Userid: CPM Schema:

instrx

Leadpct: 100% Pt. size: 9.5

Draft Ok to Print

AH XSL/XML

Fileid: … ons/i706/202309/a/xml/cycle03/source (Init. & Date) _______

Page 1 of 59 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Instructions for Form 706

(Rev. September 2023)

For decedents dying after December 31, 2022

United States Estate (and Generation-Skipping Transfer) Tax Return

Department of the Treasury

Internal Revenue Service

Section references are to the Internal Revenue Code unless

otherwise noted.

Revisions of Form 706

For Decedents Dying Use Revision of

Form 706 DatedAfter and Before

December 31, 1998 January 1, 2001 July 1999

December 31, 2000 January 1, 2002 November 2001

December 31, 2001 January 1, 2003 August 2002

December 31, 2002 January 1, 2004 August 2003

December 31, 2003 January 1, 2005 August 2004

December 31, 2004 January 1, 2006 August 2005

December 31, 2005 January 1, 2007 October 2006

December 31, 2006 January 1, 2008 September 2007

December 31, 2007 January 1, 2009 August 2008

December 31, 2008 January 1, 2010 September 2009

December 31, 2009 January 1, 2011 July 2011

December 31, 2010 January 1, 2012 August 2011

December 31, 2011 January 1, 2013 August 2012

December 31, 2012 January 1, 2017 August 2013

December 31, 2016 January 1, 2018 August 2017

December 31, 2017 January 1, 2019 November 2018

December 31, 2018 August 2019

Future Developments

For the latest information about developments related to

Form 706 and its instructions, such as legislation enacted

after they were published, go to

IRS.gov/Form706.

What's New

Various dollar amounts and limitations in Form 706 are

indexed for inflation. For decedents dying in 2023, the

following amounts are applicable.

•

The basic exclusion amount is $12,920,000.

•

The ceiling on special-use valuation is $1,310,000.

•

The amount used in figuring the 2% portion of estate tax

payable in installments is $1,750,000.

•

The basic credit amount is $5,113,800.

The IRS will publish amounts for future years in annual

revenue procedures.

Reminders

Schedule R-1 is a separate form. Schedule R-1 isn’t part

of Form 706; instead, you will need to obtain a separate

Schedule R-1 to complete and file with Form 706.

Identifying exhibits. Copies of tax returns filed with Form

706 must be identified as exhibits to the Form 706.

Estate tax closing letter fee. Effective October 28, 2021, a

user fee of $67 was established for persons requesting the

issuance of an estate tax closing letter (ETCL). See

ETCL

fee, later, for more information.

Extension of time to elect portability. Effective July 8,

2022, Rev. Proc. 2022-32 provides a simplified method for

certain estates to obtain an extension of time to file a return

on or before the fifth anniversary of the decedent’s death to

elect portability of the deceased spousal unused exclusion

(DSUE) amount. See

Extension to elect portability, later, for

more information.

General Instructions

Purpose of Form

The executor of a decedent's estate uses Form 706 to figure

the estate tax imposed by chapter 11 of the Internal Revenue

Code. This tax is levied on the entire taxable estate and not

just on the share received by a particular beneficiary. Form

706 is also used to figure the generation-skipping transfer

(GST) tax imposed by chapter 13 on direct skips (transfers to

skip persons of interests in property included in the

decedent's gross estate).

Which Estates Must File

For decedents who died in 2023, Form 706 must be filed by

the executor of the estate of every U.S. citizen or resident:

a. Whose gross estate, plus adjusted taxable gifts and

specific exemption, is more than $12,920,000; or

b. Whose executor elects to transfer the deceased

spousal unused exclusion (DSUE) amount to the

surviving spouse, regardless of the size of the decedent's

gross estate. See the instructions for Part 6—Portability

of Deceased Spousal Unused Exclusion, later, and

sections 2010(c)(4) and (c)(5).

To determine whether you must file a return for the estate

under (a) above, add:

1. The adjusted taxable gifts (as defined in section 2503)

made by the decedent after December 31, 1976;

2. The total specific exemption allowed under section 2521

(as in effect before its repeal by the Tax Reform Act of

1976) for gifts made by the decedent after September 8,

1976; and

3. The decedent's gross estate valued as of the date of

death.

Gross Estate

The gross estate includes all property in which the decedent

had an interest (including property outside the United

States). It also includes:

•

Certain transfers made during the decedent's life without

an adequate and full consideration in money or money's

worth,

•

Annuities,

•

The includible portion of joint estates with right of

survivorship (see the instructions for Schedule E),

•

The includible portion of tenancies by the entirety (see

the instructions for Schedule E),

Sep 5, 2023 Cat. No. 16779E

Page 2 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

•

Certain life insurance proceeds (even though payable to

beneficiaries other than the estate) (see the instructions

for Schedule D),

•

Digital assets (see the instructions for Schedule F),

•

Property over which the decedent possessed a general

power of appointment,

•

Dower or curtesy (or statutory estate) of the surviving

spouse, and

•

Community property to the extent of the decedent's

interest as defined by applicable law.

Note. Under the special rule of Regulations section

20.2010-2(a)(7)(ii), executors of estates who are not required

to file Form 706 under section 6018(a), but who are filing to

elect portability of the DSUE amount to the surviving spouse,

are not required to report the value of certain property eligible

for the marital deduction under section 2056 or 2056A or the

charitable deduction under section 2055. However, the value

of those assets must be estimated and included in the total

value of the gross estate. See the instructions for

Part

5—Recapitulation, items 10 and 23, later, for more

information.

For more specific information, see the instructions for

Schedules A through I.

U.S. Citizens or Residents; Nonresident

Noncitizens

File Form 706 for the estates of decedents who were either

U.S. citizens or U.S. residents at the time of death. For estate

tax purposes, a resident is someone who had a domicile in

the United States at the time of death. A person acquires a

domicile by living in a place for even a brief period of time, as

long as the person had no intention of moving from that

place. See Regulations section 20.0-1(b).

Decedents who were neither U.S. citizens nor U.S.

residents at the time of death file Form 706-NA, United

States Estate (and Generation-Skipping Transfer) Tax Return,

Estate of nonresident not a citizen of the United States.

Residents of U.S. Possessions

All references to citizens of the United States are subject to

the provisions of sections 2208 and 2209, relating to

decedents who were U.S. citizens and residents of a U.S.

possession on the date of death. If such decedents became

U.S. citizens only because of their connections with a

possession, then the decedents are considered nonresidents

not citizens of the United States for estate tax purposes, and

you should file Form 706-NA. If such decedents became U.S.

citizens wholly independently of their connections with a

possession, then the decedents are considered U.S. citizens

for estate tax purposes, and you should file Form 706.

Executor

The term “executor” includes the executor, personal

representative, or administrator of the decedent's estate. If

none of these is appointed, qualified, and acting in the United

States, every person in actual or constructive possession of

any property of the decedent is considered an executor and

must file a return.

Executors must provide documentation proving their

status. Documentations will vary but may include documents

such as certified copies of wills or court orders designating

the executor(s). Statements by executors attesting to their

status are insufficient.

When To File

You must file Form 706 to report estate and/or GST tax within

9 months after the date of the decedent's death. If you are

unable to file Form 706 by the due date, you may receive an

extension of time to file. Use Form 4768, Application for

Extension of Time To File a Return and/or Pay U.S. Estate

(and Generation-Skipping Transfer) Taxes, to apply for an

automatic 6-month extension of time to file.

Portability election. An executor can only elect to transfer

the DSUE amount to the surviving spouse if the Form 706 is

filed timely, that is, within 9 months of the decedent's date of

death or, if you have received an extension of time to file,

before the 6-month extension period ends.

Extension to elect portability. Executors who did not

have a filing requirement under section 6018(a) but failed to

timely file Form 706 to make the portability election may be

eligible for an extension under Rev. Proc. 2022-32, 2022-30

I.R.B. 101 (superseding Rev. Proc. 2017-34, 2017-26 I.R.B.

1282). Executors filing to elect portability may now file Form

706 on or before the fifth anniversary of the decedent’s death.

An executor wishing to elect portability under this

extension must state at the top of the Form 706 being filed

that the return is “Filed Pursuant to Rev. Proc. 2022-32 to

Elect Portability under section 2010(c)(5)(A).” For more

information on this extension, see

Rev. Proc. 2022-32.

Note. Any estate that is filing an estate tax return only to

elect portability and did not file timely or within the extension

provided in Rev. Proc. 2022-32 may seek relief under

Regulations section 301.9100-3 to make the portability

election.

Where To File

File Form 706 at the following address.

Department of the Treasury

Internal Revenue Service

Kansas City, MO 64999

If you’re using a private delivery service (PDS), file at this

address.

Internal Revenue Submission Processing Center

333 W. Pershing Road

Kansas City, MO 64108

If you’re filing an amended Form 706, use the following

address.

Internal Revenue Service Center

Attn: E&G, Stop 824G

7940 Kentucky Drive

Florence, KY 41042-2915

If you’re using a PDS for your amended Form 706, use this

address.

Internal Revenue Service Center

Attn: E&G, Stop 824G

7940 Kentucky Drive

Florence, KY 41042-2915

-2-

Instructions for Form 706 (Rev. 09-2023)

Page 3 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Paying the Tax

The estate and GST taxes are due within 9 months of the

date of the decedent's death. You may request an extension

of time for payment by filing Form 4768. You may also elect

under section 6166 to pay in installments or under section

6163 to postpone the part of the tax attributable to a

reversionary or remainder interest. These elections are made

by checking “Yes” on lines 3 and 4 (respectively) of

Part

3—Elections by the Executor and attaching the required

statements.

If the tax paid with the return is different from the balance

due as figured on the return, explain the difference in an

attached statement. If you have made prior payments to the

IRS, attach a statement to Form 706 including these facts.

Paying by check. Make the check payable to “United States

Treasury.” Please write the decedent's name, social security

number (SSN), and “Form 706” on the check to assist us in

posting it to the proper account.

No checks of $100 million or more accepted. The IRS

cannot accept a single check (including a cashier's check) for

amounts of $100,000,000 ($100 million) or more. If you're

sending $100 million or more by check, you'll need to spread

the payments over 2 or more checks, with each check made

out for an amount less than $100 million. The $100 million or

more amount limit does not apply to other methods of

payment (such as electronic payments). Please consider a

method of payment other than a check if the amount of the

payment is over $100 million.

Paying electronically. Payment of the tax due shown on

Form 706 may be submitted electronically through the

Electronic Federal Tax Payment System (EFTPS). EFTPS is

a free service of the Department of the Treasury.

To be considered timely, payments made through EFTPS

must be completed no later than 8 p.m. Eastern time the day

before the due date. All EFTPS payments must be scheduled

in advance of the due date and, if necessary, may be

changed or canceled up to 2 business days before the

scheduled payment date.

To get more information about EFTPS or to enroll in

EFTPS, visit EFTPS.gov or call 800-555-4477. To contact

EFTPS using Telecommunications Relay Service (TRS) for

people who are deaf, hard of hearing, or have a speech

disability, dial 711 and then provide the TRS assistant the

800-555-4477 number, above, or 800-733-4829. Additional

information about EFTPS is available in Pub. 966, Electronic

Federal Tax Payment System: A Guide to Getting Started.

Signature and Verification

If there is more than one executor, all listed executors

are responsible for the return. However, it is sufficient

for only one of the co-executors to sign the return.

All executors are responsible for the return as filed and are

liable for penalties imposed for erroneous or false returns.

If two or more persons are liable for filing the return, they

should all join together in filing one complete return.

However, if they are unable to join in making one complete

return, each is required to file a return disclosing all the

information the person has about the estate, including the

name of every person holding an interest in the property and

a full description of the property. If the appointed, qualified,

and acting executor is unable to make a complete return,

then every person holding an interest in the property must, on

notice from the IRS, make a return regarding that interest.

CAUTION

!

The executor who files the return must, in every case, sign

the declaration on page 1 under penalties of perjury.

Generally, anyone who is paid to prepare the return must

sign the return in the space provided and fill in the Paid

Preparer Use Only area. See section 7701(a)(36)(B) for

exceptions.

In addition to signing and completing the required

information, the paid preparer must give a copy of the

completed return to the executor.

Note. A paid preparer may sign original or amended returns

by rubber stamp, mechanical device, or computer software

program.

Amending Form 706

If you find that you must change something on a return that

has already been filed, you should:

•

File another Form 706;

•

Enter “Supplemental Information” across the top of

page 1 of the form;

•

Include a statement of what has changed, along with the

supporting information; and

•

Attach a copy of pages 1, 2, 3, and 4 of the original Form

706 that has already been filed.

For the mailing address for supplemental Form 706, see

Filing Estate and Gift Tax Returns.

File the amended Form 706 at the following address.

Internal Revenue Service Center

Attn: E&G, Stop 824G

7940 Kentucky Drive

Florence, KY 41042-2915

If you’re using a PDS, file at this address.

Internal Revenue Service Center

Attn: E&G, Stop 824G

7940 Kentucky Drive

Florence, KY 41042-2915

If you have already been notified that the return has been

selected for examination, you should provide the additional

information directly to the office conducting the examination.

Supplemental Documents

Note. You must attach the death certificate to the return.

If the decedent was a citizen or resident of the United

States and died testate (leaving a valid will), attach a certified

copy of the will to the return. If you cannot obtain a certified

copy, attach a copy of the will and an explanation of why it is

not certified. Other supplemental documents may be

required, as explained later. Examples include Form 712, Life

Insurance Statement; Form 709, United States Gift (and

Generation-Skipping Transfer) Tax Return; Form 706-CE,

Certificate of Payment of Foreign Death Tax; trust and power

of appointment instruments; and state certification of

payment of death taxes. If you do not file these documents

with the return, the processing of the return will be delayed.

If the decedent was a U.S. citizen but not a resident of the

United States, you must attach the following documents to

the return.

1. A copy of the inventory of property and the schedule of

liabilities, claims against the estate, and expenses of

Instructions for Form 706 (Rev. 09-2023)

-3-

Page 4 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

administration filed with the foreign court of probate

jurisdiction, certified by a proper official of the court.

2. A copy of the return filed under the foreign inheritance,

estate, legacy, succession tax, or other death tax act,

certified by a proper official of the foreign tax

department, if the estate is subject to such a foreign tax.

3. If the decedent died testate, a certified copy of the will.

Rounding Off to Whole Dollars

You may round off cents to whole dollars on the return and

schedules. If you do round to whole dollars, you must round

all amounts. To round, drop amounts under 50 cents and

increase amounts from 50 to 99 cents to the next dollar. For

example, $1.39 becomes $1 and $2.50 becomes $3.

Penalties

Late filing and late payment. Section 6651 provides for

penalties for both late filing and for late payment unless there

is reasonable cause for the delay. The law also provides for

penalties for willful attempts to evade payment of tax. The

late filing penalty will not be imposed if the taxpayer can show

that the failure to file a timely return is due to reasonable

cause.

Reasonable-cause determinations. If you receive a notice

about penalties after you file Form 706, send an explanation

and we will determine if you meet reasonable-cause criteria.

Do not attach an explanation when you file Form 706.

Explanations attached to the return at the time of filing will not

be considered.

Valuation understatement. Section 6662 provides a 20%

penalty for the underpayment of estate tax that exceeds

$5,000 when the underpayment is attributable to valuation

understatements. A valuation understatement occurs when

the value of property reported on Form 706 is 65% or less of

the actual value of the property.

This penalty increases to 40% if there is a gross valuation

understatement. A gross valuation understatement occurs if

any property on the return is valued at 40% or less of the

value determined to be correct.

Penalties also apply to late filing, late payment, and

underpayment of GST taxes.

Return preparer. Estate tax return preparers who prepare

any return or claim for refund which reflects an

understatement of tax liability due to an unreasonable

position are subject to a penalty equal to the greater of

$1,000 or 50% of the income earned (or to be earned) for the

preparation of each such return.

Estate tax return preparers who prepare a return or claim

for refund which reflects an understatement of tax liability due

to willful or reckless conduct are subject to a penalty of

$5,000 or 75% of the income earned (or income to be

earned), whichever is greater, for the preparation of each

such return.

Estate tax return preparers who prepare any return or

claim for a refund are required to furnish a copy to the

taxpayer, sign the return, and provide their PTIN, but who fail

to do so, are subject to a penalty of $50 for such failure,

unless it is shown that such failure is due to reasonable

cause and not due to willful neglect.

See sections 6694 and 6695, the related regulations, and

Announcement 2009-15, 2009-11 I.R.B. 687, available at

Announcement 2009-15, for more information.

Consistent Basis Reporting

Certain estates are required to report to the IRS and the

recipient, the estate tax value of each asset included in the

gross estate within 30 days of the due date (including

extensions) of Form 706 or the date of filing Form 706 if the

return is filed late. The basis of certain assets when sold or

otherwise disposed of must be consistent with the basis

(estate tax value) of the asset when it was received by the

beneficiary. To satisfy the consistent basis reporting

requirements, the estate must file Form 8971, Information

Regarding Beneficiaries Acquiring Property From a

Decedent, separately from the Form 706. Failure to file Form

8971, when required, is subject to information return

penalties under sections 6721 and 6722. See Form 8971 and

its instructions for more information.

Estate Tax Closing Letters

An estate tax closing letter (ETCL) will not be issued unless a

request is made via Pay.gov. To allow time for processing,

please wait at least 9 months after filing Form 706 to request

an ETCL.

ETCL fee. Effective October 28, 2021, final regulations TD

9957 established a user fee of $67 for persons requesting the

issuance of an ETCL. To make an ETCL request after

October 28, 2021, you must go to Pay.gov to submit a

request and pay the user fee. Go to

Frequently Asked

Questions on the Estate Tax Closing Letter, for instructions

and more information related to ETCLs.

Account transcript in lieu of ETCL. Instead of an ETCL,

the executor of the estate may request an account transcript,

which reflects transactions including the acceptance of Form

706 or the completion of an examination. Account transcripts

are available online to registered tax professionals using the

Transcript Delivery System (TDS) or to authorized

representatives making requests using Form 4506-T. Go to

Transcripts in Lieu of Estate Tax Closing Letters for specific

instructions to request online transcripts using the TDS or

hardcopy transcripts using Form 4506-T.

Note. For information about the release of nonresident U.S.

citizen decedents' assets using transfer certificates under

Regulations section 20.6325-1, go to

Transfer Certificate

Filing Requirements for the Estates of Nonresident Citizens

of the United States or write to:

Internal Revenue Service Center

Attn: E&G, Stop 824G

7940 Kentucky Drive

Florence, KY 41042-2915

Obtaining Forms and Publications To

File or Use

Internet. You can access the IRS website at IRS.gov 24

hours a day, 7 days a week to:

•

Download forms, including talking tax forms, instructions,

and publications;

•

Order IRS products online;

•

Research your tax questions online;

•

Search publications online by topic or keyword;

•

Use the online Internal Revenue Code, regulations, or

other official guidance;

•

View Internal Revenue Bulletins (IRBs) published in the

last few years; and

-4-

Instructions for Form 706 (Rev. 09-2023)

Page 5 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

•

Sign up to receive local and national tax news by email.

Other forms that may be required.

•

Form SS-5, Application for a Social Security Card.

•

Form 706-CE, Certificate of Payment of Foreign Death

Tax.

•

Form 706-NA, United States Estate (and

Generation-Skipping Transfer) Tax Return, Estate of

nonresident not a citizen of the United States.

•

Form 709, United States Gift (and Generation-Skipping

Transfer) Tax Return.

•

Form 712, Life Insurance Statement.

•

Form 2848, Power of Attorney and Declaration of

Representative.

•

Form 4768, Application for Extension of Time To File a

Return and/or Pay U.S. Estate (and Generation-Skipping

Transfer) Taxes.

•

Form 4808, Computation of Credit for Gift Tax.

•

Form 8821, Tax Information Authorization.

•

Form 8822, Change of Address.

•

Form 8971, Information Regarding Beneficiaries

Acquiring Property From a Decedent.

Additional Information. Pub. 559, Survivors, Executors,

and Administrators, may assist you in learning about and

preparing Form 706.

Specific Instructions

You must file the first four pages of Form 706 and all required

schedules. File Schedules A through I, as appropriate, to

support the entries in items 1 through 9 of Part

5—Recapitulation.

Make sure to complete the required pages and

schedules in their entirety. Returns filed without

entries in each field will not be processed.

IF . . .

THEN . . .

you enter zero on any item of the

Recapitulation

you need not file the schedule

(except for Schedule F) referred to on

that item.

you are estimating the value of

one or more assets pursuant to

the special rule of Regulations

section 20.2010-2(a)(7)(ii)

you must report the asset on the

appropriate schedule, but you are not

required to enter a value for the

asset. Include the estimated value of

the asset in the totals entered on Part

5—Recapitulation, items 10 and 23.

you claim an exclusion on item 12 complete and attach Schedule U.

you claim any deductions on items

14 through 22 of the Recapitulation

complete and attach the appropriate

schedules to support the claimed

deductions.

you claim credits for foreign death

taxes or tax on prior transfers

complete and attach Schedule P or

Q.

CAUTION

!

IF . . . THEN . . .

there is not enough space on a

schedule to list all the items

attach a Continuation Schedule (or

additional sheets of the same size) to

the back of the schedule (see the

Continuation Schedule at the end of

Form 706); photocopy the blank

schedule before completing it, if you

will need more than one copy.

Also consider the following.

•

Form 706 has 29 numbered pages.

•

Number the items you list on each schedule, beginning

with the number “1” each time, or using the numbering

convention as indicated on the schedule (for example,

Schedule M).

•

Total the items listed on the schedule and its

attachments, Continuation Schedules, etc.

•

Enter the total of all attachments, Continuation

Schedules, etc., at the bottom of the printed schedule,

but do not carry the totals forward from one schedule to

the next.

•

Enter the total, or totals, for each schedule on page 3,

Part 5—Recapitulation.

•

Do not complete the “Alternate valuation date” or

“Alternate value” columns of any schedule unless you

elected alternate valuation on Part 3—Elections by the

Executor, line 1.

•

When you complete the return, staple all the required

pages together in the proper order.

Part 1—Decedent and Executor

Line 2

Enter the SSN assigned specifically to the decedent. You

cannot use the SSN assigned to the decedent's spouse. If

the decedent did not have an SSN, the executor should

obtain one for the decedent by filing Form SS-5 with a local

Social Security Administration (SSA) office.

Line 6a. Name of Executor

If there is more than one executor, enter the name of the

executor to be contacted by the IRS and see line 6d.

Line 6b. Executor's Address

Use Form 8822 to report a change of the executor's address.

Line 6c. Executor's Social Security Number

Only one executor should complete this line. If there is more

than one executor, see line 6d.

Line 6d. Multiple Executors

Check here if there is more than one executor. On an

attached statement, provide the name, address, telephone

number, and SSN of any executor other than the one named

on line 6a.

Line 11. Special Rule

If the estate is estimating the value of assets under the

special rule of Regulations section 20.2010-2(a)(7)(ii), check

here and see the instructions for

Part 5—Recapitulation,

items 10 and 23.

Instructions for Form 706 (Rev. 09-2023)

-5-

Page 6 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Part 2—Tax Computation

In general, the estate tax is figured by applying the unified

rates shown in Table A to the total of transfers both during life

and at death, and then subtracting the gift taxes, as refigured

based on the date of death rates. See Worksheet TG, the

Line 4 Worksheet, and the Line 7 Worksheet.

Note. You must complete Part 2—Tax Computation.

Line 1

If you elected alternate valuation on Part 3—Elections by the

Executor, line 1, enter the amount you entered in the

“Alternate value” column of Part 5—Recapitulation, item 13.

Otherwise, enter the amount from the “Value at date of death”

column.

Line 3b. State Death Tax Deduction

You may take a deduction on line 3b for estate,

inheritance, legacy, or succession taxes paid on any property

included in the gross estate as the result of the decedent's

death to any state or the District of Columbia.

You may claim an anticipated amount of deduction and

figure the federal estate tax on the return before the state

death taxes have been paid. However, the deduction cannot

be finally allowed unless you pay the state death taxes and

claim the deduction within 4 years after the return is filed, or

later (see section 2058(b)) if:

•

A petition is filed with the Tax Court of the United States,

•

You have an extension of time to pay, or

•

You file a claim for refund or credit of an overpayment

which extends the deadline for claiming the deduction.

Note. The deduction is not subject to dollar limits.

If you make a section 6166 election to pay the federal

estate tax in installments and make a similar election to pay

the state death tax in installments, see section 2058(b) for

exceptions and periods of limitation.

If you transfer property other than cash to the state in

payment of state inheritance taxes, the amount you may

claim as a deduction is the lesser of the state inheritance tax

liability discharged or the fair market value (FMV) of the

property on the date of the transfer. For more information on

the application of such transfers, see the principles

discussed in Rev. Rul. 86-117, 1986-2 C.B. 157, prior to the

repeal of section 2011.

Send the following evidence to the IRS.

1. Certificate of the proper officer of the taxing state, or the

District of Columbia, showing the following.

a. Total amount of tax imposed (before adding interest

and penalties and before allowing discount).

b. Amount of discount allowed.

c. Amount of penalties and interest imposed or

charged.

d. Total amount actually paid in cash.

e. Date of payment.

2. Any additional proof the IRS specifically requests.

File the evidence requested above with the return, if

possible. Otherwise, send it as soon as possible after

the return is filed.

Line 6

To figure the tentative tax on the amount on line 5, use Table

A—Unified Rate Schedule and put the result on this line.

Lines 4 and 7

Three worksheets are provided to help you figure the entries

for these lines. Worksheet TG—Taxable Gifts Reconciliation

allows you to reconcile the decedent's lifetime taxable gifts to

figure totals that will be used for the Line 4 Worksheet and

the Line 7 Worksheet.

You must have all of the decedent's gift tax returns (Forms

709) before completing Worksheet TG—Taxable Gifts

Reconciliation. The amounts needed for Worksheet TG can

usually be found on the filed returns that were subject to tax.

However, if any of the returns were audited by the IRS, use

the amounts that were finally determined as a result of the

audits.

In addition, you must make a reasonable effort to discover

any gifts in excess of the annual exclusion made by the

decedent (or on behalf of the decedent under a power of

attorney) for which no Forms 709 were filed. Include the value

of such gifts in column b of Worksheet TG. The annual

exclusion per donee is as follows.

Table A—Unified Rate Schedule

Column A

Taxable amount over

Column B

Taxable amount not over

Column C

Tax on amount in column A

Column D

Rate of tax on excess over amount

in column A

. . . .

$0 $10,000 $0 18%

10,000 20,000 1,800 20%

20,000 40,000 3,800 22%

40,000 60,000 8,200 24%

60,000 80,000 13,000 26%

80,000 100,000 18,200 28%

100,000 150,000 23,800 30%

150,000 250,000 38,800 32%

250,000 500,000 70,800 34%

500,000 750,000 155,800 37%

750,000 1,000,000 248,300 39%

1,000,000 – – – – 345,800 40%

-6-

Instructions for Form 706 (Rev. 09-2023)

Page 7 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Period

Annual Exclusion Amount Per

Donee

1977 through 1981 $3,000

1981 through 2001 $10,000

2002 through 2005 $11,000

2006 through 2008 $12,000

2009 through 2012 $13,000

2013 through 2017 $14,000

2018 through 2021 $15,000

2022 $16,000

2023 $17,000

Taxable Gift Amount Table

Column A Column B Column C Column D

Amount in Row

(p), Line 7

Worksheet over...

Amount in Row

(p), Line 7

Worksheet not

over...

Property Value

on Amount in

Column A

Rate (Divisor)

on Excess of

Amount in

Column A

0 1,800 0 18%

1,800 3,800 10,000 20%

3,800 8,200 20,000 22%

8,200 13,000 40,000 24%

13,000 18,200 60,000 26%

18,200 23,800 80,000 28%

23,800 38,800 100,000 30%

38,800 70,800 150,000 32%

70,800 155,800 250,000 34%

155,800 248,300 500,000 37%

248,300 345,800 750,000 39%

345,800 – – – – – – 1,000,000 40%

How to complete the Line 7 Worksheet.

Row (a). Beginning with the earliest year in which the taxable

gifts were made, enter the tax period of prior gifts. If you filed

returns for gifts made after 1981, enter the calendar year in

Row (a) as (YYYY). If you filed returns for gifts made after

1976 and before 1982, enter the calendar quarters in Row (a)

as (YYYY-Q).

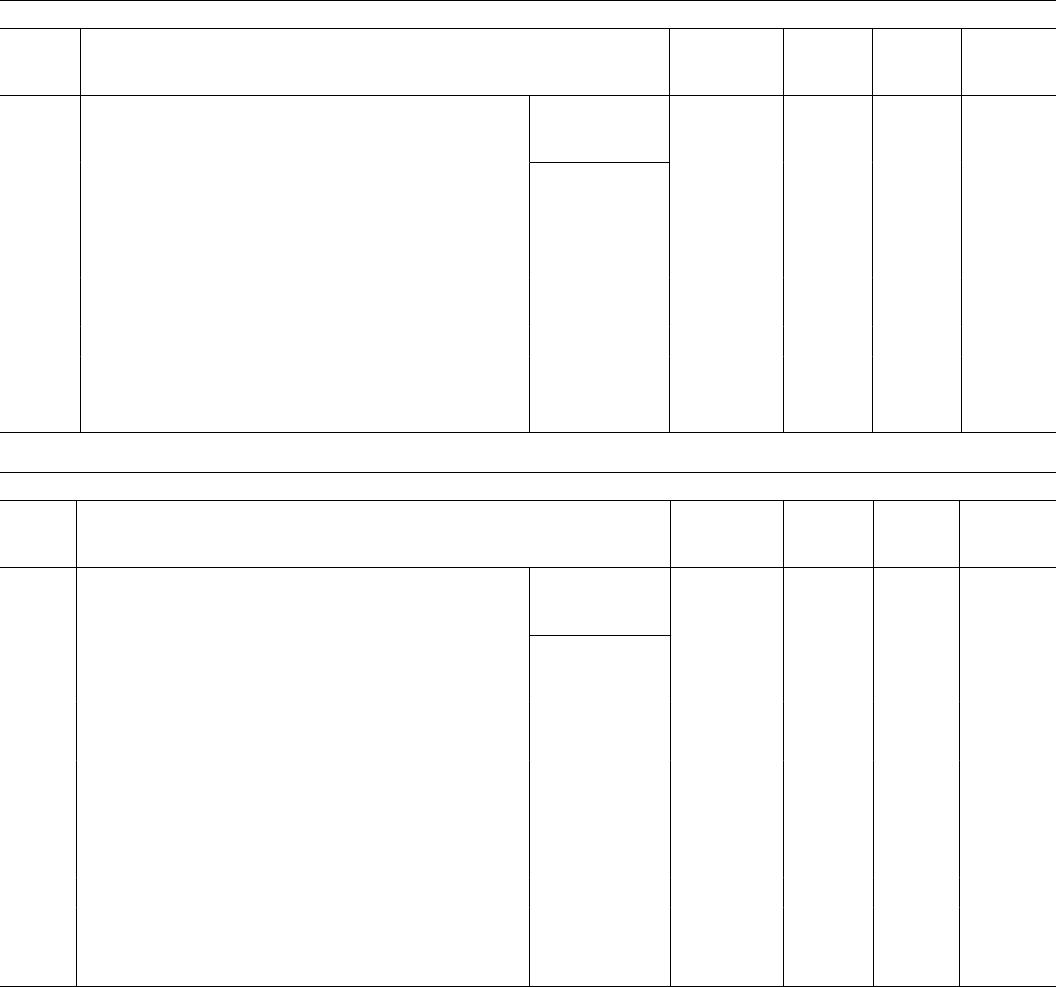

Worksheet TG—Taxable Gifts Reconciliation

Worksheet TG—Taxable Gifts Reconciliation

(To be used for lines 4 and 7 of the Tax Computation)

Gifts

made

after

June 6,

1932,

and

before

1977

a.

Calendar year or

calendar quarter

b.

Total taxable gifts for

period (see Note)

Note. For the definition of a taxable gift, see section 2503. Follow Form 709. That is, include only

the decedent’s one-half of split gifts, whether the gifts were made by the decedent or the

decedent’s spouse. In addition to gifts reported on Form 709, you must include any taxable gifts

in excess of the annual exclusion that were not reported on Form 709.

c.

Taxable amount

included in column b

for gifts included in

the gross estate

d.

Taxable amount included

in column b for gifts that

qualify for “special

treatment of split gifts”

described below

e.

Gift tax paid by

decedent on gifts in

column d

f.

Gift tax paid by

decedent's spouse

on gifts in column c

1. Total taxable gifts

made before 1977

Gifts

made

after

1976

2. Totals for gifts made after

1976

Line 4 Worksheet—Adjusted Taxable Gifts Made After 1976

1. Taxable gifts made after 1976. Enter the amount from Worksheet TG, line 2, column b ......................... 1.

2. Taxable gifts made after 1976 reportable on Schedule G. Enter the amount from Worksheet

TG, line 2, column c ....................................................

2.

3. Taxable gifts made after 1976 that qualify for “special treatment.” Enter the amount from

Worksheet TG, line 2, column d ...........................................

3.

4.

Add lines 2 and 3 ........................................................................ 4.

5. Adjusted taxable gifts. Subtract line 4 from line 1. Enter here and on Part 2—Tax Computation, line 4 ..............

5.

Instructions for Form 706 (Rev. 09-2023)

-7-

Page 8 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Row (b). Enter all taxable gifts made in the specified year.

Enter all pre-1977 gifts in the pre-1977 column.

Row (c). Enter the amount from Row (d) of the previous

column.

Row (d). Enter the sum of Row (b) and Row (c) from the

current column.

Row (e). Enter the amount from Row (f) of the previous

column.

Row (f). Enter the tax based on the amount in Row (d) of the

current column using Table A—Unified Rate Schedule.

Row (g). Subtract the amount in Row (e) from the amount in

Row (f) for the current column.

Row (h). Complete this row only if a DSUE amount was

received from predeceased spouse(s) and was applied to

lifetime gifts or if a Restored Exclusion Amount on taxable

gifts to a same-sex spouse was applied to lifetime gifts (or

both). Enter the sum of lines 2 and 3 from Schedule C on the

Form 709 filed for the year listed in Row (a) for the amount to

be entered in this row.

Row (i). Enter the applicable amount from the Table of Basic

Exclusion Amounts.

Row (j). Enter the sum of Row (h) and Row (i).

Row (k). Figure the applicable credit on the amount in Row

(j) using Table A—Unified Rate Schedule, and enter here.

Line 7 Worksheet—Submit a copy with Form 706

Line 7 Worksheet, Part A—Used to determine Applicable Credit Allowable for Prior Periods after 1976

(a) Tax Period

1

Pre-1977

(b) Taxable Gifts for Applicable Period

(c) Taxable Gifts for Prior Periods

2

(d) Cumulative Taxable Gifts Including Applicable

Period (add Row (b) and Row (c))

(e) Tax at Date of Death Rates for Prior Gifts (from

Row (c))

3

(f) Tax at Date of Death Rates for Cumulative

Taxable Gifts Including Applicable Period (from

Row (d))

(g) Tax at Date of Death Rates for Gifts in

Applicable Period (subtract Row (e) from Row

(f))

(h) Total DSUE applied and Restorable Exclusion

Amount from Prior Periods and Applicable

Period (see instructions later)

(i) Basic Exclusion for Applicable Period (Enter the

amount from the Table of Basic Exclusion

Amounts)

(j) Applicable Exclusion Amount (add Row (h) and

Row (i))

(k) Maximum Applicable Credit amount based on

Row (j) (Using Table A—Unified Rate

Schedule)

4

(l) Applicable Credit amount used in Prior Periods

(add Row (l) and Row (n) from prior period)

(m) Available Credit in Applicable Period (subtract

Row (l) from Row (k))

(n) Credit Allowable (lesser of Row (g) or Row (m))

(o) Tax paid or payable at Date of Death rates for

Applicable Period (subtract Row (n) from Row

(g))

(p) Tax on Cumulative Gifts less tax paid or payable

for Applicable Period (subtract Row (o) from

Row (f))

(q) Cumulative Taxable Gifts less Gifts in the

Applicable Period on which tax was paid or

payable based on Row (p) (Using the Taxable

Gift Amount Table)

(r) Gifts in the Applicable Period on which tax was

payable (subtract Row (q) from Row (d))

Line 7 Worksheet, Part B

1 Total gift taxes payable on gifts after 1976 (sum of amounts in Row (o)).

2 Gift taxes paid by the decedent on gifts that qualify for “special treatment.” Enter the amount from Worksheet TG, line 2, col. e.

3 Subtract line 2 from line 1.

4 Gift tax paid by decedent's spouse on split gifts included on Schedule G. Enter amount from Worksheet TG, line 2, col. f.

5 Add lines 3 and 4. Enter here and on Part 2—Tax Computation, line 7.

6

Cumulative lifetime gifts on which tax was paid or payable. Enter this amount on Form 706, Part 6–Portability of Deceased

Spousal Unused Exclusion (DSUE), Section C, line 3 (sum of amounts in Row (r)).

1

Row (a): For annual returns, enter the tax period as (YYYY). For quarterly returns, enter tax period as (YYYY-Q).

2

Row (c): Enter amount from Row (d) of the previous column.

3

Row (e): Enter amount from Row (f) of the previous column.

4

Row (k): Figure the applicable credit on the amount in Row (j), using Table A—Unified Rate Schedule, and enter here. (For each column in Row (k), subtract 20% of any

amount allowed as a specific exemption for gifts made after September 8, 1976, and before January 1, 1977.)

-8-

Instructions for Form 706 (Rev. 09-2023)

Page 9 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Note. The entries in each column of Row (k) must be

reduced by 20% of the amount allowed as a specific

exemption for gifts made after September 8, 1976, and

before January 1, 1977 (but no more than $6,000).

Row (l). Add the amounts in Row (l) and Row (n) from the

previous column.

Row (m). Subtract the amount in Row (l) from the amount in

Row (k) to determine the amount of any available credit.

Enter the result in Row (m).

Row (n). Enter the lesser of the amounts in Row (g) or Row

(m).

Row (o). Subtract the amount in Row (n) from the amount in

Row (g) for the current column.

Row (p). Subtract the amount in Row (o) from the amount in

Row (f) for the current column.

Row (q). Enter the Cumulative Taxable Gift amount based on

the amount in Row (p) using the Taxable Gift Amount Table.

Row (r). If Row (o) is greater than zero in the applicable

period, subtract Row (q) from Row (d). If Row (o) is not

greater than zero, enter -0-.

Repeat for each year in which taxable gifts were made.

Remember to submit a copy of the Line 7 Worksheet

when you file Form 706. If additional space is needed

to report prior gifts, please attach additional sheets.

CAUTION

!

Table of Basic Exclusion Amounts

Period

Basic Exclusion

Amount

Credit Equivalent

at 2023 Rates

1977 (Quarters 1 and 2) $30,000 $6,000

1977 (Quarters 3 and 4) $120,667 $30,000

1978 $134,000 $34,000

1979 $147,333 $38,000

1980 $161,563 $42,500

1981 $175,625 $47,000

1982 $225,000 $62,800

1983 $275,000 $79,300

1984 $325,000 $96,300

1985 $400,000 $121,800

1986 $500,000 $155,800

1987 through 1997 $600,000 $192,800

1998 $625,000 $202,050

1999 $650,000 $211,300

2000 and 2001 $675,000 $220,550

2002 through 2010 $1,000,000 $345,800

2011 $5,000,000 $1,945,800

2012 $5,120,000 $1,993,800

2013 $5,250,000 $2,045,800

2014 $5,340,000 $2,081,800

2015 $5,430,000 $2,117,800

2016 $5,450,000 $2,125,800

2017 $5,490,000 $2,141,800

2018 $11,180,000 $4,417,800

2019 $11,400,000 $4,505,800

2020 $11,580,000 $4,577,800

2021 $11,700,000 $4,625,800

2022 $12,060,000 $4,769,800

2023 $12,920,000 $5,113,800

Note. In figuring the line 7 amount, do not include any tax

paid or payable on gifts made before 1977. The line 7 amount

is a hypothetical figure used to figure the estate tax.

Special treatment of split gifts. These special rules apply

only if:

•

The decedent's spouse predeceased the decedent;

•

The decedent's spouse made gifts that were “split” with

the decedent under the rules of section 2513;

•

The decedent was the “consenting spouse” for those split

gifts, as that term is used on Form 709; and

•

The split gifts were included in the decedent's spouse's

gross estate under section 2035.

If all four conditions above are met, do not include these

gifts on line 4 of the Tax Computation and do not include the

gift taxes payable on these gifts on line 7 of the Tax

Computation. These adjustments are incorporated into the

worksheets.

Instructions for Form 706 (Rev. 09-2023)

-9-

Page 10 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Lines 9a Through 9e. Applicable Credit Amount

(Formerly Unified Credit Amount)

The applicable credit amount is allowable credit against

estate and gift taxes. It is figured by determining the tentative

tax on the applicable exclusion amount, which is the amount

that can be transferred before an estate tax liability will be

incurred.

The applicable exclusion amount equals the total of lines

9a, 9b, and 9c. See

Lines 9d and 9e, applicable exclusion

and credit amount, later, for more information.

Line 9a, basic exclusion amount. In 2023, the basic

exclusion amount, as adjusted for inflation under section

2010(c)(3), is $12,920,000.

Line 9b, DSUE. If the decedent had a spouse who died after

2010, whose estate did not use all of its applicable exclusion

against gift or estate tax liability, a DSUE amount may be

available for use by the decedent's estate. If the predeceased

spouse died in 2011, the DSUE amount was figured and

attached to the predeceased spouse’s Form 706. If the

predeceased spouse died in 2012 or after, this amount is

found in Part 6, Section C, of the Form 706 filed by the estate

of the decedent's predeceased spouse. The amount to be

entered on line 9b is figured in Part 6, Section D.

Line 9c, restored exclusion amount. If a decedent made a

taxable gift during the decedent's lifetime to the decedent's

same-sex spouse and that transfer resulted in a reduction of

the decedent's available applicable exclusion amount, the

amount of the applicable exclusion that was reduced can be

restored. If the applicable exclusion was previously restored

on a Form 709, enter the value on Schedule C, line 3, of Form

709. If the applicable exclusion has not yet been previously

restored, follow the directions in the instructions for Form

709, Schedule C, to determine the Restored Exclusion

Amount. The Restored Exclusion Amount is entered on

line 9c.

Lines 9d and 9e, applicable exclusion and credit

amount. The total of lines 9a, 9b, and 9c is entered on

line 9d. If the amounts entered on both lines 9b and 9c are

zero, enter $5,113,800 on line 9e. Otherwise, determine the

applicable credit on the amount on line 9d by using Table

A—Unified Rate Schedule and enter the result on line 9e.

Line 10. Adjustment to Applicable Credit

If the decedent made gifts (including gifts made by the

decedent's spouse and treated as made by the decedent by

reason of gift splitting) after September 8, 1976, and before

January 1, 1977, for which the decedent claimed a specific

exemption, the applicable credit amount on this estate tax

return must be reduced. The reduction is figured by entering

20% of the specific exemption claimed for these gifts.

Note. The specific exemption was allowed by section 2521

for gifts made before January 1, 1977.

If the decedent did not make any gifts between September

8, 1976, and January 1, 1977, or if the decedent made gifts

during that period but did not claim the specific exemption,

enter zero.

Line 15. Total Credits

Generally, line 15 is used to report the total of credit for

foreign death taxes (line 13) and credit for tax on prior

transfers (line 14).

However, you may also use line 15 to report credit taken

for federal gift taxes imposed by chapter 12 of the Code, and

the corresponding provisions of prior laws, on certain

transfers the decedent made before January 1, 1977, that are

included in the gross estate. The credit cannot be more than

the amount figured by the following formula.

Gross estate tax minus (the sum of the state

death taxes and unified credit)

x

Value of

included

gift

Value of gross estate minus (the sum of the

deductions for charitable, public, and similar

gifts and bequests and marital deduction)

When taking the credit for pre-1977 federal gift taxes:

•

Include the credit in the amount on line 15; and

•

Identify and enter the amount of the credit you are taking

on the dotted line to the left of the entry space for line 15

on page 1 of Form 706 with a notation, “Section 2012

credit.”

For more information, see the regulations under section

2012. This computation may be made using Form 4808.

Attach a copy of a completed Form 4808 or the computation

of the credit. Also, attach all available copies of Forms 709

filed by the decedent, with "Exhibit to Estate Tax Return"

entered across the top of the first page of each, to help verify

the amounts entered on lines 4 and 7, and the amount of

credit taken (on line 15) for pre-1977 federal gift taxes.

Canadian marital credit. In addition to using line 15 to

report credit for federal gift taxes on pre-1977 gifts, you may

also use line 15 to claim the Canadian marital credit, where

applicable.

When taking the marital credit under the 1995 Canadian

Protocol:

•

Include the credit in the amount on line 15; and

•

Identify and enter the amount of the credit you are taking

on the dotted line to the left of the entry space for line 15

on page 1 of Form 706 with a notation, “Canadian marital

credit.”

Also, attach a statement to the return that refers to the

treaty, waives qualifying domestic trust (QDOT) rights, and

shows the computation of the marital credit. See the 1995

Canadian income tax treaty protocol for details on figuring the

credit.

Part 3—Elections by the Executor

Note. The election to allow the decedent's surviving spouse

to use the decedent's unused exclusion amount is made by

filing a timely and complete Form 706. See the instructions

for

Part 6—Portability of Deceased Spousal Unused

Exclusion, later, and sections 2010(c)(4) and (c)(5).

Line 1. Alternate Valuation

See the example showing the use of Schedule B

where the alternate valuation is adopted, later.

Unless you elect at the time the return is filed to adopt

alternate valuation, as authorized by section 2032, value all

property included in the gross estate as of the date of the

decedent's death. Alternate valuation cannot be applied to

only a part of the property.

You may elect special-use valuation (line 2) in addition to

alternate valuation.

TIP

-10-

Instructions for Form 706 (Rev. 09-2023)

Page 11 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

You may not elect alternate valuation unless the election

will decrease both the value of the gross estate and the sum

(reduced by allowable credits) of the estate and GST taxes

payable by reason of the decedent's death for the property

includible in the decedent's gross estate.

Elect alternate valuation by checking “Yes” on line 1 and

filing Form 706. You may make a protective alternate

valuation election by checking “Yes” on line 1, writing the

word “protective,” and filing Form 706 using regular values.

Once made, the election may not be revoked. The election

may be made on a late-filed Form 706, provided it is not filed

later than 1 year after the due date (including extensions

actually granted). Relief under Regulations sections

301.9100-1 and 301.9100-3 may be available to make an

alternate valuation election or a protective alternate valuation

election, provided a Form 706 is filed no later than 1 year

after the due date of the return (including extensions actually

granted).

If alternate valuation is elected, value the property

included in the gross estate as of the following dates, as

applicable.

•

Any property distributed, sold, exchanged, or otherwise

disposed of or separated or passed from the gross estate

by any method within 6 months after the decedent's

death is valued on the date of distribution, sale,

exchange, or other disposition. Value this property on the

date it ceases to be a part of the gross estate; for

example, on the date the title passes as the result of its

sale, exchange, or other disposition.

•

Any property not distributed, sold, exchanged, or

otherwise disposed of within the 6-month period is

valued as of 6 months after the date of the decedent's

death.

•

Any property, interest, or estate that is affected by mere

lapse of time is valued as of the date of the decedent's

death or on the date of its distribution, sale, exchange, or

other disposition, whichever occurs first. However, you

may change the date of death value to account for any

change in value that is not due to a “mere lapse of time”

on the date of its distribution, sale, exchange, or other

disposition.

The property included in the alternate valuation and

valued as of 6 months after the date of the decedent's death,

or as of some intermediate date (as described above), is the

property included in the gross estate on the date of the

decedent's death. Therefore, you must first determine what

property was part of the gross estate at the decedent's death.

Interest. Interest accrued to the date of the decedent's

death on bonds, notes, and other interest-bearing obligations

is property of the gross estate on the date of death and is

included in the alternate valuation.

Rent. Rent accrued to the date of the decedent's death on

leased real or personal property is property of the gross

estate on the date of death and is included in the alternate

valuation.

Dividends. Outstanding dividends that were declared to

stockholders of record on or before the date of the

decedent's death are considered property of the gross estate

on the date of death and are included in the alternate

valuation. Ordinary dividends declared to stockholders of

record after the date of the decedent's death are not included

in the gross estate on the date of death and are not eligible

for alternate valuation. However, if dividends are declared to

stockholders of record after the date of the decedent's death

so that the shares of stock at the later valuation date do not

reasonably represent the same property at the date of the

decedent's death, include those dividends (except dividends

paid from earnings of the corporation after the date of the

decedent's death) in the alternate valuation.

On Schedules A through I, you must show the following.

1. What property is included in the gross estate on the date

of the decedent's death.

2. What property was distributed, sold, exchanged, or

otherwise disposed of within the 6-month period after the

decedent's death, and the dates of these distributions,

etc. (These two items should be entered in the

“Description” column of each schedule. Briefly explain

the status or disposition governing the alternate

valuation date, such as “Not disposed of within 6 months

following death,” “Distributed,” “Sold,” “Bond paid on

maturity,” etc. In this same column, describe each item of

principal and includible income.)

3. The date of death value, entered in the appropriate value

column with items of principal and includible income

shown separately.

4. The alternate value, entered in the appropriate value

column with items of principal and includible income

shown separately. (In the case of any interest or estate,

the value of which is affected by lapse of time, such as

patents, leaseholds, estates for the life of another, or

remainder interests, the value shown under the heading

“Alternate value” must be the adjusted value, for

example, the value as of the date of death with an

adjustment reflecting any difference in its value as of the

later date not due to lapse of time.)

Note. If any property on Schedules A through I is being

valued pursuant to the special rule of Regulations section

20.2010-2(a)(7)(ii), values for those assets are not required

to be reported on the schedule. See Part 5—Recapitulation,

item 10, later.

Distributions, sales, exchanges, and other dispositions of

the property within the 6-month period after the decedent's

death must be supported by evidence. If the court issued an

order of distribution during that period, you must submit a

certified copy of the order as part of the evidence. The IRS

may require you to submit additional evidence, if necessary.

If the alternate valuation method is used, the values of life

estates, remainders, and similar interests are figured using

the age of the recipient on the date of the decedent's death

and the value of the property on the alternate valuation date.

Line 2. Special-Use Valuation of Section 2032A

In general. Under section 2032A, you may elect to value

certain farm and closely held business real property at its

farm or business use value rather than its FMV. Both

special-use valuation and alternate valuation may be elected.

To elect special-use valuation, check “Yes” on line 2 and

complete and attach Schedule A-1 and its required additional

statements. You must file Schedule A-1 and its required

attachments with Form 706 for this election to be valid. You

may make the election on a late-filed return so long as it’s the

first return filed.

The total value of the property valued under section 2032A

may not be decreased from FMV by more than $1,310,000

for decedents dying in 2023.

Instructions for Form 706 (Rev. 09-2023)

-11-

Page 12 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Real property may qualify for the section 2032A election if:

1. The decedent was a U.S. citizen or resident at the time of

death;

2. The real property is located in the United States;

3. At the decedent's death, the real property was used by

the decedent or a family member for farming or in a trade

or business, or was rented for such use by either the

surviving spouse or a lineal descendant of the decedent

to a family member on a net cash basis;

4. The real property was acquired from or passed from the

decedent to a qualified heir of the decedent;

5. The real property was owned and used in a qualified

manner by the decedent or a member of the decedent's

family during 5 of the 8 years before the decedent's

death;

6. There was material participation by the decedent or a

member of the decedent's family during 5 of the 8 years

before the decedent's death; and

7. The property meets the following percentage

requirements.

a. At least 50% of the adjusted value of the gross estate

must consist of the adjusted value of real or personal

property that was being used as a farm or in a closely

held business and that was acquired from, or passed

from, the decedent to a qualified heir of the

decedent.

b. At least 25% of the adjusted value of the gross estate

must consist of the adjusted value of qualified farm or

closely held business real property.

For this purpose, adjusted value is the value of property

determined without regard to its special-use value. The value

is reduced for unpaid mortgages on the property or any

indebtedness against the property, if the full value of the

decedent's interest in the property (not reduced by such

mortgage or indebtedness) is included in the value of the

gross estate. The adjusted value of the qualified real and

personal property used in different businesses may be

combined to meet the 50% and 25% requirements.

Qualified Real Property

Qualified use. Qualified use means use of the property as a

farm for farming purposes or in a trade or business other than

farming. Trade or business applies only to the active conduct

of a business. It does not apply to passive investment

activities or the mere passive rental of property to a person

other than a member of the decedent's family. Also, no trade

or business is present in the case of activities not engaged in

for profit.

Ownership. To qualify as special-use property, the decedent

or a member of the decedent's family must have owned and

used the property in a qualified use for 5 of the last 8 years

before the decedent's death. Ownership may be direct or

indirect through a corporation, a partnership, or a trust.

If the ownership is indirect, the business must qualify as a

closely held business under section 6166. The indirect

ownership, when combined with periods of direct ownership,

must meet the requirements of section 6166 on the date of

the decedent's death and for a period of time that equals at

least 5 of the 8 years preceding death.

Directly owned property leased by the decedent to a

separate closely held business is considered qualified real

property if the business entity to which it was rented was a

closely held business (as defined by section 6166) for the

decedent on the date of the decedent's death and for

sufficient time to meet the “5 in 8 years” test explained above.

Structures and other real property improvements.

Qualified real property includes residential buildings and

other structures and real property improvements regularly

occupied or used by the owner or lessee of real property (or

by the employees of the owner or lessee) to operate a farm or

other closely held business. A farm residence that the

decedent occupied is considered to have been occupied for

the purpose of operating the farm even when a family

member and not the decedent was the person materially

participating in the operation of the farm.

Qualified real property also includes roads, buildings, and

other structures and improvements functionally related to the

qualified use.

Elements of value such as mineral rights that are not

related to the farm or business use are not eligible for

special-use valuation.

Property acquired from the decedent. Property is

considered to have been acquired from or to have passed

from the decedent if one of the following applies.

•

The property is considered to have been acquired from

or to have passed from the decedent under section

1014(b) (relating to basis of property acquired from a

decedent).

•

The property is acquired by any person from the estate.

•

The property is acquired by any person from a trust, to

the extent the property is includible in the gross estate.

Qualified heir. A person is a qualified heir of property if the

person is a member of the decedent's family and acquired or

received the property from the decedent. If a qualified heir

disposes of any interest in qualified real property to any

member of the qualified heir’s family, that person will then be

treated as the qualified heir for that interest.

A member of the family includes only:

•

An ancestor (parent, grandparent, etc.) of the individual;

•

The spouse of the individual;

•

The lineal descendant (child, stepchild, grandchild, etc.)

of the individual, the individual's spouse, or a parent of

the individual; or

•

The spouse or surviving spouse of any lineal descendant

described above.

Note. A legally adopted child of an individual is treated as a

child of that individual by blood.

Material Participation

To elect special-use valuation, either the decedent or a

member of the decedent’s family must have materially

participated in the operation of the farm or other business for

at least 5 of the 8 years ending on the date of the decedent's

death. The existence of material participation is a factual

determination. Passively collecting rents, salaries, draws,

dividends, or other income from the farm or other business is

not sufficient for material participation, nor is merely

advancing capital and reviewing a crop plan and financial

reports each season or business year.

-12-

Instructions for Form 706 (Rev. 09-2023)

Page 13 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

In determining whether the required participation has

occurred, disregard brief periods (that is, 30 days or less)

during which there was no material participation, as long as

such periods were both preceded and followed by substantial

periods (more than 120 days) during which there was

uninterrupted material participation.

Retirement or disability. If, on the date of death, the time

period for material participation could not be met because the

decedent was retired or disabled, a substitute period may

apply. The decedent must have retired on social security or

been disabled for a continuous period ending with death. A

person is disabled for this purpose if the person was mentally

or physically unable to materially participate in the operation

of the farm or other business.

The substitute time period for material participation for

these decedents is a period totaling at least 5 years out of the

8-year period that ended on the earlier of:

•

The date the decedent began receiving social security

benefits, or

•

The date the decedent became disabled.

Surviving spouse. A surviving spouse who received

qualified real property from the predeceased spouse is

considered to have materially participated if the surviving

spouse was engaged in the active management of the farm

or other business. If the surviving spouse died within 8 years

of the first spouse's death, you may add the period of

material participation of the predeceased spouse to the

period of active management by the surviving spouse to

determine if the surviving spouse's estate qualifies for

special-use valuation. To qualify for this, the property must

have been eligible for special-use valuation in the

predeceased spouse's estate, though it does not have to

have been elected by that estate.

For additional details regarding material participation, see

Regulations section 20.2032A-3(e).

Valuation Methods

The primary method of valuing special-use property that is

used for farming purposes is the annual gross cash rental

method. If comparable gross cash rentals are not available,

you can substitute comparable average annual net share

rentals. If neither of these is available, or if you so elect, you

can use the method for valuing real property in a closely held

business.

Average annual gross cash rental. Generally, the

special-use value of property that is used for farming

purposes is determined as follows.

1. Subtract the average annual state and local real estate

taxes on actual tracts of comparable real property from

the average annual gross cash rental for that same

comparable property.

2. Divide the result in (1) by the average annual effective

interest rate charged for all new federal land bank loans.

See

Effective interest rate, later.

The computation of each average annual amount is based

on the 5 most recent calendar years ending before the date

of the decedent's death.

Gross cash rental. Generally, gross cash rental is the

total amount of cash received in a calendar year for the use

of actual tracts of comparable farm real property in the same

locality as the property being specially valued. You may not

use:

•

Appraisals or other statements regarding rental value or

areawide averages of rentals,

•

Rents paid wholly or partly in-kind, or

•

Property for which the amount of rent is based on

production.

The rental must have resulted from an arm's-length

transaction and the amount of rent may not be reduced by

the amount of any expenses or liabilities associated with the

farm operation or the lease.

Comparable property. Comparable property must be

situated in the same locality as the qualified real property as

determined by generally accepted real property valuation

rules. The determination of comparability is based on a

number of factors, none of which carries more weight than

the others. It is often necessary to value land in segments

where there are different uses or land characteristics

included in the specially valued land.

The following list contains some of the factors considered

in determining comparability.

•

Similarity of soil.

•

Whether the crops grown would deplete the soil in a

similar manner.

•

Types of soil conservation techniques that have been

practiced on the two properties.

•

Whether the two properties are subject to flooding.

•

Slope of the land.

•

For livestock operations, the carrying capacity of the

land.

•

For timbered land, whether the timber is comparable.

•

Whether the property as a whole is unified or segmented.

If segmented, the availability of the means necessary for

movement among the different sections.

•

Number, types, and conditions of all buildings and other

fixed improvements located on the properties and their

location as it affects efficient management, use, and

value of the property.

•

Availability and type of transportation facilities in terms of

costs and of proximity of the properties to local markets.

You must specifically identify on the return the property

being used as comparable property. Use the type of

descriptions used to list real property on Schedule A.

Effective interest rate. See Tables 1 and 2 of Rev. Rul.

2023-15, 2023-34 I.R.B. 559, available at Rev. Rul. 2023-15,

for the average annual effective interest rates in effect for

2023.

Net share rental. You may use average annual net share

rental from comparable land only if there is no comparable

land from which average annual gross cash rental can be

determined. Net share rental is the difference between the

gross value of produce received by the lessor from the

comparable land and the cash operating expenses (other

than real estate taxes) of growing the produce that, under the

lease, are paid by the lessor. The production of the produce

must be the business purpose of the farming operation. For

this purpose, produce includes livestock.

The gross value of the produce is generally the gross

amount received if the produce was disposed of in an

arm's-length transaction within the period established by the

Department of Agriculture for its price support program.

Otherwise, the value is the weighted average price for which

the produce sold on the closest national or regional

commodities market. The value is figured for the date or

Instructions for Form 706 (Rev. 09-2023)

-13-

Page 14 of 59 Fileid: … ons/i706/202309/a/xml/cycle03/source 12:20 - 5-Sep-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

dates on which the lessor received (or constructively

received) the produce.

Valuing a real property interest in a closely held busi-

ness. Use this method to determine the special-use

valuation for qualifying real property used in a trade or

business other than farming. You may also use this method

for qualifying farm property if there is no comparable land or if

you elect to use it. Under this method, the following factors

are considered.

•

The capitalization of income that the property can be

expected to yield for farming or for closely held business

purposes over a reasonable period of time with prudent

management and traditional cropping patterns for the

area, taking into account soil capacity, terrain

configuration, and similar factors.

•

The capitalization of the fair rental value of the land for

farming or for closely held business purposes.

•

The assessed land values in a state that provides a

differential or use value assessment law for farmland or

closely held business.

•

Comparable sales of other farm or closely held business

land in the same geographical area far enough removed