.Ifso,theQEprogramspotentiallyboosted

thecredibilityandhence

effectivenessoftheFOMC’sforwardguidancebyhelpingtoconvincefinancialmarketparticipants and

othersthattheFOMCreallywouldbepersistentlymoreaggressivethanpreviouslythoughtinusingall

itspolicytoolstobringtheeconomybacktowardfullemployment,whileperhapsbeingmoretolerant

of

amodesttemporaryovershootininflationaswell.Suchshiftsinpolicyexpectationscausedbythe

QEactionsareextremelydifficult,ifnotimpossible,todisentanglefromchanges inexpectations

associatedwithforwardguidancealone,giventhatbothtypesofunconventionalpolicieswereused

simultaneouslyandprobablyweremutuallyreinforcing.

Forthisreason,weestimatethe

macroeconomiceffectsofthecombina tionofthesetwounconventionalmonetarypolicies.

10

Ofcourse,suchconfirmationsmightreduceuncertaintyabouttheFOMC’sfuturebehavior,andifbydoingso,

financialmarketparticipants,firms,andhouseholdsbecamelessconcernedaboutpotentialriskstotheoutlook,

thentheclarifyingofforwardguidancecouldconceivablyboosteconomicactivitytosomedegree.

11

SeeCampbell,Evans,Fisher,andJustiniano(2012)foradiscussionofthedistinctionbetweenforwardguidance

thatchangesprivateexpectationsbypubliclycommittingtheFOMCtodeviatefromitsusualpolicyreaction

function—whattheycall“Odyssean”forwardguidance—fromforwardguidancethatmaysimplyprovidea

forecastoffuturepolicythat

onlyconfirmsthepublic’sexpectationsthattheFOMCwillfollowitstypicalpolicy

reactionfunction—whattheycall“Delphic”forwardguidance.

12

Inparticular,thispossibilityhasbeennotedbyBauerandRudebusch(2011),Bhattarai,Eggertsson,andGafarov

(2014),andWoodford(2012).

Page7of54

III. MeasuringShiftsinMonetaryPolicyRateExpectations

Thissectiondescribesourprocedureforestimatingchangesinprivate‐sectorexpectationsaboutthe

wayinwhichmonetarypolicymakerswerelikelytorespondtofuturemovementsineconomicactivity,

inflation,andfinancialconditions.Toconstructourestimateswe

usesurveydatafromtheBlueChip

EconomicIndicators.Theco‐movementsoftheeconomicprojectionsreportedintheBlueChipsurvey,

togetherwiththewaysinwhich theseforecastshaverevisedovertime,allowustoinferhowprivate‐

sectorforecasters’beliefsabouttheFOMC’simplicitpolicyreactionfunctionchanged

sincelate2008.In

thisregard,ourmethodologydiffersimportantlyfrompreviousworksuchasCampbelletal.(2012),in

thatthetypicalapproachhasbeentousesurveydatatoinferexpectationsoftemporarydepartures

from“standard”centralbankbehavior(i.e.,shockstoafixedrule),ratherthansystematic

changesto

beliefsabouthowthecentralbankwouldrespondtoeconomicconditions.

Forourpurpose,themostinformativesurveyresultsarethosepublishedeveryMarchandOctober,

whichincludenotonlyquarterlyforecastsofeconomicactivity,inflation,andinterestratesforthe

currentandcomingyear,whicharecollected

everymonth,butalsoforecastsofannualconditions

extendingsixyearsintothefuture.Importantly,theMarchandOctobersurveysalsoreportforecasters’

assessmentsofconditionsinthelongerrun,therebyallowing ustoinferanychangesovertimein

privateassessmentsofthenaturalrateofunemployment, theequilibriumreal

rateofinterest,andthe

FOMC’seffectiveinflationtarget,whicharekeyparametersintheperceivedpolicyreactionfunction.

13

Figure1summarizestheevolutionsince2007oftheBlueChipconsensusprojectionsfortheannual

averageofthe3‐monthTreasurybillrate,theyear‐over‐yearrateofGDPpriceinflation,andthe

averageannualunemploymentrate,togetherwithanimputedconsensusforecastfortheannualoutput

gap.

14

Aftertheeffectivelowerboundforthefederalfundsratewashitinlate2008,privateforecasters

forsometimeprojectedthattheTreasurybillratewouldbeginrisingatarelativelyrapidpacewithina

fewquarters.Startingin2011,however,theprojectedliftoffdatewaspushedfurtherinto

thefuture;in

addition,theexpectedpaceoftighteningafterliftoffdeclinedappreciablywhilethenominallevelof

short‐termratesexpectedtoprevailinthelongrunfellnoticeably.Presumably,theserevisionsinthe

expectedpathofshort‐terminterestratesareexplainedatleastinpartbymarkedrevisions

overtimein

theoutlookforeconomicactivity,asprivateforecastersgraduallycametorealizethatthepaceof

recoveryinthelabormarketandthebroadereconomywouldbemarkedlyslowerthaninitially

anticipatedintheimmediateaftermathoftherecession.Incontrast,revisionsintheoutlookfor

inflation

publishedafterMarch2009appearlesssubstantial,withinflationalwaysprojectedtoconverge

relativelyquicklybackuptoaround2percent.Giventherecentaveragehistoricalwedgebetween

inflationmeasuredusingGDPpricesandinflationmeasuredusingthePCEpriceindex,theout‐yearBlue

13

AlthoughtheBlueChipEconomicIndicatorsreportsupdatedprojectionseachmonth,theforecasthorizonforall

buttheMarchandOctoberreleasesextendsonlytothecomingyear.Asaresult,BlueChipprojectionsreleasedin

theothertenmonthsoftheyearareoflimitedvalueinidentifyingshifts

inprivateforecasters’perceptionsofthe

FOMC’simplicitreactionfunction,particularlyasalmostallforecastsreleasedafterearly2009showedshort‐term

interestratesattheireffectivelowerboundthroughmostifnotallofthefollowingyear.

14

AlthoughtheBlueChipsurveydoesnotcollectforecastsoftheoutputgap,theonespublishedinMarchand

Octoberdoreportprojectionsforthelong‐runleveloftheunemploymentrate—thatis,thenaturalrate.Private

forecasters’implicitprojectionsfortheoutputgapmadeattimetcanthus

beapproximatedas2

∗

,

where

∗

denotestheconsensusprojectionofthenaturalrate,

istheprojectedunemploymentratejyears

ahead,and2istheassumedvalueofthecoefficientinOkun’sLaw.

Page8of54

Chipforecastsappeartobefairlywellalignedwiththelonger‐terminflationobjectiveof2percent

(definedintermsofthePCEpriceindex)thattheFOMCannouncedinearly2012.

15

Inourmodel‐basedevaluationofthequantitativeeffectsofunconventionalpoliciesonrealactivityand

inflationlaterinthepaper,changesinpublicperceptionsoftheFOMC’sreactionfunction—p resumedto

beadirectconsequenceoftheFederalReserve’sforwardguidanceandassetpurchases—areoneofthe

twometricsof

the“impulse”fromunconventionalmonetarypolicy(theotherbeingQE‐relatedshifts in

termpremiums).Togaugethemagnitudeofchangesintheperceivedpolicyruleovertime,weusethe

BlueChipforecaststoinferprivate‐sectorbeliefsabouttheFOMC’slikelyfutureresponsestochangesin

economicconditions.

ThehistoricalbehavioroftheFederalReserveandothercentralbankscanbe

approximatedquitecloselybysimplereactionfunctions,evenifthepolicymakersattheseinstitutions

donotliterallyemployaruletosetthepolicyrate.

16

Consistentwiththatevidence,itisreasonableto

assumethat,attimeperiodt,privateforecastersandothersbasetheirj‐step‐aheadexpectationsfor

short‐terminterestratesonaTaylor‐typeruleofthefollowingform:

(1)

∗

∗

Here,

denotestheprojectednominalshort‐terminterestrate,

∗

istheprojectedlevelofthereal

short‐terminterestrateconsistentwithfullemploymentoverthelongerrun(i.e.,theequilibriumreal

rate),istheprojectedinflationrate,

∗

istheperceivedinflationtargetoftheFOMC,and

isthe

projectedoutputgap.Asnotedabove,theextendedBlueChip surveyprovidesdataonallthetermsin

thisexpressionexceptthecoefficientstobeestimated—αandβ—withthecaveatthatprojectionsof

the3‐monthTreasurybill

ratemustbeusedinplaceofforecastsoftheexpectedfederalfundsrate;we

thinkthisisareasonablesubstitution,giventhehighcorrelationbetweenthetwoseries.

17

Aswritten,equation(1)allowsforshiftsovertimein publicperceptionsoftheFOMC’sresponsiveness

tomovementsinrealactivityandinflatio n.Toprovideabenchmarkofprivateforecasters’beliefsabout

thereactionfunctionpriortothefinancialcrisis,weestimatetheparametersαandβovertheperiod

fromthe

early1990s,whenthelong‐horizonBlueChipforecastsfirstbecomeavailable,totheeveofthe

recessionin2007,treatingbothparametersasfixedcoefficientsinthecontextofapanelregression

involvingpooledBlueChipconsensusprojections ofv a ryinghorizonspublishedatdifferenttimes.

15

TheBlueChipalsoreportsconsensusforecastsfortheoverallCPI,whichmightatfirstglancebethoughtofas

moresimilarinnaturetooverallPCEprices—theFOMC’spreferredmeasureofinflationoverthelongerterm—

thantheGDPpricemeasureweuseinouranalysis.However,insettingmonetary

policy,theFOMChas

traditionallysoughttolookthroughtemporarypricefluctuationsandinsteadfocusonunderlyinginflationtrends

by,amongotherthings,closelymonitoringthegenerallymorepersistentmovementsincorePCEinflationaswell

asmeasuresoflong‐terminflationexpectations.Giventhepronouncedshort‐runeffectsof

transitoryfoodand

energypricefluctuationsontheoverallCPI,researchershavetendedtouseeithercore(CPIorPCE)inflationor

GDPpriceinflationwhenestimatingtheFOMC’sreactionfunction.TheBlueChipsurveydoesnotreportforecasts

forcoreinflation.

16

Inparticular,thisbehaviorhasbeennotedbyTaylor(1993,1999)andTaylorandWilliams(2011).

17

Inouranalysis,thepredictedvalueoftheequilibriumrealinterestrateattimetisassumedtoequalthelong‐

runBlueChipforecastforthenominalTreasurybillratelessthelong‐runprojectionforGDPpriceinflation.

Similarly,theperceivedvalueoftheFOMC’sinflationtargetis

assumedtoequalthelong‐runprojectionforGDP

inflation.

Page9of54

Interestingly,theestimatedparametersareveryclosetothosesuggestedbytheoriginalTaylor(1993)

rule.

18

Bycontrast,onecouldplausiblyexpecttheFederalReserve’sunconventionalpoliciesoverthepastfew

yearstohavegraduallyalteredpublicperceptionsofthefutureresponsivenessoftheFOMCtochanges

ineconomicconditions.Time‐varyingperceptionsoftheFOMC’sresponsetoeconomicconditions

couldtakedifferentforms;theycoul d

alteroneorbothoftheresponsecoefficientsαandβ,orthey

couldhavetemporarilyreducedtheinterceptoftheperceivedpolicy rulebelowthelonger‐run

equilibriumrealrate

∗

.GiventheemphasisplacedonexpectedlabormarketconditionsbytheFOMC

initscommunications,wefocushereontimevariationintheeconomicslackparameterwhilekeepingα

fixedandsettingtherule’sintercepttothesurvey‐impliedlong‐runequilibriumrealrate.Inparticular,

onewouldexpectthevalue

ofβconsistentwiththeBlueChipprojectionstoriseovertime.

19

Accordingly,wedonotpoolresults fromdifferentsurveysinourregressionanalysisforthepost‐

recessionperiodbutinsteadestimateseparatecoefficientsforeachMarchandOctobersurveyreleased

from2009through2013.Giventhatthesurveysreportannualprojectionsforonlythecurrentyear

throughsixyearsahead

(plusanassessmentoflong‐runconditions),thenumberofobservations

employedineachindividualregressionisnecessarilysmall.Toimprovethedegreesoffreedomofthis

exercise,wefixthevalueofαinalltheregressionsat0.5,itsvalueinthestandardTaylorruleand,as

discussedabove,consistent

withtheaveragebehavioroftheFOMCperceivedbyprivateforecastersin

theyearspriortothefinancialcrisis.Duetothecomparativelyminordeviationsofinflationfromthe2

percentobjective,andthefactthatthesedeviationswereexpectedtocloserelativelyquickly,allowing

fortimevariationinthe

coefficientαwouldinanycasenothavehadlargeeffectsontheexpected

futurepathofshort‐terminterestrates

20

Inlightofthelimitednumberofobservations,wealsodonot

considertemporarydeviationsoftheinterceptfromthelong‐runequilibriumrealrate.

Table3summarizestheresultsfromthisregressionanalysis.Whenannualprojectionsatallpublished

forecasthorizonsareincludedintheregression(thefirstcolumn),

theestimatedcoefficien tonthe

outputgaprisesmarkedlyovertime,fromlessthan0.3inthe2009and2010surveystomorethan0.9

intheOctober2013survey.However,theshiftintheparameterestimatesovertime is biased

downwardsincethenear‐termannualprojectionsofthe

Treasurybillrateinmanyofthesurveysare

constrainedbythezerolowerbound(ZLB),whichcausestheactualnear‐termprojectionsofshort‐term

interestratestodeviatefromwhattheunconstraine d policyrulewouldotherwiseprescribebyan

18

Forexample,inapooledsampleofallMarchandOctoberBlueChipsurveystakenfrom1992through2007,the

estimatedcoefficientsforαandβare.517(.184)and.424(.063),respectively.(Standarderrorsinparentheses.)

Inthisregression,dummyvariablesareincludedforthezero‐step‐aheadforecaststocontrol

forthefactthatthe

observationpartlyreflectsactualdata.

19

Inprinciple,perceivedchangestomonetarypolicyintentionscouldmanifestthemselvesasanticipatedfuture

shockstoanunchangedFOMCimplicitpolicyrule,inplaceoforinconjunctionwithchangesintherule’s

coefficients.InouranalysisoftheBlueChipprojections,however,werestrictourselvestocoefficientshiftsfor

reasonsofparsimonyandbecausesuchshiftsbettercapturethesystematicchangesinpolicymanifestedinBlue

Chipprojectionsthatextendsixyearsintothefuture.Incontrast,Campbelletal(2012)useBlueChipquarterly

forecastsforthecurrentandcomingyeartoestimateshockstoanunchangedrule,possibly

becausetheiruseof

shorter‐horizonprojectionswouldnotpermitestimationof time‐varyingpolicyrules.

20

Forexample,iftheinflationcoefficientintheperceivedpolicyrulehasremainedabout0.5,thenthemarginal

effectoftheprojectedinflationgapontheTreasurybillrateisonlyontheorderof25basispointsonaveragein

thefirstyearofprojectionsmadesinceearly2009,

withtheeffectdiminishingrapidlywiththeextensionofthe

forecasthorizonthereafter.

Page10of54

increasingamountovertime.Tomitigatethisproblem,thesecondcolumnofthetablereportsresults

whentheregressionsonlyincludeforecastsinwhichtheprojectedTreasurybillrateisgreaterthan0.3

percentagepoint,acut‐offpointconsistentwithafederalfundsrateabove

itscurrenttargetrangeof0

to25basispoints.(Inpractice,thisscreeninginvolvesdroppingthecurrent‐yearand,inthelater

surveys,theone‐year‐aheadprojections.)Inthiscase,theincreaseovertimeintheestimatedvalueof

βimplicitintheconsensusBlueChipprojectionsiseven

morepronounced,climbingfromabout0.15in

theMarch2009surveyto1.60intheOctober2013survey.Basedontheseresults,onecouldjudgethe

effectivenessoftheFederalReserve’sunconventionalpolicyactionsininfluencingpolicyexpectationsas

considerable,particularlyaftertheFOMCbeganissuingmoreexplicitforwardguidancein

August2011.

Figure2illustratestheimplicationsfortheprojectedtrajectoryofshort‐terminterestratesofthese

inferredshiftsintheexpectedpolicyreactionfunction.Tobegin,theblacklinesshowtheevolutionof

theactualBlueChipprojectionsoftheTreasurybillratepublishedoverthe2009‐2013

period,whilethe

dashedredlinesshowwhatwouldhavebeenprescribedbythes tandardTaylor(1993)ruleconditional

ontheaccompanyingBlueChipprojectionsforeconomicslack,inflation,theequilibriumrealrate,and

theFOMC’slong‐runinflationtarget.Asthefigureshows,privateforecastersinearly2009anticipated

that

short‐terminterestrateswouldbegintorisemuchearlierandfasterthanpredictedbytheTaylor

(1993)rule;thisprojectedrapidtighteningmayhavereflectedforecasters’beliefthattheFOMCwould

bereluctanttokeepthefundsrateatalevelwellbelowanythingseensincethe1930s,even

ifsucha

lowratewasconsistentwithperceptionsoftheFOMC’spastbehaviorasapproximatedbytheTaylor

rule.ThispatternpersisteduntilOctober2011,whentheBlueChipprojectionsbecamereasonably

well‐alignedwiththestandardTaylorrule.Afterthisdate,privateforecastersappearedtoanticipate

thattheFOMC

wouldbemorepatientthanthestandardTaylorruleimpliedforpolicyastheeconomy

recovered,toadegreethatincreaseda ppreciablyovertime.Theestimatedchangesinpolicy

expectationsunderlyingtheBlueChipprojectionsisreasonablywellapproximatedbythebluedashed

line,whichshowsthepolicyprescriptionsfrom

asimpleruleinwhichtheperceivedvalueofβrevises

overtimeasreportedinthesecondcolumnofTable3,resulting—asonewouldexpect—inmuchbetter

trackingperformance.

Nonetheless,therulesestimatedwithannualdatahavedifficultyaccountingforprivateforecasters’

expectationsforthetimingofliftoffasreportedin

both2009surveysandintheMarch2010andthe

March2011surveys.Thesediscrepancies,plustheemphasisplacedinFOMCcommunicationsonthe

conditionsthatwouldwarrantkeepingthefederalfundsratenearzero,suggesttakingacloserlookat

BlueChipprojectionsofunemploymentandinflationatthe

timeofliftoff,asisdoneinTable4.Thefirst

fewcolumnsofthetablesummarizetheconsensusforecastsforeconomicconditionsinthequarter

duringwhichprivateforecastersimplicitlyexpectedthefederalfundsratetofirstriseaboveitseffective

lowerbound.

21

Intheimmediateaftermathofthefina ncialcrisis,privateforecastersanticipatedthat

liftoffwouldoccurinlate2009eventhoughtheunemploymentratewouldstillbeabove9percentand

GDPpriceinflationwouldbeonly1percent.Astimepassed,however,privateforecasterspushedthe

21

AlthoughtheBlueChipEconomicIndicatorssurveydoesnotpublishfundsrateprojections,forecastsofthe3‐

monthTreasurybillratecanbeusedtoinfertheexpectedliftoffdate.Inparticular,thebillrateshouldequalthe

expectedaveragevalueofthe(overnight)federalfundsrateoverthenext

91days,abstractingfromtax

considerationsandtransitorysafe‐haveneffects.Giventhattaxeffectsareessentiallyzerowhentheinterestrates

areverylow,andgiventhatsafe‐havenconcernsarepresumedtobeapproximatelynormalwhentheFederal

Reservebeginsraisingthefederalfundsratetarget,weassumethat

iftheprojectedT‐billratefirstrisesabove0.3

percentinquartert,thenliftoffisexpectedtooccurinquartert+1.Asdiscussedintheappendix,thisassumption

appearsreasonablyconsistentwithfinancialmarketparticipants’forecastsoftheliftoffdateforthefederalfunds

rate.

Page11of54

projecteddatefortheonsetoftighteningfurtherandfurtherintothefuture,presumablyinresponseto

adisappointinglyslowpaceofrecovery,continuedmoderateinflation,asequenceoflarge‐scaleasset

purchaseprograms,andincreasinglyaggressiveforwardguidance.Critically,theyreviseddownsharply

theirexpectations

fortherateofunemploymentthatwouldprevailatlif toff toabout6½percentbylate

2013,alevelbroadlyconsistentwiththeFOMC’sannounce dunemploymentthreshold,whilegradually

revisinguptheirexpectationsfortheaccompanyingrateofinflationtoabout2percent.

22

Holdingthevalueofαconstantat0.5,andassumingthattheFOMCraisesthefederalfundsrateto50

basispointsatliftoff,wecanestimatethevalueofβconsistentwiththeprojectionsofeconomic

conditionsatliftoff(t=LO)inaspecificBlueChipforecastas:

(2)

0.5

∗

0.5

∗

2

∗

⁄

ThefinalcolumnofTable4reportstheresultsfromthiscalibrationexerciseusingtheprojectedvalues

fortheunemploymentrateandinflationatliftoffreportedinthesecondandthirdcolumnsofthetable

andthelong‐runBlueChipforecastsfortheunemploymentrate,inflation,and

therealfundsrate

reportedinthefourththroughsixthcolumns.Acomparisonoftheseresultswiththefinalcolumnof

Table3revealssimilarrevisionsinβovertime.Forexample,theimplicitoutputgapcoefficientatliftoff

climbsfrom0.25intheMarch2009surveyto1.6intheOctober

2013survey,achangealmostidentical

tothatobtainedusingannualprojections.Moreover,mostofthecumulativerevisiontoβoccursafter

early2011,asisthecasewiththeannualestimates.Finally,Figure2illustratesthat,fromtheOctober

2011surveyon,theprescriptionsoftheestimatedliftoffrules(dashed

greenlines)arequitesimilarto

onesgeneratedusingtheestimatedan nualrules(dashedbluelines).Priortothatsurvey,however,it

appearsthatprivateforecastersanticipatedthat thebehavioroftheFOMCwouldbenoticeablymore

accommodativeatthetimeofliftoffthanitwouldbeinthelongerrun.

(Asinthecaseoftheannual‐

basedestimates,theshiftsintheexpectedsensitivityofthefederalfundsratetoslackatthetimeof

liftoffwouldnotbemateriallyalteredifwehadinsteadassumedanaccompanyingdeclineinthe

coefficientontheinflationgap,giventhatprivate

forecastersfromOctober2011onconsistently

expectedinflationtobe closetoitslong‐runlevelatthetimeofliftoff.)

Sofar,wehavemadenoallowanceinouranalysisforthepossibilitythatprivateforecastersmayhave

expectedtheFOMCtobehaveinertially,inthatwehavenot

includedthelaggedTreasurybillrate inour

regressionsasfollows:

(3)

1

∗

∗

22

TheBlueChipforecastsreleasedduring2013,aftertheinitialannouncementofthresholds,mayinfactbemore

consistentwiththeFOMC’sforwardguidancethanimpliedbytheestimatesreportedinTable4becausethelatter

areaffectedbymodestquarterlyimputationerrorsbeginningwiththeOctober2011release.Beginning

withthat

release,privateforecastersanticipatedthatliftoffwouldoccursometimeintheyearfollowingthecomingyear.

BecausetheBlueChipsurveyprovidesquarterlyforecastsforthecurrentandcomingyearonly,theexact

quarterlytimingofliftoffanditsaccompanyingconditionsintheOctober2011releaseandbeyondmust

be

imputedusingannualprojections.Theseimputationsaresomewhatimprecise,particularlywithregardstothe

federalfundsrate,whichissubjecttothenon‐lineareffectivelowerboundandtendstoberaisedindiscretesteps

bytheFOMC.Asaresult,theliftoffdateactuallyanticipatedbyprivateforecasters

couldbeaquarterortwolater

thanreportedinthetable,implyingthattheaccompanyingunemploymentratecouldbeasmuchas¼percentage

pointlower.Theestimatedinflationrateatthetimeofliftoffwouldbelittlechanged,however.

Page12of54

Forforecastspublishedfrom2009through2011,thereappearstobelittleevidenceofinertia.For

forecastspublishedfrom2012on,however,thestoryissomewhatdifferent.Ifλisassumed

toequal0.8onaquarterlyfrequency,andβiscalibratedasshownintheright‐most

columnofTable3,

thentheresultingruledescribes theBlueChipforecastsaboutaswellasthenon‐inertialestimatedrule.

ThetrackingperformanceofthiscalibratedruleisillustratedbytheorangelineinFigure2.

Thereareseveralcaveatstotheresultspresentedhere.First,ouranalysisassumes

thatprivate

forecastersbasetheirprojectionsofshort‐terminterestratesonasimplepolicyruleinvolvingonlythe

outputgap,inflation,andassessmentsoftheequilibriumrealrateandtheFOMC’sinflationtarget.In

practice,however,theirprojectionsmightincorporateotherinfluencesaswell,suchasthecyclical

growth

rateofrealGDP,thehealthoffinancialinstitutions,oraperceptionthateconomy’sequilibrium

realrate(theinterceptintherule)istime‐varying.Second,ourapproximationfortheprojectedoutput

gapimplicitintheBlueChipsurveycouldmisstateprivateforecasters’actualviewsaboutthelikely

trajectoryforfuture

resourceutilization,aswouldoccurifforecastersseethenaturalrateof

unemploymentasvaryingovertheprojectionhorizo nandthereforenotequivalenttotheirprojections

oftheunemploymentrateinthelongerrun,oriftheyanticipatevariabilityintheOkun’sLaw

relationshipperhaps,forexample,relatedtounusual

projectedmovementsintrendlaborforce

participationandtrendpr oductivity.Third,evenifourresultsdoaccuratelygaugetheevolutionofthe

monetarypolicyviewsofprivateforecasters,thoseviewsmaynotconformcloselytotheviewsof

households,firms,andthefinancialmarketsmorebroadly.(Asdiscussedintheappendix,

however,

forecastsmadebyfinancialmarketparticipantsdoseembroadlyconsistentwiththosepublishedin the

BlueChipEconomicIndicators.)Nonetheless, weviewtheresultsaspointingstronglytoamarkedshift

intheperceptionsofprivateforecastersoftheFOMC’swillingnesstofollowahighlyaccommodative

monetarypolicy.

IV.

SpecifyingtheEffectsofFederalReser veQuantitativeEasingonTermPremiums

Inadditiontoestimatingshiftsinperceptionsoftheimplicitpolicyreactionfunction,ouranalysisalso

needstotakeintoaccounttheothermonetary“impulse”fromunconventionalpolicy—thechangesin

termpremiumsassociatedwiththeFederalReserve’squantitativeeasing

programs.Forestimatesof

theseeffects,wedrawontheconsiderablebodyofworkthathasemergedinrecentyearsconcerning

thefinancialmarketeffectsoflarge‐scaleassetpurchases.Usingavarietyoftechniques,anumberof

studiesfindonbalancethattheFOMC’sassetpurchaseshavesucceededinreducing

yieldsonlonger‐

termTreasurysecuritiesandagencyMBSbyanappreciableamount,andsomehavefoundnoticeable

reductionsincorporatebondyields.

23

Inmanyofthesestudies,however,thereportedredu ctionsin

yieldsmayreflectamixofchangedexpectationsaboutthefuturepathofshort‐terminterestratesand

policy‐drivendeclinesin termpremiums.

Forouranalysis,weusethetermpremiumestimatesreportedbyIhrigetal.(2012)becausethose

estimatesarederivedusingamethodologythatallowstheeffectsofshiftsintermpremiumsonlong‐

termTreasuryyieldsduetochangesinquantitativeeasingpoliciestobeisolatedfromotherinfluences,

includingtheeffectsofchangesinexpectationsforthepathofthefederalfundsrate.Indeed,their

resultshaveseveraladvantagesoverotherresearchinthisarea.Toestimatethetermpremiumeffects

23

ThesestudiesincludeBauerandRudebusch(2012),D’Amico,English,Lopez‐SalidoandNelson(2013),D’Amico

andKing(2013),Gagnonetal(2011),HamiltonandWu(2012),JoyceandTong(2013),KrishnamurthyandVissing‐

Jorgensen(2011),LiandWei(2013),MeaningandZhu(2011),Neely(2010),Rosa(2012),Rogers,Scottiand

Wright

(2014),andSwanson(2011);alongwithKiley(2012)andGilchrist,López‐Salido,andZakrajšek(2014).

Page13of54

ofthequantitativeeasingprograms,Ihrigetalrelyheavilyontheempiricalarbitrage‐freeterm

structuremodeldevelopedbyLiandWei(2013).Thismodelpresumestheexistenceofpref erred‐

habitatinvestorsofthesortdescribedbyVayanosandVila(2009),whichinturnimplies

thattheslope

oftheyieldcurveshouldrespondtosu pplyfactorssuchaschangesinthesizeandmaturitystructureof

theoutstandingstockofTreasuryandagencysecuritiessuppliedtothepublic.

24

Ihrigetal.adjustthemethodologyoriginallyemployedbyLiandWeitoscorethetermpremiumeffects

ofLSAP1andLSAP2byusingtheFOMC’snormalizationplansannouncedinmid‐2011,whichlaidoutthe

relationshipbetweenthetimingofliftoffofthefederalfundsratefromthelower

boundontheone

hand,andtheendofreinvestingmaturingassetsfromtheSOMAportfolioandthetimingofassetsales

ontheother.TheycombinethisinformationwithBlueChipexpectationsforthetimingofliftoffto

arriveatmarketexpectationsforthepathofthebalancesheet.

25

Ihrigetal.alsoemploytheLi‐Wei

methodologytoscoretheeffectsofthematurityextensionprogramsthattheFederalReserveinitiated

inSeptember2011andco mpletedinlate2012:ByreducingtheaveragedurationoftheTreasury

securitiesheldbythepublic,MEP1andMEP2putfurthermodest

downwardpressureonterm

premiumsevenasthesizeoftheFederalReserve’sportfolioremainedunchanged.

26

Figure3plotstheIhrigetal.estimatesofthetermpremiumeffectsofthequantitativeeasingprograms.

Theblacklineindicates thatthefirstroundofassetpurchasesisestimatedtohaveloweredtheterm

premiumon10‐yearTreasuryyieldsroughly40basispointsonaverageatthe

startoftheprogramin

early2009.

27

Thereafter,thetermstructuremodelpredictsthatthedownwardpressureontheterm

premiumunderthefirstLSAPprogramwouldbeexpectedtodiminishsteadilyastheaveragematurity

oftheFederalReserve’sholdingsdeclined,thescale oftheeconomyincreased,andthe

contemporaneousBlueChipprojectionsforthedate

ofliftoffofthefederalfundsrate—whichwould

signalthestartofactivebalance‐sheetnormalization—drewnearer.Asindicatedbythegreenline,the

24

UsingmonthlydatafromMarch1994throughJuly2007onvolumesandyieldsofTreasurysecuritiesandagency

MBS,LiandWeifindstrongempiricalsupportforthistheoreticalproposition.Theyalsousetheirestimatedmodel

toinferthetermpremiumeffectsofchangesinthesizeandcompositionof

publicholdingsofTreasurysecurities

andagencyMBSofthesortthatresultedfromthefirsttwoLSAPprograms,andconcludethattheywerequite

large.

25

WhereasLiandWei’sestimatesoftheeffectsofthefirsttwoassetpurchaseprogramswerebasedonthe

assumptionthattheFOMCwouldbeginsellingassetstwoyearsaftertheendofeachprogramandconcludesuch

salesoveraspanofthreeyears,Ihrigetal.tiethe

beginningofsalestotheexpecteddateofliftoffbasedonBlue

Chipsurveyexpectations,whichatthetimewasexpectedtooccursoonerthantwoyearsaftertheconclusionof

eachprogram,therebyreducingthetermpremiumeffects.

26

AnassumptionmaintainedthroughoutouranalysisisthattheTreasurydidnotchangeitsstrategyforthe

maturitycompositionofitsissuanceofnewsecuritiesinresponsetotheFOMC’sassetpurchases.TheTreasury’s

debtmanagementstrategyhadbeenpersistentlyincreasingtheaveragematurityofnewly‐issuedTreasury

securitiessince

around2002.AlthoughtheTreasury’sstrategyhadtheoppositeeffectontheaveragedurationof

outstandingTreasurysecuritiesastheFOMC’sQEpolicies,theTreasuryhadbeguntopursueitsstrategylong

beforethefinancialcrisisandcontinuedwithitevenwiththeFOMC’sdecisiontoexpandthesizeandduration

of

theFederalReserve’ssecurityholdings,whichwasconsistentwiththeTreasury’susualpracticewhenfacedwith

thelargeincreasesinfederalgovernmentborrowingduringthisperiod.Accordingly,themarginaleffectof

quantitativeeasingwasstilltoreducetermpremiumsrelativetowhattheyotherwisewouldhavebeen.(See

Greenwood,

Hansen,Rudolph,andSummers(2014)foramorecriticalviewoftheTreasury’sdebtmanagement

practicewhiletheFederalReservewaspursuingitsQEprograms.)

27

Aportionofthiseffectoccursearlyin2009becausetheFederalReservemadeitsfirstannouncementabout

assetpurchasesattheveryendof2008.Thefullscopeofthefirstassetpurchaseprogramwasnotknownuntil

afterthereleaseoftheFOMCstatementinlateMarch2009.

Page14of54

projectedtrajectoryoftermpremiumeffectsareestimatedtoshiftdownslightlywiththeFOMC’s

announcementthatpaymentsontheFederalReserve’sholdingsofsecurities(particularlyMBS)would

bereinvested,slowingtherateofdeclineinthesizeandaveragedurationofitsportfolio.

Commencementof

asecondroundofassetpurchasesinNovember2010isestimatedtoprompta

furtherdownwardrevisionintheprojectedpath,whichalsoincorporatestheeffectsoftheassets

purchasedunderLSAP1(solidredline).Importantly,theinitialrevisionintermpremiumeffectsatthe

startofLSAP2isfollowedby

furtheronesasBlueChipforecastsforthedateofliftoffarepushedfurther

offintothefuture(thereddashedlines).Finally,theIhrigetalresultsindicatethatthematurity

extensionprogramsfirstincreasedandthenmaintainedthecumulativedownwardpressureonterm

premiumstoabout60basis

throughmid‐2012.

ThethreepurplelinesshowtheextensionoftheIhrigetal.methodologytoincludetheeffectsofthe

thirdroundofassetpurchasesthatbeganinSeptember2012.Theimplementationofthisprogramis

estimatedtohavegreatlymagnifiedthedownwardpressureontermpremiums,bringingit

closeto120

basispointsatthestartoftheprogram.Marketparticipantsinitiallyexpecteditssizetobeabout$1.2

trillion,substantiallysmallerthanthefirstassetpurchaseprogram;nonethelessitseffectswere

substantiallylarger,inpartbecausepurchasesofTreasurysecuritieswereconcentratedinlonger

maturitiesthanthey

hadbeeninLSAP1,andinpartbecausetheexpansionoftheSOMAholdingswas

expectedtolastlongerthantheoriginalpurchasesin2009.Asshownbythefirstdashedline,the

projectedlonger‐runtrajectoryofthecumulativeeffectsfromallassetpurchaseprogramsshifteddown

inresponseto

FOMCcommunicationsindicatingthatitwouldprobablyeschewactivesalesofitsMBS

holdingsonceitbeganshrinkingthesizeofitsbalancesheet,incontrasttotheCommittee’ s previous

guidance.Finally,marketexpectationsgraduallyshiftedtowardtheprogram’sultimatesizeof$1.5

trillion.

Becausedurationeffectsshouldvaryacross

securitiesofdifferentmaturities,theresultsreportedin

Figure3applyonlytothetermpremiumsembeddedin10‐yearTreasuryyields.Simulationsofthe

Li‐Weitermstructuremodelpredictthattheeffectsofthevariousassetpurchaseprogramsontheterm

premiumsembeddedin30‐yearTreasuryyieldsshould

beonaverageonly35percentorsoofthese

estimatedfor10‐yearsecurities;thecorrespondingfigurefor5‐yearTreasurynotesisabout80

percent.

28

V. EstimatingtheMacroeconomicEffectsofUnconven tionalPoliciesUsingFRB/US

HavingquantifiedtheeffectsoftheFederalReserve’sunconventionalpolicyactionsonperceptionsof

itsimplicitpolicyruleandontermpremiums,wenowturntotheissueoftheeffectsoftheseactionson

aggregateeconomicactivityandinflation

overthepastfewyears.Thissectiondiscussesourchoiceofa

structuralmacroeconometricmodelforsimulatingtheresponseoftheeconomytounconventional

policymeasures,andthenpresentsanddiscussesresultsforsomeillustrativepolicyactions.

TheFRB/USmodel

Toquantifythemacroeconomiceffects ofunconventionalpolicies,weneedamacroeconomic

modelthatisstructuralinthesensethatitcanappropriatelycontrolfortheeffectsofpolicy

measuresthroughexpectations.Infact,asouranalysiswillhighlight,expectationsaboutthefuture

courseofpolicyarecriticallyimportantfortheeffectivenessoftheunconventionalpolicyactions

28

WethankMinWeiforprovidinguswiththesefigures.

Page15of54

studiedhere.WhilethisgeneralpointhasbeenappreciatedsinceLucas’(1976)paper,thisissueis

ofparticularrelevanceinthecircumstancesofthepastfewyears,whenthepublichashadtorely

disproportionatelyonpolicyannouncementsforformingexpectationsbecausetherewasnopast

recordofunconventionalpolicyactionsattheZLBtogoby.

Asmentionedearlier,onlyafewstudieshaveexaminedthemacroeconomiceffectsof

unconventionalpoliciesinstructuralmodels.Thesestudiesaremostlyconductedusingdynamic

stochasticgeneralequilibrium(DS GE)modelsbuiltaroundarepresentativehouseholdandassuming

someformoffinancialfriction,suchasinChenetal.(2012)andGertlerandKaradi(2013).Inour

studyweusetheFederalReserveBoard’sFRB/USmodel,whichdepartsfromtheseothermodelsin

certaindimensionsthatwewillbrieflydiscusshere.MoredetailedinformationabouttheFRB/US

modelingeneralisavailableelsewhere.

29

ThreepropertiesofFRB/USinparticularareworthhighlighting.First,theFRB/USmodelfeaturesa

broadarrayoffinancialassetswhosepricescanserveaspotentialtransmissionmechanismsfor

monetarypolicy:Besidestheshort‐terminterestratethatisthe(conventional)toolofmonetary

policy,therearelong‐termTreasurysecuritiesatthreedifferentmaturities,residentialmortgages,

corporatebonds,corporateequity,andtherealtrade‐weightedexchangerate.Thepricesofthese

variousassetsarelinkedtoeachotherviaarbitrageconditionsthatin cludetermandriskpremiums

whicharethemselvesmodeledasendogenousvariables,dependinginmanyinstanceson

expectationsaboutthefuturecyclicalpositionoftheeconomy.InthebaselineversionofFRB/US

usedinthispaper,termpremiumsareaffectedonlybyunconventionalmonetarypolicymeasures,

whereasriskpremiumsonotherassetsareendogenous.Thebroadarrayoffinancialassetsin

FRB/US,andinparticularthecentralroleplayedbyspecificmeasuresoflong‐terminterestrates,

makesthemodelveryusefulforstudyingtheeffectsofunconventionalmonetarypolicy,especially

assetpurchases.Thatsaid,thereliabilityofitssimulationresultsdependsimportantlyonthe

empirical“reasonableness”ofitspredictionsforQE‐relatedspillovereffectsonprivateborrowing

rates,corporateequityprices,andtheexchangerate—somethingthatwewillexamineshortly.

Fromsomeperspectives,theapproachtakeninFRB/USmayhavecertainlimitations:Practicallyall

spendingdecisionsdependonlonger‐termrealinterestrates,therebyassigningequallystrong

effectsonaggregatedemandtochangesintermpremiumsandinexpectedfutureshortrates;and

premiumsaremodelledinreduced‐formratherthanbeingderivedexplicitlyfromfinancial

frictions.

30

Asecondfeatureisthatthereisnorepr esentativeagentintheFRB/USmode l;insteadthereare

bothliquidity‐constrainedandunconstrainedhouseholds,wheretheformerspendalltheirincome

eachquarterandthelatterconsumeandinvestbasedontheirassessmentoftheirlifetime

resources.Inmakingthisassessment,unconstrainedhouseholdsdiscountfuturelaborandtransfer

incomeataratesubstantiallyhigherthanthediscountrateonfutureincomefromnon‐human

wealth,reflectinguninsurableindividualincomerisk.

31

Notably,aggregatefutureincomeisvalued

29

Documentationofthemodelisavailableatwww.federalreserve.gov/econresdata/frbus/us‐models‐about.htm,

includingacompletelistingofmodelequationsandcoefficients,papersdiscussingdifferentaspectsofFRB/US,

andillustrativesimulationprograms.

30

Kiley(2012)presentsevidencethattheaggregatedemandeffectsofchangesintermpremiumsmaybeweaker

thanthoseofexpectedfutureshortrates.

31

Themarginalpropensityofhouseholdstoconsumeoutofdifferenttypesofincomecanvary,dependingon

whichgroupofhouseholdsreceivestheincome.Forexample,transferincomeisdisproportionatelyreceived

Page16of54

bydifferentdiscountfactorsdependingonitssourceandtheaverageageoftherecipient

household.Asaresult,theeffectiveplanninghorizonfortheaveragehouseholdinFRB/USisclose

tothefive‐yearperiodadvocatedbyFriedman(1957)ratherthanthemuchlongertimehorizonof

householdsembeddedinatypi calDSGEmodel.Thismodelingchoicereduces,inourview

realistically,theabilitytoaffectcurrenteconomicactivitythroughpoliciesthatraiseexpectationsof

futurerealactivityandincomes(forexample,asanalyzedinWerning(2012)).Theabsenceofa

representativehouseholdalsomeansthatwecannotevaluateunconventionalpoliciesaccordingto

theirwelfareimplications;instead,wesimplyreporttheirestimatedeffectsonrealeconomic

activityandinflation.

Finally,priceandwageinflationdynamicsfollowaNewKeynesianPhillipscurvespecificationinthe

presenceofnonzerotrendinflation.

32

WhilethisspecificationisverysimilartothoseusedinDSGE

models,theestimateddegreeofinertiainpriceandwageinflationishigherthaninmostDSGE

modelsbasedonthesticky‐priceparadigm.Thisfeatureinteractswithhouseholds’highdiscount

rateoffutureincomediscussedbeforetodampentheeffectsofannouncedfuturemonetarypolicy

changes,suchasforwardguidance.Inparticular,thecombinationofthesetwofeaturesexplains

why,asourresultswillshow,theFRB/USmodeldoesnotexhibitthe“forwardguidancepuzzle”that

besetsstandardDSGEmodels(DelNegroetal.,2013).

33

AsshowninAppendix2,inasituation

whenthenominalshortrateisheldconstantforanextendedperiodoftime,forexampl ebecause

thezerolowerboundisbinding,acredibleannouncementtodayoflowershort‐termratesinthe

futureraisescurrentoutputandinflationinacanonicalDSGEmodel, andtheseincreasesarelarger

thefurtherintothefutureistheannouncedaction.Givenconstantnominalinterestrates,the

increaseininflationreducescurrentandexpectedfuturerealinterestrates,whichinturnhasstrong

aggregatedemandeffectsbecauseofthehigherinterestratesensitivityduetohouseholds’longer

planninghorizons.Bothofthesechannelsaresubstantiallyand,inourview,plausiblyattenuatedin

FRB/US.

Monetarypolicyismodeledasasimpleruleforthefederalfundsratesubjecttothezerolower

boundonnominalinterestrates;importantlyforouranalysis,theparametersofthepolicyruleused

insimulationscanbemodifiedasdesiredtobeconsistentwithprivatebeliefsaboutthelikelyfuture

behavioroftheFOMC.Inourcounterfactualsimulations,thepronouncedweaknessofthe

economysincelate2008meansthattheZLBmarkedlyandpersistentlyconstrainsactualand

expectedmonetarypolicy.Moreover,theimpositionoftheZLBmakesthemodelhighlynon‐linear,

therebyprofoundlyinfluencingthesimulateddynamicsoftheeconomy.

34

InourbaselineversionoftheFRB/USmodel,allprivateagentsareassumedtohaverational

expectations—thatis,beli efswhichareconsistentwiththedynamicsofthefullmodel,conditionalon

theanticipatedbehaviorofpolicymakers.Thepublicdoesnotnecessarilyhaveperfectforesightabout

byretireeswhoarewell‐advancedintheirlifecycles.Inaddition,aggregationacrossagegroupsleadsto

averagepropensitiestospendthatvaryacrossdifferenttypesofaggregateincome,reflectingvariationsinthe

distributionofincomeacrossgroups.

32

ThespecificationofthePhillipscurveusedinFRB/USisbasedonthemodeldevelopedbyCogleyandSbordone

(2008);thismodelallowsfortimevariationintheunderlyingtrendininflation,reflecting(forthemostpart)

changesinthecentralbank’sinflationobjective.InFRB/US,thepost‐1979trend

isbasedonmeasuresofexpected

long‐runinflationasreportedinitiallyintheHoeySurveyandlatertheSurveyofProfessionalForecasters.

33

SeeChung(2015)foracomparisonofthemacroeconomiceffectsofforwardguidanceintheFRB/USmodel

comparedtotwostandardDSGEmodels.

34

Tosolvethemodel,weusedthesolutionmethoddescribedbyBrayton(2012).

Page17of54

theshocksthatwillhittheeconomyinthefuture,however,northeFOMC’sresponsetothoseshocks.

Whileweviewanexaminationoftheeffectsofunconventionalmonetarypolicyinarangeofalternative

modelsasaworthwhileundertaking,itisbeyondthescopeofthispaper.Instead,wewillreportresults

oftheseeffectsforarangeofalternativeparameterizationsofFRB/US,suchasalternativeassumptions

abouttheformationofexpectationsbyvariousagents,aboutinflationdynamics,andabouttheinterest

elasticityofaggregatedemand.

Illustrativesimulations

Beforeturningtoestimatesoftheeffectsoftheunconventionalpolicyactionsactuallyundertakenby

theFederalReserve,weillustratethemacroeconomiceffectsofforwardguidanceandassetpurchases

inahypotheticalscenarioinwhichtheU.S.economyishit withasequenceofverylargeandpersistent

contractionaryshocks.Inordertoillustratesomekeyfactorsthatinfluencethenetstimulusprovided

byunconventionalpolicy,andsoneedtobetakenintoaccountwhenwescoretheactualeffectiveness

oftheFOMC’sactionsinthenextsection,werunthisexerciseunderalternativeassumptionsabout

boththe

public’sunderstandingofthepersistenceoftheeconomicdownturnandthespeedatwhich

policymakersrespond.

Thescenarioiscalibratedsuchthat,underabaselineassumptionofthefederalfundsratefollowingthe

standardTaylorruleandwithoutanyassetpurchases,thefederalfundsrateisatitseffectivelower

boundforfiveyears.Oncetheeconomicslumpstarts,thepublicisassumedtohaveperfectforesight

abouttheshocksthatwillbuffettheeconomyovertime,aswellasthemonetarypolicyresponseto

thoseshocks.AsindicatedbytheblacklinesinFigure4,themagnitudeoftheseshocks

causesthe

unemploymentratetoroughlydoublewithinthefirsttwoyears,from5¼percentpriortotheslumpto

apeakof10¼percent,andtodeclinethereaftergradually,whileinflationdropsbymorethan1

percentagepoint.Despitetheassociateddeclineininflationexpectedoverthenext10

years,thereal

10‐yearyieldfallsbyabout2½percentagepoints,reflectingthelowerpathoftherealfederalfundsrate

overthattimehorizon.Becausepolicymakersdonotengageinlarge‐scaleassetpurchasesinthis

scenario,termpremiumsareassumedtobeunaffectedalthoughriskpremiumsoncorporate

bondsand

equityincreaseendogenously.

AstheredlinesplottedinFigure4illustrate,theseadverseeffectswouldbenoticeablymitigatedby

raisingtheoutputgapresponsecoefficientfrom0.5to1,whichwoulddelayliftofffromtheeffective

lowerboundbytwoquarters.Thereafter,thefederalfundspathis

littlechangedcomparedtothe

standardTaylorrulesimulation,butgiventhehigherpathforinflation,thereal10‐yearTreasuryyield

runsabout¼percentagepointlowerforseveralyearsinarow.Similar, albeitslightlysmaller,effects

fromthischangeinpolicyruleobtaininamoderateslumpscenario,

inwhichthefederalfundsrate

underthestandardTaylorruleisconstrainedforonlythreeyearsbytheeffectivelowerbound(theblue

andgreenlines).

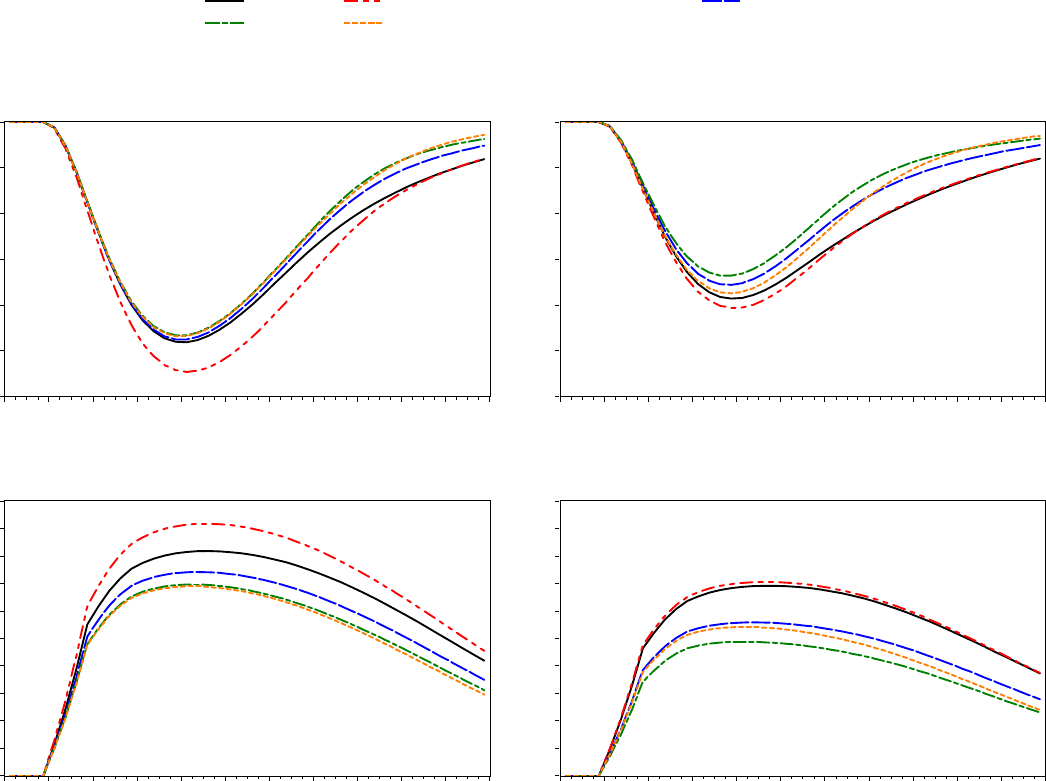

Themarginalunemploymentrateandinflationeffectsofvariouspolicyrulechangesunderthesetwo

scenariosareshowninFigure5,expressedas

deviationsfromoutcomesunderthestandardTaylorrule.

Inadditiontotherulewithanoutputgapcoefficientequalto1(thereddashedlines),thefigurealso

showstheeffectsofraisingtheoutputgapcoefficientto1.5,ofraisingitto1.0butinadditionswitching

toaninertial

rulewithacoefficientof0.8onthelaggedfederalfundsrate,orofimplementinga

thresholdstrategywherebythefederalfundsratestaysattheeffectivelowerbounduntilthe

unemploymentratefallsbelow6½percentandthereafterfollowsthestandardTaylorrule.The

macroeconomiceffectsofadoptingeither

oftheserulesarelargerinthehighlypersistentslump

Page18of54

scenario(theleftpanels)thaninthemoderatelypersistentslumpscenario(therightpanels),andare

thelargestfortheinertialrule,followedbytherulewithanoutputgapresponseof1.

35

ThefirsttwocolumnsofTable5provideinformationaboutthechannelsinFRB/USthroughwhichthe

changeintheperceivedpolicyruleistransmittedtorealeconomicactivityandinflation.Inthehighly

persistentslumpscenario(theupperrowsofthetable),long‐termrealTreasuryyieldsdeclinemostly

becauseofanincreaseinexpectedinflationratherthanareducti onintheexpectednominalpathof

futureshort‐terminterestrates;theinflationeffectisespeciallypronouncedinthecaseofachangeto

aninertialpolicyrule(column2).Endogenousdeclinesinriskpremiumsleadtolargerreductions

inreal

corporateyieldsaswellasanotableincreaseinequityvaluations.Financialmar keteffectsareslightly

smallerinthemoderatelypersistentslumpscenario,pointingtotheimportanceofexpectationsabout

thepersistenceofadverseeconomiccircumstances;differencesfromthehighly‐persistentscenario

wouldbemoreappreciableiftheslump

wasevenmoretransitory.

Figure6highlightstheimportanceofinformationalassumptionsfortheestimatedmacroeconomic

effectsofthesepolicies.Theleft‐handpanelspresenttheresponsesofunemploymentandinflation

underthreeoftherulesthatwerereportedinFigure5,againexpressedrelativetooutcomesunderthe

standardTaylorrulewithoutasset

purchases,inthecontextofthehighlypersistentslumpscenario.As

mentionedbefore,thepublichasacompleteunderstandingofhowtheslumpwilldevelopovertime,

andmonetarypolicyrespondsimmediately tothecrisis.Incontrast,themiddleandright‐handpanels

ofthechartshowthemarginaleffectiveness

ofthesamepoli cyinitiativesunderalternativeassumptions

forprivateagents’knowledgeofthefutureandthetimingofpolicyresponses.Specifically,themiddle

panelsofFigure6reportthemarginaleffectivenessofthesameshiftsinpolicyruleswhenagents

initiallyexpectthecontractioninrealactivitytobemuch

lesssevereandpersistentthanactuallyturns

outtobethecase,andsoonlygraduallycometounderstandthattheeconomyhasenteredaprolonged

ZLBepisode.Theright‐handpanelsofthefigureshowthestimulusprovidedwhenthepublicfully

understandsthenatureoftheshockshitting

theeconomybutthecentralbankshifts toadifferent

policyruleonlythreeyearsaftertheonsetofthecrisis,andthepublicdoesnotanticipateanychangein

policybeforehand.Ascanbeseen,eithertypeofdelaynotonlyshiftsthetimingofstimulusbut

actuallyreducesits

magnitude—animportantconsiderationinanyscoringoftheefficacyoftheFOMC’s

unconventionalpolicyactions,giventhegradualnatureoftherevisionstoboththeBlueChip

projectionsandpolicyexpectationsobservedfromearly2009throughlate2013.

Figure7showsthemarginaleffectsofannouncing a$1.5trillionLSAP

programattheonsetofthecrisis,

conditioningontheinterestrateruleinplaceatthetimeoftheannouncement.Basedonsimulationsof

theLi‐Weimodel,suchaprogramwouldbeexpectedtoreducethetermpremiumembeddedinthe10‐

yearTreasuryyieldabout60basis

pointsinitially,withtheeffectfadingawaythereafteratroughlythe

averagepaceshowninFigure3.Columns3to5ofTable5illustrateforthreeoftherulesshownin

Figure7that,inFRB/US,suchareductioninpremiumsdirectlyincreasesthedownwardpressureon

Treasuryyieldsand

indirectlyinfluencesotherassetpricesthrougharbitrageeffects,therebyeasingthe

costofborrowingforhouseholdsandfirms,checkingtherecession‐drivendeclinesincorporateequity

valuationsandhouseholdwealth,andfurtherloweringtherealforeignexchangevalueofthedollar.

35

ThesimulationresultsarebroadlyconsistentwiththeresultsreportedinTables3and4.Inparticular,inthe

middlecolumnofTable3,theestimatedcoefficientontheoutputgaprisesabove1intheMarch2013BlueChip

survey,whentheunemploymentrateatthetimeofliftoff

isexpectedtobe6.8percent.Bycomparison,inthe

simulationinfigure5withβequalto1,theunemploymentrateatthetimeofliftoffinthehighlypersistentslump

scenariois6.4percent.

Page19of54

Formostoftherules,themarginaleffectsoftheLSAPprogramareverysimilar.Thestrongereconomic

conditionsinducedbytheassetpurchasescallforthastrongerinterestrateresponseafterliftoffunder

themore‐aggressivepolicyrules,illustratingthatinFRB/US,fundsratepolicy

andassetpurchasesactto

someextentassubstitutes.

TheanticipatedreductioninthepathofTreasurytermpremiumsassociatedwithassetpurchases

influencesmacroeconomicconditionsviatheformer’seffectsonavarietyoffinancialmarketvariables.

Exceptforthesizeofthetermpremiumeffect,whichwetakefromthe

analysisofIhrigetal.(2013),the

financialmarketresponsesshowninTable5areendogenouslygeneratedbyFRB/US.Arethemodel’s

predictionsfortheresponseoffinancialmarketconditionstoashiftinTreasurytermpremiumsinline

withtheempiricalevidence?InAppendix2,wesummarizesomeof

thefindingsofeventstudies

followingQE‐relatedevents.Althoughthereissomevarietyinresultsacrossstudies,agoodcentral

estimateisthataQE‐inducedreductionin10‐yearTreasuryyieldsby20basispointsisassociatedwitha

reductioninthe30‐yearmortgagerateofabout25

basispoints(reflectingthesizeableshareofMBS

purchasesintheFederalReserve’sQEprograms),areductioninBBBcorporatebondsofabout15basis

points,anincreaseinequitypricesofabout1¾percent,andareductionintherealexchangerateof

about¾percent.Therelativemagnitudes

ofthemodel‐generatedresponsesshownincolumns3to5

ofTable5areveryclosetotheseestimates,suggestingthatthemodelprovidesagoodapproximation

ofthisstageofthetransmissionchannel.

ThedifferencesbetweentheleftandrightpanelsinFigure7illustratethattheeffectsof

LSAPsdepend

importantlyonhowlongthefederalfundsrateisexpectedtoremainattheeffectivelowerbound,and

hencehowfarintothefuturehighershort‐terminterestrateswillbegintooffsettheeffectsofthe

LSAPs.Accordingly,ifagentsatthelaunchofaQEprogram

aresubstantiallyoverestimatingthepaceat

whichtheeconomywillrecoverandsoprojecttooearlyadateforliftoffofthefundsrate,thedirect

downwardpressureonlong‐terminterestratescausedbyassetpurchasesinitiallywillbesubstantially

offsetbyasimultaneousupwardrevisiontotheexpectedpath

offutureshort‐termrates.Similar

considerationsattendthestimulusprovidedbyanannouncedchangeintheimplicitpolicyrule.Iflabor

andproductmarketgapsarealreadyexpectedtoclosequicklyevenwithouttheadoptionofamore

accommodativerule,thenincreasingthecoefficientonslackoradoptinga

moreinertialapproachto

policysettingwillnotmarkedlyaltertheprojectedfuturepathofthefundsrate,incontrasttowhat

wouldoccurifslackwasexpectedtoremainsizeableformanymoreyears.

VI. TheEffectsoftheFOMC’sUnconventionalPolicyActions—SimulationResults

Thissectionpresentsourquantitative

assessmentsoftheactualstimulustorealactivityandinflation

providedbytheFOMC’sforwardguidanceandassetpurchasessinceearly2009,basedon

counterfactualsimulationsofFRB/US.Webeginwithadiscussionofthedesignofourcounterfactual

simulationanalysis,whichamongotherthingshastodealwithcomplications arising

fromgradual

learningonthepartofthepublicaboutfuturemonetarypolicyaswellasthelikelymagnitudeand

persistenceofthepost‐crisiseconomicslump.Usingthebaselineversionofthemodel,wefindthatthe

FOMC’sunconventionalpolicyactionsapparentlyprovidedonlyasmallboosttothe

realeconomy

duringtherecessionandtheinitialrecoveryperiodbutthattheseeffectshavesincebecomemore

substantial;thebaselinecounterfactualsimulationsalsosuggestthatinflationeffectstodatehavebeen

relativelymodest.Considerableuncertaintyattendstheseassessments,however,assimulations

generatedusingplausiblealternativespecificationsofthemodelyield

awiderangeofestimated

unemploymentandinflationeffects;inaddition,our analysisdoesnottakeintoaccountthepossibility

Page20of54

thattheFOMC’sunconventionalactionsmayhaveledtomarkedimprovementsinhouseholdand

businessconfidence,therebysignificantlyboostingtheeconomybeyondwhatourmodel(s)predict.

Simulationdesign

Toassesstheconsequencesofannouncingasystematicchangeinmonetarypolicy,onetypicallystarts

withabaseline

embodyingsomereferencerulecalibratedtomatchtheFOMC’srecentbehavior,and

thensimulatestheeffectofswitchingtoanewpolicyruleundertheassumptionthatagentshave

rationalexpectationsandthepolicyannouncementiscompletelycredible.Astheprecedingsimulations

demonstrate,however,thestimulusprovidedbyunconventionalpolicy

atanypointintimedepended

notonwhattheFOMCwouldactuallydofromthatpointforward,butonwhatthepublicatthetime

expectedtheFederalReservetodointhefuture—animportantconsiderationforourefficacy

assessmentsgiventhattheperceivedpolicyruleand theexpectedtrajectory

oftermpremiumeffects

evolvedgraduallyfromearly2009tolate2013.Controllingforthepaceoflearningisalsoimportant

withregardstochangesovertimeinperceptionsofthefundamentalshocksactingtoshapethe

economicoutlook,giventhattheillustrativesimulations alsoshowedthattheactualstimulus

imparted

byforwardguidanceandassetpurchasespartiallydependsonhowlongthefundsrateisexpectedto

remainconstrainedbythezerolowerbound.

Tocontrolfortheselearningeffects,weemployasequenceofbaselinesofpastandprojected

conditions,eachofwhichrepresentsasnapshotofpast

economicdevelopmentsandexpectationsfor

thefuturetakenataparticularpointintime.Thisapproachenablesustocontrolfortheactualtiming

oftheshiftsinexpectationsassociatedwithrevisionsinboththeperceivedvalueofβintheimplicit

fundsrateruleandtheexpectedtrajectoryofQE‐related

termpremiumeffects.Inaddition ,itallowsus

toparsetheforcesdrivingchangesovertimeintheeconomicoutlook—asreflectedinrevisionstothe

extendedBlueChipprojections—intothoseassociatedwithperceivedinnovationsinpolicy,andthose

associatedwithchangingassessmentsofthefundamentalshockstoaggregatedemandand

other

factorshittingtheeconomy,bothnowandinthepast.

Forcomputationalconvenience,weassumethatexpectationsaboutfuturepolicyandotherfactorsare

updatedtwiceayear,onceinthefirstquartertotakeonboardontheinformationprovidedbythe

MarchBlueChipsurveys,andoncein

thethirdquartertoincorporatetheresultsfromtheOctober

surveys.Eachupdateofexpectationsrequiresthecreationofanewbaseline;thus,weconstructa

2009Q1baseline,a2009Q3baseline,a2010Q1baseline,andsoontoourfinal2013Q3baseline.The

expectedtrajectoryofQE‐relatedterm premium

effectsincorporatedintoeachbaselinematchesthe

correspondingpathestimatedbyIhrigetalandreportedinFigure3;forexample,thepathincorporated

intothe2009Q3baselineisthesameastheLSAP1path,whil e thepath incorporatedintothe2010Q3

baselinematchestheinitialestimatedtrajectoryofLSAP2effects.

36

Withregardstorevisionsinthe

policyruleacrossbaselines,ourbase‐caseassumptionisthattheperceivedvaluesofλandαarealways

zeroand0.5,respectively,butthattheperceivedvalueofβguidingfuturemonetarypolicyratchetsup

markedlyasonemovesfromthe2009Q1baselinetothe2013Q3

baseline.Asdiscussedearlier,it

appearsthatprivateforecasterspersistentlyanticipatedpolicyatthetimeofliftofftobemore

accommodativethanthatwhichwouldbefollowedoverthelongerrun. Accordingly,weassumethat

36

ThefulldimensionsofthefirstLSAPprogramwerenotannounceduntilaftertheMarch18,2009FOMC

meeting,althoughsomeinformationabouttheFederalReserve’sintentionstobuyMBSwasavailableinlate2008.

Forthisreason,weassumethatagentsin2009Q1expectedassetpurchasestolowerterm

premiumsbyroughly

10basispointsinthefirsthalfof2009,withthedownwardpressureerodingawayrapidlythereafter.

Page21of54

agentsatthetimeofeachsurveyexpectedβinthefuturetoequalthevaluesreportedinTable4

throughtheprojecteddateofliftoff,butthenanticipatedthatβwouldthereafterdeclinegraduallyto

thelonger‐runestimatesreportedinTable3.Theprecisepatternof

revisionstotheexpectedpathofβ

acrossbaselinesisillustratedinFigure8bytherisingsequenceofblacklines.Inadditiontothisbase‐

caseassumption,wealsoconsideranalternativeevolutionafter2011fortheperceivedpolicyrulethat