Bloomberg Fixed Income Indices

Bloomberg Fixed Income Index Methodology 1

Bloomberg Fixed Income

Index Methodology

December 15, 2023

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 2

Version Tracker*:

Date Update

12 December 2018

Methodology Update for BMR requirements

29 April 2020

Methodology Update for ESG disclosures, as well as index changes and clarifications since previous

version

24 August 2021

Methodology Update for end of co-branding agreement, and rules changes and clarifications since

previous version

26 April 2023

Methodology Update for pricing snap times, MBS factor date, default definition, and rules changes

and clarifications since previous version. ESG BMR disclosures updated.

29 September 2023

Methodology Update for FX hedging changes, market disruption, removal of redundant sections, ESG

BMR disclosures updated.

13 December 2023

Methodology Update for sanctions language, Bloomberg tickers, and rule clarifications since previous

version.

*For the latest updates and rules clarifications since the last version noted above, please see INP<GO> on the Bloomberg Terminal

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 3

Table of Contents

Introduction 8

Benchmark Index Solutions 8

Benchmark Index Design Principles 11

Design Principles 11

Understanding Portfolio Uses of Benchmark Indices 11

Fundamental Design Questions to Construct a Fixed Income Index 11

BISL Benchmark Index Governance 12

Benchmark Index Eligibility Rules 13

Currency 14

Local Currency Market Inclusion 14

Global Aggregate Index Market Inclusion 14

EM Local Currency Government Index Market Inclusion 14

World Government Inflation-Linked Bond Index (“WGILB”) Market Inclusion 15

Sector 17

Bloomberg Fixed Income Classification System 17

Sector Hierarchy and Definitions for Taxable Indices 18

Sector Assignment and Reclassifications 21

Municipal Index Classifications 22

Municipal Index Classifications 22

Credit Quality 24

Bloomberg Index Rating 24

Sovereign Ratings 25

Classifications when Bond-Level Ratings are Unavailable 25

Use of Expected Ratings 25

Issuer Ratings 25

Ratings for Pfandbriefe 25

Average Quality at the Index Level 25

Defaulted Securities 26

Minimum Amount Outstanding 26

Local Currency Minimums 27

Global Aggregate and EM Local Currency Minimum Issue Sizes 27

Inflation-Linked Indices 28

US Aggregate Minimum Issue Sizes 28

Other Bloomberg Flagship Indices 28

Municipal Indices 29

Minimum Market Size 29

Float Adjustments to Amount Outstanding 29

US Treasuries 29

Float Adjustments for Other Markets 29

Other Amount Outstanding Eligibility Rules 30

Called Securities 30

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 4

Sinkable Bonds 30

Agency MBS Prepayments 30

Pay-in-Kind Securities 30

Maturity 30

Index Eligibility and Classification by Maturity 30

Sub-Indices by Maturity 31

Country 31

Country Classification 31

Initial Issuer Country Assignment and Review 32

Bloomberg Indices’ Emerging Markets Country List 32

Offshore entities 32

Market of Issue 35

Market of Issue Criteria 36

US Indices 36

Other Regional Aggregate Indices 37

Taxability 38

Taxability of Debt versus Equity 38

Taxable versus Tax-Exempt Bonds 38

Build America Bonds (“BAB”) 38

Calculation of Index Returns 39

Subordination 39

Secured Bonds 39

Senior Debt 39

Subordinated Debt 40

Capital Securities 40

Benchmark Index Rebalancing Rules 41

Benchmark Returns and Projected Universes 41

Bloomberg “Index Flags” 42

Index Rebalancing Dynamics 44

Index Turnover 44

Duration Extension 45

Other Index Rebalancing Mechanics 46

Settlement Assumptions 46

Holiday Calendars 47

Timing of New Issues 48

Rebalancing Details for Other Indices 48

Benchmark Index Pricing and Analytics 49

Benchmark Index Pricing 49

Pricing and Other Sources 49

Pricing Verification 49

Pricing Quote Conventions 50

Pricing Timing and Frequency 50

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 5

Pricing Settlement Assumptions 50

Benchmark Index Analytics 51

Duration 51

Convexity 51

Spread 52

Yield 52

Derived and Model-Driven Analytics 53

Benchmark Index Returns Calculations and Weighting Rules 53

Bond Total Return Calculations 53

Monthly Price Return 54

Monthly Coupon Return 54

Monthly Paydown Return 54

Monthly Currency Return 55

Bond Excess Return Calculations 56

Index Weight Calculations 56

Market Value Weights 56

Index Return Calculations and Aggregation 58

Monthly Index Return Calculations 58

Cumulative and Periodic Total Return Calculations 58

Periodic Excess Return Calculations 58

Duration Hedged/Mirror Futures Index Return Calculations 58

ESG Benchmarks 59

Accessing Indices 59

Bloomberg Terminal® 59

Bloomberg Indices Website 60

Data Distribution 60

Index Licensing 60

Appendices 61

Appendix 1: Total Return Calculations 61

Total Return Calculations (Series-B Indices) 63

Appendix 2: Index Rules for Currency Hedging and Currency Returns 65

Unhedged Returns 65

Hedged Returns 65

End-of-Month Roll of Currency Hedging Positions 67

Using Hedges of Longer Tenors 67

Common Questions about Currency Returns for Bloomberg Indices 67

Currency Returns and Hedging for Series-B Indices 71

Unhedged and Hedged Return Indices 72

Foreign Currency: Total Return Index (Unhedged) 72

Hedged Return Calculations 72

Appendix 3: Detailed Discussion of Excess Return Computations 76

Using Key Rate Duration to Compute Excess Returns 76

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 6

Calculating Excess Returns Using KRDs 76

Duration-Bucket Approach 77

Approximating Excess Returns from OAS 77

OAS-Based Excess Return Calculation 77

Calculating Periodic and Cumulative Excess Returns 78

Appendix 4: Benchmark Index Pricing Methodology 80

US Aggregate Index Components 80

US Treasury, US Agency, US Credit/Corporate (Investment Grade), US CMBS, US Fixed-Rate ABS Indices 80

US MBS Index 80

Other US Indices 81

US Corporate High Yield Index 81

US Municipal Bond Index 81

US Floating-Rate ABS Index 82

Pan-European Indices 82

Euro Treasury, Euro Government (Series-B), UK Gilt (Series-L and Series-B), and Pan-European Government-Related,

Securitised (Fixed Coupon) and Corporate Indices 82

Pan-European ABS FRN Index 83

Other Pan-European Indices 83

Pan-European High Yield Corporate Index 83

Euro and Sterling Treasury Bills Indices 83

Pan-European Corporate FRN Index 84

Other Pan-European Local Currency Indices 84

Asian-Pacific Indices 84

Japanese Government Bond Index 84

Other JPY-Denominated Corporate, Government-related and Securitized Indices 85

Other Asian-Pacific Aggregate Components 85

EM Local Currency Government Index-Eligible Currencies 85

EM Hard Currency Aggregate Indices 86

Price Timing & Conventions for Nominal Bonds and Convertibles 86

Inflation-Linked Indices 88

Universal Government Inflation-Linked Bond Index (“UGILB”) 88

World Government Inflation-Linked Bond Index (“WGILB”) 88

EM Government Inflation-Linked Bond Index (“EMGILB”) 88

Global Inflation-Linked Bond Index (“Series-L”) 88

Appendix 5: Bloomberg Fixed Income Classification System and Codes 90

Appendix 6: Glossary of Terms – Index Terms 92

Appendix 7: Glossary of Terms – Index Analytics 98

Appendix 8: Glossary of Terms – Index Aggregation Values 100

Appendix 9: Index Governance 101

Appendix 10: Methodology considerations 102

General Methodology Considerations 102

Limitations of the Indices 102

Third Parties 102

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 7

Expert Judgment 102

Reinvestment of Dividends and Coupons 103

Appendix 11: Environmental, Social and Governance Disclosures 104

Appendix 12: Index Identification and Publication Currency 104

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 8

Introduction

Our global family of fixed income indices traces its history to 1973 when the first total return

bond index was created. For nearly fifty years, the Bloomberg Fixed Income Indices have been

the market standard for fixed income investors seeking objective, rules-based, and

representative benchmarks to measure asset class risk and return. The Bloomberg Fixed

Income benchmark indices have been designed to measure the risk and return characteristics

of the global fixed income markets in an objective manner.

While Bloomberg Index Services Limited (“BISL” and with its affiliates, “Bloomberg”) publishes a

wide range of index primers, factsheets, rules documents, technical notes, and index specific

research in support of the Bloomberg Fixed Income Indices, the scope of our offering can make

it a challenge for both new and experienced index users to get a full overview of the

methodology in a single publication. This document supplements these index-specific

documents to detail information for the Bloomberg Fixed Income Indices in a single

publication.

In particular, this methodology document will cover:

● Index eligibility criteria and inclusion rules

● Rebalancing rules and mechanics

● Return calculations, analytics and pricing conventions

● Weighting and aggregation rules

A user should read an index specific methodology document in conjunction with this document

in order to understand the rules that apply to a particular index. Glossaries of terms used in this

document are set out in Appendices 6, 7 and 8.

Benchmark Index Solutions

Benchmark indices are used by global investors for three primary purposes: 1) as portfolio

performance targets, 2) as informational measures of security-level and asset class risk and

return characteristics, and 3) as references for index-linked products. Bloomberg offers index

users a number of benchmark-related services and solutions supporting these primary uses in

the portfolio management process.

Customized Benchmark Index Solutions

With the proliferation of standard benchmark indices offered as part of the benchmark index

platform, there has been increased demand for bespoke measures of asset classes that may be

more consistent with investor-specific portfolio objectives.

Bloomberg recognizes that no single benchmark design is universal or appropriate for all

investors. Our goal is to offer a broad and evolving suite of unbiased index products from which

investors may select or customize the most appropriate benchmark for their portfolio needs. In

addition to our flagship indices, Bloomberg now publishes thousands of bespoke benchmarks

and actively works with index users in a consultative manner on benchmark design,

methodology, back-testing, selection, and documentation of their custom indices. The types of

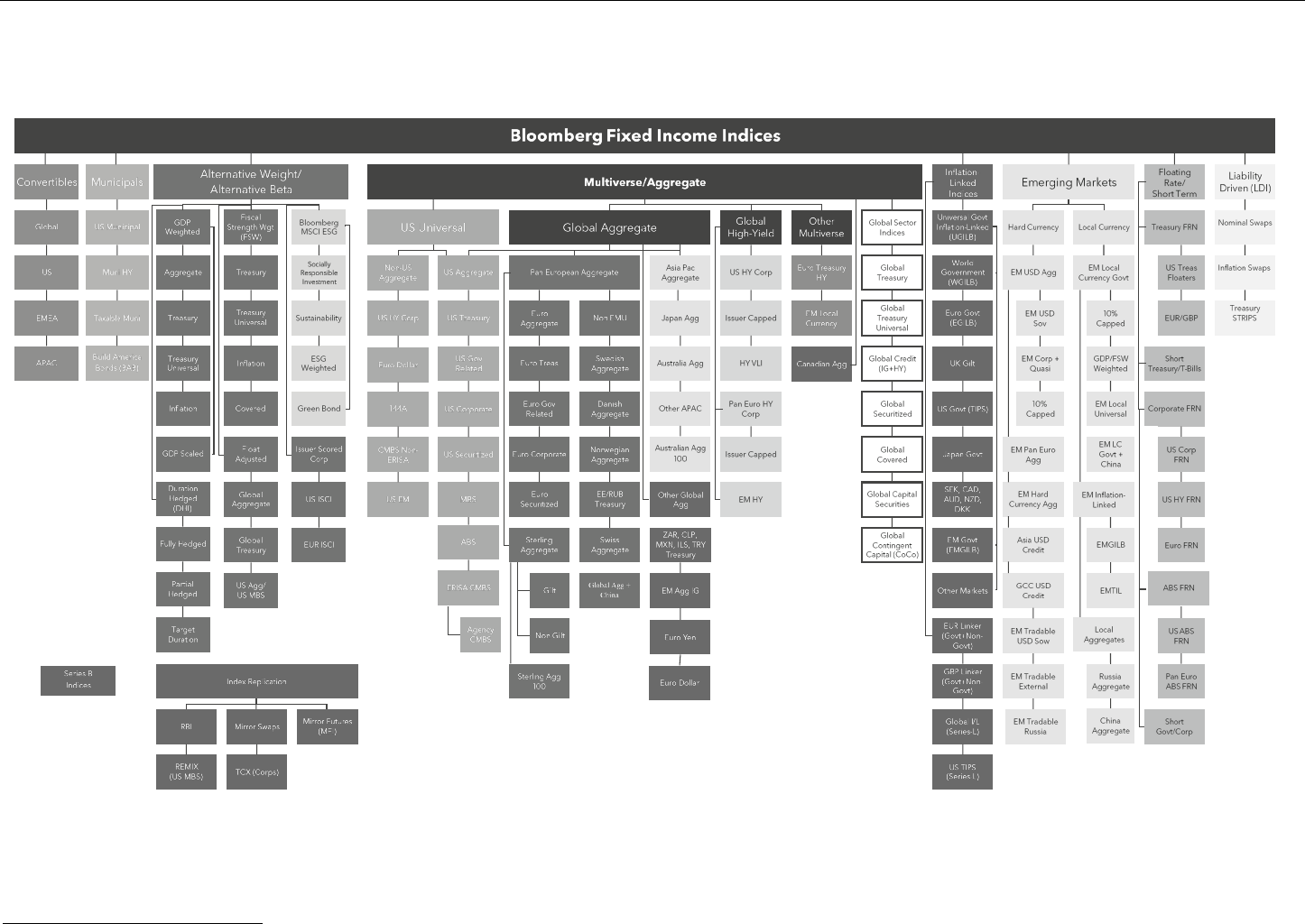

customizations available through the index platform are shown in Figure 1.

Figure 1

Common Types of Index Customizations

Sub-Index Type

Description

Examples

Enhanced Constraint

Applies a more or less stringent set of

constraints to any existing index.

Global Aggregate ex Baa

Global Aggregate 1-3 Year

Composites

Investors assign their own weights to sectors

or other index sub-components within an

overall index.

50% Global Treasury; 50% Global

Aggregate ex Treasury

Issuer Constrained

Indices that cap issuer exposure to a fixed

percentage. Options available for applying

Global Aggregate 2% Issuer

Capped

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 9

issuer caps and redistributing excess MV to

other issuers.

“Smart Beta”/ Alternative

Weights

Uses other rules-based weighting schemes

instead of market value weights.

Global Aggregate GDP Weighted

Global Aggregate Fiscal Strength

Weighted

ESG Screened/Weighted

Applies Environmental, Social and Governance

filters and/or tilts to a standard index.

Global Corporate Socially

Responsible Index

Global Aggregate ESG Weighted

Duration Hedged

Indices constructed to reflect the underlying

return of an index with its duration fully or

partially hedged using a futures-based

replication (Mirror Futures Index).

Global Aggregate Duration

Hedged Index

Replication Strategies

The index team offers tools for clients seeking to passively replicate fixed income benchmarks

with cash bonds and/or isolate fixed income beta through other strategies and products so that

it may be repackaged in new ways (e.g., portable alpha strategies). Bloomberg also licenses its

indices to third parties for use in index replication products, such as ETFs.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 10

Figure 2

Bloomberg Fixed Income Indices

1

1

While this methodology intends to cover the general construction of most Bloomberg indices, not all of the rules discussed in this publication apply to all indices (e.g. Convertibles), while other indices have differing

methodologies (e.g. Index Replication, Breakeven Inflation, Leveraged, etc.). Hence, these other indices are covered in separate publications. See INP<Go> on the Terminal in accessing these supplemental materials.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 11

Benchmark Index Design Principles

The Bloomberg Fixed Income Indices adhere to the following core design principles:

● Representative of the market or asset class being measured and the desired risk exposures

sought by index users.

● Replicable, offering a sufficiently sized universe without unnecessary turnover and

transaction costs.

● Objective and transparent, with clearly defined and objective rules, as well as daily visibility

into current index composition and future composition during rebalancing.

● Relevant as investment benchmarks for a diverse set of index uses, including both actively

and passively managed portfolios.

The Bloomberg Fixed Income Indices are designed to meet these fundamental criteria, as all

indices are rules-based with inclusion determined by transparent eligibility criteria that have

been set to accurately and comprehensively measure different fixed income asset classes.

Additionally, comprehensive statistics for each index are readily available to index users, with

performance statistics available daily for most indices.

The principal objective of this

document is to guide users

through each step of index

design to better understand

the rules, methodologies and

conventions of Bloomberg

Fixed Income Indices

Design Principles

Understanding Portfolio Uses of Benchmark Indices

BISL tends to observe three common uses for fixed income indices, which influence preferences

in index design and benchmark construction.

• Portfolio Performance Targets

• Informational Measures of Asset Class Risk and Return

• References for Index-Linked Products

Given the variety of uses, BISL recognizes that no single benchmark design is universal or

appropriate for all investors. The goal of Bloomberg Fixed Income Indices is to offer a broad,

innovative and evolving suite of fixed income indices from which investors are able to select or

customize the most appropriate benchmark for their portfolio needs. The “right” fixed income

index can be viewed as the most appropriate and replicable benchmark for a specific portfolio

objective within the context of the dedicated portfolio as well as part of an overall asset

allocation mix. As an index provider, BISL remains impartial to the benchmark selection

decisions made by investors.

Fundamental Design Questions to Construct a Fixed Income Index

Each benchmark within the Bloomberg fixed income benchmark index platform can be

differentiated and summarized by the answers to three fundamental design questions: 1) what

investment universe is the index intending to measure?, 2) how are the return and risk

characteristics of index-eligible securities measured?, and 3) how are security-level returns and

risk characteristics weighted and aggregated to the index level?

What investment universe is the index trying to measure?

The answer here defines the universe of securities that an investor considers to be part of their

choice set. This can be explicitly defined in an investor’s portfolio guidelines, but may also

include a broader risk budget to out-of-index securities not specified by investment guidelines.

From that defined universe, the benchmark must define index-eligible securities with objective,

rules-based and transparent eligibility criteria that represent and measure the desired asset

class.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 12

How are the risk and return characteristics of eligible securities measured?

Once an investment/index universe is defined, these securities must be measured from both a

return (pricing, coupon and principal payments) and a risk (duration, convexity and spread)

perspective.

How are security-level returns and risk characteristics weighted and aggregated to the

index level?

With these security-level risk and return characteristics measured, they must then be

aggregated to a summary or index level. How frequently the indices are rebalanced and how

the relative weights of index-eligible securities are determined are key considerations to arrive

at a final index construction.

The principal objective of this document is to guide index users through each of these steps of

the index design process to better understand existing index rules, methodologies, and

conventions for flagship Bloomberg Indices and their evolution.

BISL Benchmark Index Governance

Please see the BISL Benchmark Procedures Handbook for details on BISL’s index governance

and control framework.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 13

Benchmark Index Eligibility Rules

Index inclusion of individual securities and the application of published index rules are

determined by clearly defined, published eligibility criteria.

A common core set of

security-level attributes are

used to determine index

eligibility for most fixed

income indices

The central design of any fixed income index starts with an evaluation of security attributes to

determine whether a bond will be index eligible as of the rebalancing date. While the threshold

for inclusion varies from index to index, most benchmarks evaluate a core set of common

attributes.

This section explains the most commonly used bond index eligibility criteria and how they are

applied to a variety of Bloomberg benchmark fixed income index families. The criteria include:

● Currency denomination of a bond’s principal and interest payments.

● Sector classification of the bond issuer, recognizing the wide range of issuer types in the

fixed income market including corporate, government and securitized borrowers.

● Credit quality of a bond as measured by the ratings agencies, Moody’s, Standard and

Poor’s, and Fitch.

2

This is important for index users with investment guidelines that make a

clear distinction between investment grade (rated Baa and higher) and high yield (rated Ba

and lower) securities.

● Amount outstanding of a bond, with larger bonds generally more widely held by investors

and viewed as more liquid.

● Time to maturity of a bond’s principal repayment.

● Country of risk of the issuing entity, especially in cases where an investor may make a

distinction between developed and emerging markets in their portfolios.

● Market of issue/placement type of a security reflecting whether a bond is (or will soon be)

publicly registered, exempt from registration or privately placed. This also indicates whether

a bond is being marketed and sold to local investors only, non-local investors or globally

offered in multiple markets.

● Taxability of a security’s cash flows and principal payments from an issuer’s and an

investor’s perspective. From the issuer perspective, distinctions are made when cash

payments are made by a borrower on a pre-tax basis (debt) vs. after-tax basis (equity

dividend). From the investor perspective, bonds that offer tax-exempt proceeds (particularly

US municipal securities) are generally bought by a different investor base than taxable

bonds.

● Subordination of a security, which identifies where an investor’s claim is within the

borrower’s capital structure, distinguishing between bonds whose holders have senior

claims and those whose holders have subordinated claims in a credit event.

Additional attributes that are used to determine index inclusion include whether a bond

contains explicit optionality on the earlier repayment of principal (callable, putable, etc.), the

coupon type used to determine interest payments (fixed- vs. floating-rate), as well as other

considerations, such as sanctions.

3

As fixed income markets continue to evolve, new types of bond features and structures are

brought to market. When evaluating new security types for the purposes of index eligibility,

BISL takes a number of factors into account, including, but not limited to, existing index rules,

eligibility precedents of similar types of debt and the views of clients and internal research

teams. Often, index eligibility rules are reviewed as part of the formal index governance proces

2

Canada Aggregate family of indices additionally employ DBRS bond ratings beginning in August 2018.

3

New and/or existing debt issued by entities placed on relevant lists and/or programs enforced by the 1) U.S. Department of the Treasury's Office of Foreign Assets

Control ("OFAC"); 2) UK HM Treasury Office of Financial Sanctions Implementation ("OFSI"); and 3) European Union ("EU") are considered restricted and are not eligible

for Bloomberg Indices.

Relevant lists and regulations include, but are not limited to: 1) OFAC's Specially Designated Nationals and Blocked Persons ("SDN") list, 2) Schedule 2 of OFSI's Russia

(Sanctions) (EU Exit) Regulations 2019, and 3) Transferable securities and money-market instruments captured under relevant articles of Council Regulation (EU) No

833/2014. If a sanctions regime is no longer applicable, BISL will review the affected instruments to determine eligibility for inclusion in the index based on all other index

eligibility criteria.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 14

Currency

The Bloomberg benchmark fixed income index platform offers broad-based indices

denominated in a single currency, such as the US Aggregate (“USD”) and Euro Aggregate

(“EUR”) Indices, as well as multi-currency benchmarks, such as the Global Aggregate and EM

Local Currency Government Indices. Returns on multi-currency indices are calculated on both

an unhedged and a currency hedged basis in a number of reporting currencies. Additionally,

returns for single-currency indices are available in currencies other than that of the index.

For index purposes, the determination of a bond’s currency is generally straightforward, as its

prospectus and other publicly available sources will clearly state the currency denomination of

principal and coupon payments. The primary index consideration is whether a particular local

currency bond market should qualify for certain broad-based indices. Bloomberg evaluates

local currency inclusion candidates for benchmarks such as the Global Aggregate and EM Local

Currency Government to ensure that inclusion candidates meet broader index rules and are

sufficiently investable. Local currency debt markets may also be removed from existing indices if

there is a significant impairment to the investability of the market.

A bond’s currency is also important for identifying the appropriate reference curves to calculate

security risk characteristics (duration, convexity, spread, etc.).

Local Currency Market Inclusion

The eligibility of local currency debt markets in broad-based, multi-currency indices is reviewed

annually by BISL. Historical inclusion by market is listed in Figure 2.

Global Aggregate Index Market Inclusion

To be a candidate for inclusion in broad-based, investment grade indices, such as the Global

Aggregate Index, a local currency debt market must exhibit several necessary (but not, by

themselves, sufficient) characteristics:

● Sovereign debt rating (long term local currency) must be investment grade using the index

credit quality classification methodology (middle rating of Moody’s, Fitch and S&P).

● The currency must be freely tradable and convertible and not exposed to exchange

controls that are designed to encumber its buying and selling by foreign investors.

● There must be an established and developed forward market or non-deliverable

forward (NDF) market for the local currency such that foreign market participants can

hedge their exposures into core currencies.

Other aspects of local market investability (market size, settlement and clearing, capital controls

and tax regimes, secondary market liquidity, accessibility for foreign investors, etc.) are

considered when assessing a market’s potential inclusion. BISL considers these factors while

determining whether a market is eligible for inclusion in the Global Aggregate Index.

EM Local Currency Government Index Market Inclusion

Local market inclusion in flagship Emerging Markets Local Currency indices is also evaluated on

an annual basis and requires an established forward or NDF market for hedging for offshore

investors. The initial criterion for inclusion in this index family is whether a country is classified as

an emerging market under the indices’ EM definition.

New market inclusion is also based on a minimum market size requirement of USD5bn of index-

eligible debt. Other EM-specific evaluations of investability, including capital controls and local

market accessibility for offshore investors, are considered.

Because the accessibility of local EM debt is variable and often depends on whether an investor

has an onshore presence, markets commonly characterized as difficult to gain exposure to

4

are

not included in the flagship EM Local Currency Government Index, but instead are eligible for

the broader EM Local Currency Government Universal Index. The Egyptian, Indian and

4

This is generally due to the presence of capital controls, quotas or other institutional constraints.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 15

Taiwanese government bond markets are tracked but included only in the EM Local

Government Universal Index, the broadest measure of EM local debt.

5

EM Local Currency Bonds that Settle Globally

Globally settled bonds that pay principal and accrue interest in local currency, but settle in USD

are classified as local currency bonds and qualify for local currency benchmarks. These

securities offer exposure to local currency government debt (both sovereign credit and local

FX) and are less likely to be subjected to local taxation than locally settled bonds.

World Government Inflation-Linked Bond Index (“WGILB”) Market Inclusion

The WGILB is designed to include only those markets and securities in which a global

government linker fund is likely and able to invest. To be considered for index inclusion, any

new market must first satisfy the credit rating threshold of A3/A- for G7 and euro area countries

and Aa3/Aa- otherwise (using the index credit quality methodology).

Having fulfilled the qualitative assessment, an eligible market must then fulfil the minimum

market size criterion. New eligible markets must meet a minimum market size, based on

uninflated amount outstanding, of USD4bn using Refinitiv: WM/Reuters Closing Spot Rates at

4pm London time as of the last business day of each quarter. If an eligible market meets the

minimum market size, it will be added to the WGILB at the end of the following quarter.

The quarterly market size assessment applies only to developed markets that have initiated a

new linker program or revived an inactive one. For markets already included in the WGILB

Index, market size is reviewed on an annual basis, concurrently with the annual governance

process. Once added to the WGILB, the threshold for each market is lowered to USD2bn to

prevent unnecessary turnover due to short-term fluctuations, particularly in foreign exchange.

5

Croatia and Egypt exited the flagship EM Local Currency Government Index in April 2014. Croatia was included in the EM Local Government Universal Index until

December 2022, at which point it exited the index due to Croatia’s adoption of the Euro from January 1, 2023.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 16

Figure 3

Index Inclusion by Currency

Currency Global Aggregate Inclusion

World Government Inflation-Linked

Bond Index (WGILB) Inclusion

EM Local Currency Government

Inclusion

Argentine peso (ARS) - -

July 1, 2008 (added)

July 1, 2011 (removed)

August 1, 2017 (added)

Australian dollar (AUD)

January 1, 1990

January 1, 1997

-

Brazilian real (BRL)

-

-

July 1, 2008

British pound (GBP)

January 1, 1990

January 1, 1997

-

Canadian dollar (CAD)

January 1, 1990

January 1, 1997

-

Chilean peso (CLP)

January 1, 2005

-

July 1, 2008

Chinese renminbi (CNY)

April 1, 2019***

-

April 1, 2019***

Offshore Chinese renminbi (CNH)

-

-

April 1, 2013*

Colombian peso (COP)

September 1, 2020

-

July 1, 2008

Czech koruna (CZK)

January 1, 2005

-

July 1, 2008

Danish krone (DKK)

January 1, 1990

April 1, 2014

-

Egyptian pound (EGP)

-

-

July 1, 2008*

European euro (EUR) January 1, 1990

October 1, 1998 (France)

October 1, 2003 (Italy added)

April 1, 2006 (Germany)

August 1, 2012 (Italy removed)

April 1, 2015 (Italy, Spain added)

-

Hong Kong dollar (HKD)

September 1, 2004

-

-

Hungarian forint (HUF)

January 1, 2005 (added)

November 1, 2013 (removed)

April 1, 2017 (added)

- July 1, 2008

Indian rupee (INR)

-

-

July 1, 2008*

Indonesian rupiah (IDR)

June 1, 2018 (added)

-

July 1, 2008

Israeli shekel (ILS)

January 1, 2012

-

July 1, 2008

Japanese yen (JPY)

January 1, 1990

May 1, 2005

-

Malaysian ringgit (MYR)

January 1, 2006

-

July 1, 2008

Mexican peso (MXN)

January 1, 2005

-

July 1, 2008

New Zealand dollar (NZD)

January 1, 1990

January 1, 2014

-

Nigerian naira (NGN)

-

-

April 1, 2013*

Norwegian krone (NOK)

January 1, 1990

-

-

Peruvian sol (PEN)

September 1, 2020

-

July 1, 2008

Philippine peso (PHP)

-

-

July 1, 2008

Polish zloty (PLN)

January 1, 2005

-

July 1, 2008

Romanian leu (RON)

September 1, 2020

-

April 1, 2013

Russian ruble (RUB)

April 1, 2014

-

July 1, 2008

Singapore dollar (SGD)

January 1, 2002

-

-

South African rand (ZAR)

January 1, 2005 (added)

May 1, 2018 (removed)

- July 1, 2008

South Korean won (KRW)

January 1, 2002

-

July 1, 2008

Swedish krona (SEK)

January 1, 1990

January 1, 1997

-

Swiss franc (CHF)

January 1, 2010

-

-

Taiwan dollar (TWD)

January 1, 2006 (added)

January 1, 2012 (removed)

- April 1, 2013*

Thai baht (THB)

January 1, 2002 (added)

March 1, 2007 (removed)

July 1, 2008 (added)

- July 1, 2008

Turkish lira (TRY)

April 1, 2014 (added)

October 1, 2016 (removed)

- July 1, 2008

US dollar (USD)

January 1, 1990

January 1, 1997

-

Note: *Eligible for the Bloomberg Emerging Markets Local Currency Government Universal Index only. ** Italy was removed from the WGILB on

August 1, 2012 due to the credit rating rule for the WGILB Indices at the time. Eurozone ascension currencies that were historically index eligible

before adopting the EUR include the Slovak koruna (“SKK”) and the Slovenian tolar (“SIT”). ***On April 1, 2019, BISL began adding Chinese RMB-

denominated government and policy bank securities to the Global Aggregate Index over a 20-month period.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 17

Sector

Sector classifications categorize bonds by industry, government affiliation or some other

grouping of ultimate issuer risk. Granular by design, Bloomberg sector classifications are

hierarchal and allow for comparisons across sectors and within a specific peer group of issuers

with similar risk characteristics.

The fixed income asset class presents layers of complexity far greater than those in commonly

used equity classification schemes because of the diversity of issuer and security types. In

addition to corporate issuers and central government borrowers, a broad universe of

government-related entities (supranationals, local governments, government agencies) and

securitized structures with bankruptcy remote issuers or ring-fenced assets must be classified

appropriately.

The Bloomberg global

classification scheme uses

four pillars to classify bonds

by issuer type

Bloomberg Fixed Income Classification System

The Bloomberg global sector classification scheme is designed to reflect the large universe of

corporate, government, government-related and securitized bonds that comprise the global

fixed income investment choice set. In addition to corporate bonds, this universe also includes

central government sovereign/treasury bonds, government-related or quasi-sovereign bonds,

and securitized bonds backed by a pool of assets rather than the unsecured credit of an issuer.

6

The indices’ sector classification scheme has been modified over the years to recognize the

evolution of certain industries and security types where the existing classification scheme was

not representative of relevant peer groups. Additionally, increased granularity has been added

for sectors that have grown and where meaningful distinctions have become warranted.

7

Index-eligible bonds are divided into one of four broad categories: treasury, government-

related, corporate and securitized. Within each broad sector, there are up to three additional

layers depending on the depth and heterogeneity of issuers within the market. The indices’

global sector classification scheme can be found in Figure 3.

8

A table with classification codes is

provided in Appendix 5.

Figure 4

Bloomberg Fixed Income Classification System (as of the date of this document)

Class 1 Class 2 Class 3 Class 4

Treasury

Government-Related

Agencies

Government Guarantee

Government Owned

No Guarantee

Government Sponsored

Local Authorities

Sovereign

Supranational

Corporate Industrial

Basic Industry

Chemicals, Metals & Mining, Paper

Capital Goods

Aerospace & Defense, Building Materials, Construction Machinery,

Diversified Manufacturing, Environmental, Packaging

Communications

Cable & Satellite (called Media Cable prior to July 2014), Media &

Entertainment (called Media-Non-Cable prior to July 2014), Wireless,

Wirelines

Consumer Cyclical

Automotive, Consumer Cyclical Services, Gaming, Home Construction,

Leisure (called Entertainment prior to July 2014), Lodging, Restaurants,

Retailers

Consumer Non-Cyclical

Consumer Products, Food & Beverage, Healthcare, Pharmaceuticals,

Supermarkets, Tobacco

6

The sector classification scheme is designed to classify issuer types. It does not make distinctions based on country of risk (such as emerging vs. developed market) or

security type (taxable vs. tax-exempt municipals).

7

One key consideration in the definition of sector and sub-sector peer groups is size. Additional granularity can always be offered to isolate issuers with similar risk

characteristics, but for index purposes it is important that a particular sector or sub-sector is not too sparsely populated to facilitate relevant comparisons.

8

The Bloomberg Fixed Income Classification System has been designed for fixed income securities and may at times diverge from the Bloomberg BICS classification

scheme, which was designed for equities.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 18

Class 1 Class 2 Class 3 Class 4

Energy

Independent, Integrated, Midstream, Oil Field Services, Refining

Technology

Transportation

Airlines, Railroads, Transportation Services

Other Industrial

Utility

Electric

Natural Gas**

Other Utility

Financial Institutions

Banking

Brokerage, Asset Managers,

Exchanges (called Brokerage

prior to July 2014)

Finance Companies

Insurance

Health Insurance, Life, P&C

REITS

Apartment, Healthcare, Office, Retail, Other

Other Financial

Securitized

MBS Pass-Through Agency Fixed-Rate

GNMA 30y, GNMA 15y, Conventional 30y, Conventional 20y,

Conventional 15y

ABS

Credit Card

Auto

Student Loans

Residential Mortgages

Whole Business

Stranded Cost Utility

ABS Other

CMBS

Agency CMBS

Non-Agency CMBS

Covered

Mortgage Collateralized

Pfandbriefe, Jumbo Pfandbriefe, Non-Pfandbriefe

Public Sector Collateralized

Pfandbriefe, Jumbo Pfandbriefe, Non-Pfandbriefe

Hybrid Collateralized

Other

Pfandbriefe, Non-Pfandbriefe

Sector Hierarchy and Definitions for Taxable Indices

The following section details the classifications used at the first, second, third and fourth levels

within the indices, where applicable.

The treasury sector includes

debt issued by central

governments in its native

currency

Treasury (Class 1)

The treasury sector includes native currency debt issued by central governments. These bonds

are backed by the full faith and credit of a central government and represent one of the largest,

most liquid segments of the global bond market. There are no sub-classifications under

treasury, though index users will typically use additional segmentations by country or currency

when evaluating this sector. Both nominal and inflation-linked native currency government debt

is classified within the treasury sector.

A minimum 50% ownership

rule is used to classify issuers

as government agencies

Government-Related (Class 1)

The government-related sector groups all issuers with government affiliations in a single

category. It has four sub-sectors: Agencies, Sovereign, Supranational and Local Authority. In the

case of Agencies (Class 2), there is further granularity at the Class 3 level.

● Agencies (Class 2): This broad category is designed to capture all issuers that are owned,

sponsored or whose payments are guaranteed by a government. The three sub-

classifications are:

○ Government Guaranteed (Class 3): Issues that carry direct guarantees of timely

payment of interest and principal from central governments or from government

agencies that carry direct guarantees from central government. Government ownership

is not a factor, although most entities will be government owned.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 19

○ Government Owned No Guarantee (Class 3): Issuers that are 50% or more owned by

central governments

9

but issue debt that carries no guarantee of timely repayment. This

includes direct ownership by governments, as well as indirect ownership through other

government owned entities. This sector also includes state-owned entities that operate

under special public sector laws. Entities that are less than 50% government owned are

classified in the appropriate corporate bucket, unless the entity fits the definition of

government sponsored.

○ Government Sponsored (Class 3): Entities that are less than 50% owned by central

governments and that have no guarantee, but carry out government policies and benefit

from “closeness” to the central government. Evidence of closeness includes government

charters, government-nominated board members, government subsidies for carrying

out “social” policies, provisions for lines of credit and government policies executed at

sub-market rates with accompanying economic support from the government.

● Local Authority (Class 2): Debt issued directly by local authorities and by entities that are

50% or more owned by one or more local authorities. In the US market, taxable municipal

bonds, including Build America Bonds (BABs), fall into this category. Entities less than 50%

owned by a local authority will be classified within the appropriate corporate bucket.

● Sovereign (Class 2): The sovereign sector contains debt issued directly by central

governments, but denominated in a currency other than the governments’ native one. Due

to the issuer’s inherent foreign currency risk, investors often classify these bonds separately

from native currency treasury debt.

● Supranational (Class 2): This sector covers international organizations whose stakeholders

extend beyond a specific nation.

Corporate (Class 1)

The corporate classification and accompanying hierarchy is the most detailed component of the

Bloomberg Indices’ sector classification scheme. It is a global scheme that has been developed

and refined over the years to categorize issuers across geographic markets based on their

primary lines of business, revenue streams and operations that are used to service their debt.

Classifications are frequently reviewed by the index group in response to market events,

changes in an issuer’s ownership structure, mergers and acquisitions, divestitures, or changes in

the primary line of business. New classifications may be added on an as-needed basis if a large

segment of the market exhibits a well-defined risk profile that is not categorized in the existing

scheme, though these types of changes are uncommon.

While some fixed income sectors may appear comparable to equity sectors, they are not

interchangeable and are often different in definition, composition and placement within a

broader hierarchy. The indices’ bond classifications are specific to the global debt market and

consist of peer group definitions that include publicly traded issues, as well as debt issued by

privately held companies that may have different issuance patterns.

The corporate sector is categorized into three broad categories at the second level of the

classification scheme: Industrial, Financial Institutions and Utilities. Further classifications at the

third and fourth levels offer additional granularity for cross-sector and peer group comparisons.

The corporate Class 3 and Class 4 sub-sectors are:

● Industrials (Class 2)

○ Basic Industry (Class 3): Class 4 sub-sectors include Chemicals, Metals & Mining and

Paper.

○ Capital Good (Class 3): Class 4 sub-sectors include Aerospace & Defense, Building

Materials, Construction Machinery, Diversified Manufacturing, Environmental and

Packaging.

○ Communications (Class 3): Class 4 sub-sectors include Cable & Satellite (called Media-

Cable prior to July 2014), Media & Entertainment (called Media Non-Cable prior to July

2014), Wireless and Wirelines.

9

The 50% ownership threshold provides a clear and objective delineation between government-related and corporate issuers. The rule promotes consistency in

implementation and is based on measurable ownership information, which is generally publicly available.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 20

○ Consumer Cyclical (Class 3): Class 4 sub-sectors include Automotive, Consumer

Cyclical Services, Gaming, Home Construction, Leisure (called Entertainment prior to

July 2014), Lodging, Restaurants and Retailers.

○ Consumer Non-Cyclical (Class 3): Class 4 sub-sectors include Consumer Products,

Food & Beverage, Healthcare, Pharmaceuticals, Supermarkets and Tobacco.

○ Energy (Class 3): Class 4 sub-sectors include Independent, Integrated, Midstream

(added in July 2014), Oil Field Services and Refining.

○ Technology (Class 3)

○ Transportation (Class 3): Class 4 sub-sectors include Airlines, Railroads and

Transportation Services.

○ Other Industrial (Class 3)

● Utilities (Class 2)

○ Electric (Class 3)

○ Natural Gas (Class 3)

○ Other Utility (Class 3)

● Financial Institutions (Class 2)

○ Banking (Class 3)

○ Brokerage, Asset Managers and Exchanges (Class 3)

○ Finance Companies (Class 3)

○ Insurance (Class 3): Class 4 sub-sectors include Health Insurance, Life and P&C.

○ REITS (Class 3):

10

Class 4 sub-sectors include Apartment, Healthcare, Office, Retail, and

Other (all Class 4 sub-sectors added in July 2014).

○ Other Finance (Class 3)

Securitized (Class 1)

The securitized sector is designed to capture fixed income instruments whose payments are

backed or directly derived from a pool of assets that is protected or ring-fenced from the credit

of a particular issuer (either by bankruptcy remote special purpose vehicle or bond covenant).

Underlying collateral for securitized bonds can include residential mortgages, commercial

mortgages, public sector loans, auto loans or credit card payments.

11

There are four main sub-

components of the securitized sector: MBS Pass-Through, ABS, CMBS and Covered.

● MBS Pass-Through (Class 2): Fixed income structures that pool residential mortgage loans

with similar characteristics into a mortgage backed security and then allocate principal and

interest payments of underlying loans to bond holders. This sector includes agency and

non-agency issuers, but only agency issuers (FNMA, FHLMC and GNMA) are eligible for the

indices. Beginning July 2019, the indices reflect both 45- and 55-day delay Freddie

securities to reflect the UMBS initiative.

○ Agency Fixed-Rate (Class 3): Sub-sectors include GNMA 30 Year, GNMA 15 Year,

Conventional 30 Year, Conventional 20 Year, and Conventional 15 Year.

○ Non-Agency (Class 3): This classification captures non-agency mortgage pass-throughs

in the US and mortgage pass-throughs denominated in non-USD currencies.

● ABS (Class 2): Within ABS, Class 3 sub-sectors are based on collateral types, though not all

are represented in fixed- or floating-rate indices: auto, credit card, residential mortgages,

stranded cost utility, student loans and whole business.

12

10

Industrial issuers that have reorganized or are structured as REITS for tax purposes are classified within their respective industrial peer group.

11

Instruments such as CMOs that package other bonds into a new security are not index-eligible.

12

ABS home equity loan sector was retired on October 1, 2009, and manufactured housing sector was retired on January 1, 2008. Starting from May 1, 2021, the ABS

sector also includes motorcycle ABS (under the Auto ABS class), equipment ABS (under Other ABS class), and device payment plan (also under Other ABS class).

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 21

● CMBS (Class 2): CMBS are backed by commercial real estate loans or multi-family

properties. Effective July 2014, Class 3 sub-sectors differentiate between agency CMBS and

non-agency CMBS. Other index classifications are used in this market (CMBS 2.0, ERISA-

eligible, etc.) to segment the asset class further, but they are not part of the core

classification scheme.

● Covered (Class 2): Covered bonds are recourse debt instruments that are secured by a

ring-fenced pool of assets on an issuer’s balance sheet (commercial real estate, residential

mortgages, public sector loans or other assets).

13

Investors having recourse to the originator

is the defining difference between covered bonds and ABS.

14

Securities that are issued

under the Pfandbriefe Act in Germany and similar bonds in other jurisdictions (non-

Pfandbriefe) are classified as covered bonds under this definition.

○ Mortgage Collateralized (Class 3): Bonds collateralized by residential and commercial

real estate. Class 4 sub-sectors include Pfandbriefe, Jumbo Pfandbriefe and Non-

Pfandbriefe. Danish MBS are classified as Non-Pfandbriefe.

○ Public Sector Collateralized (Class 3): Bonds collateralized by public sector loans.

Class 4 sub-sectors include Pfandbriefe, Jumbo Pfandbriefe and Non-Pfandbriefe public

sector loans.

○ Hybrid Collateralized (Class 3): Bonds collateralized by a combination of public sector

loans, mortgages and/or other assets.

15

○ Other (Class 3): Bonds collateralized by single asset classes other than real estate or

public sector loans. Two Class 4 sub-sectors distinguish between Pfandbriefe and Non-

Pfandbriefe.

Bloomberg looks at several

factors when assigning a new

classification or reviewing a

current classification

Sector Assignment and Reclassifications

The Bloomberg Data group looks at a number of factors when assigning a Fixed Income sector

classification or reviewing a current classification. These include an issuer’s business lines and

sources of revenue, as well as an evaluation of comparable companies with similar risk profiles

or organizational structures. Sector classification can change due to various factors:

● Corporate Actions: In the case of corporate actions, such as a merger, acquisition or spin-

off, the classifications may be updated to better reflect the business lines of the new

entities.

16

● Change in Government Ownership: A move between corporate and government-related

may result from a decrease or increase in a government’s ownership stake.

● Evolution of Business Lines: If the business lines of a corporate entity shift, it could be

reclassified to reflect its new peer group.

Issuers with diverse business lines can present a challenge when cases can be made for

multiple classifications. Whether assigning a classification to a new issuer or reviewing

classifications of existing ones, Bloomberg evaluates all publicly available information on a

given entity to assign the most appropriate classification.

13

For purposes of rules clarity, the Covered Bond Index will exclude bonds that primarily contain fixed income securities issued by third parties (other than the issuer) in

the cover pool.

14

The category includes “structured covered bonds,” for which securitization techniques have been used to enhance the rating of the covered bonds, but the issuing

entity is usually not bankruptcy remote. Structured covered issues are not governed by national covered bond legislation and regulation, while covered bonds are,

where such guidelines exist. These bonds fall under “Other Covered” at the Class 3 level.

15

There are no hybrid Pfandbriefe.

16

Due to potential uncertainty and complications surrounding corporate actions, changes to classifications for index purposes take effect after the close of transaction

rather than following the announcement.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 22

Figure 5

Bloomberg Sector Classification Scheme: Before and After January 1, 2005

Municipal Index Classifications

Due to the unique nature of this asset class, Bloomberg uses a classification scheme that is

unique to the risk factors associated with the municipal market for related indices.

Municipal Index Classifications

For the tax-exempt municipal market, bonds in the Bloomberg Municipal Bond Index are

categorized into the following sector types:

1. Pre-Refunded: Bonds backed by special US Treasury issuance or other high quality bonds;

this supersedes all other sector designations.

2. General Obligation (“GO”): Bonds that have not been pre-refunded and are backed by the

credit of the issuing entity, not a directed revenue stream or project.

3. Revenue: Bonds that have not been pre-refunded that are backed by revenue generating

projects as a funding source.

Municipal bonds are also classified into municipal-specific classes 2 and 3. The scheme is

detailed in Figure 5.

Government Credit Securitized

Treasury Government-Related

Corporate

Securitized

MBS Pass-through

ABS

CMBS

Pfandbriefe

Other Mortgage

Non-Corporate

Foreign Agency

Foreign Local

Government

Sovereign

Supranational

Industrial

Utility

Financial

Institutions

Agency

Local Government

Treasury Corporate

MBS Pass-through

ABS

CMBS

Covered

Industrial

Utility

Financial

Institutions

Agency

Mortgage

Collateral

Public Sector

Hybrid

Government

Guarantee

Government

Owned No

Guarantee

Government

Sponsored

Other

Local Authority

Sovereign

Supranational

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 23

Figure 6

Municipal Index Classification Scheme

Class 1 Class 2 Class 3

Municipals

State

State

Local

County

City

Tax Backed District

School District

Guaranteed

Education

Higher Education

Private Schools

Charter Schools

Prim & Sec Education

Student Loans

Health Care

Hospitals, Treatment/ Research Centers

Nursing Homes/ Assisted Living

Continued Care Retirement Center

Lease

Education Lease

Ad Valorem Lease

Government Lease

Appropriation

Housing

Single Family

Multi Family

Student Housing

IDR/ PCR

Tobacco

Gas Forwards

Resource Recovery

Economic and Industrial Development

Utilities

Electric and Public Power

Combined Utilities

Water/ Sewer

Transportation

Airport

Tollroad, Bridges & Tunnels

Farebox (Mass & Rapid Transit)

Port/ Marina

Parking Facilities

Non-Toll

Special Tax

Sales Tax

Bond Bank

Special Assessment

Miscellaneous Tax

Income Tax

Tax Increment Financing

Mello Roos

Other

Other

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 24

Credit Quality

The credit rating of a security is a key classification in the fixed income market, with a clear

distinction between investment grade (Baa3/BBB- or higher) and high yield (Ba1/BB+ or lower)

debt.

An added layer of complexity exists in the assignment of credit quality because the rating

agencies used in index classifications (Moody’s, Standard & Poor’s and Fitch) may assign a

different rating to the same security. BISL uses multiple ratings sources to classify securities,

including bond-level ratings from the different agencies, issuer ratings, and foreign or local

currency sovereign debt ratings.

BISL uses the middle rating of

Moody’s, S&P and Fitch to

determine a security’s credit

classification for most indices

Bloomberg Index Rating

BISL uses the middle rating of Moody’s, S&P and Fitch

17

to determine a security’s credit

classification or index rating for most bonds.

18

This essentially works as a “two-out-of-three” rule

because at least two of the three agencies need to rate a bond as investment grade to qualify it

for investment grade indices (or two agencies to rate it as high yield to qualify it for the high

yield indices).

If only two agencies rate a security, the more conservative (lower) rating is used. If only one

rates a security, that single rating is used.

19

The only indices that additionally employ a fourth rating agency, DBRS, in the determination of

index rating are the Canadian Aggregate family of indices. For these indices only, index rating is

determined by removing the highest and lowest of four ratings, and taking the lower of the two

remaining ratings. If fewer than four ratings are available, the standard methodology based on

three or fewer ratings is used, as described above.

Below are three index rating examples :

Bloomberg Index Bond Rating Example 1:

Moody’s Rating: Ba3

S&P Rating: BBB-

Fitch Rating: BB

Index Rating: Ba2/BB

Despite S&P’s investment grade rating of BBB-, this issue is still classified as high yield for

index purposes since Moody’s and Fitch have it rated as high yield.

Bloomberg Index Bond Rating Example 2:

Moody’s Rating: Ba1

S&P Rating: BBB

Fitch Rating: BBB+

Index Rating: Baa2/BBB

This issue has an index rating of Baa2/BBB because the Moody’s rating (lowest) and the

Fitch rating (highest) would be dropped.

Bloomberg Index Bond Rating Example 3:

Moody’s Rating: A3

S&P Rating: BBB+

Fitch Rating: NR

Index Rating: Baa1/BBB+

This issue has an index classification of Baa1/BBB+, as Fitch rating is not available, and the

more conservative S&P rating of the two available ratings is taken.

17

Bloomberg does not currently supplement the ratings of Moody’s, Fitch and S&P with that of other ratings agencies for most asset classes or sub-sets of the global

fixed income markets for index purposes (except the Canadian Aggregate Indices). However, the use of additional ratings sources is reviewed with index users on a

periodic basis through the annual governance process.

18

Though S&P and Fitch ratings are used in determining an index rating, Moody’s nomenclature is used for all bonds. Ratings may be solicited or unsolicited.

19

This methodology for Canadian indices is effective beginning on August 1, 2018.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 25

Sovereign Ratings

Local currency treasury and hard currency sovereign issues are classified using the middle

sovereign

20

rating from Moody’s, Fitch and S&P for all outstanding bonds even if bond-level

ratings are available.

21

The middle sovereign rating is applied uniformly as the “index rating” at

the bond level across all treasury bonds, even if bond-level ratings show as NR for one or more

agencies.

22

This rule is also applied in cases where issuers that are backed by a central

government have ratings for some, but not all securities at the bond level. To prevent split

ratings for such issuers, the sovereign rating may be applied as the index rating to all bonds

from that issuer.

23

Credit quality may be

assigned using an expected

rating, issuer rating or

sovereign rating when bond-

level ratings are unavailable

Classifications when Bond-Level Ratings are Unavailable

In certain cases, bond-level ratings for index-eligible securities may not be available, while other

assessments of credit quality, such as expected ratings or issuer-level ratings, are. The following

rules are used to assign credit quality in such situations. They may be applied for short-term

purposes where the absence of a rating may be temporary or in longer-term cases where a

rating agency only offers issuer-level ratings, not bond-level ratings.

Use of Expected Ratings

When the credit rating assigned by a rating agency is referred to as “expected,” it generally

indicates that a rating has been assigned based on the agency’s expectations of receiving final

documentation from the issuer. Once the final documentation is received and reflects the

agency’s expectations, the expected rating is converted to a final rating. Expected ratings at

issuance may be used to ensure timely index inclusion or to classify split-rated issuers properly.

For example, if a bond has one confirmed high yield rating and one confirmed investment

grade rating, a third unconfirmed rating may be used to prevent unnecessary index turnover

between high yield and investment grade indices once the third rating is confirmed.

Issuer Ratings

For unrated senior securities from issuers with other index-eligible bonds, BISL may apply the

issuer rating that exists on any existing senior bond. For unrated subordinated securities, BISL

may apply the issuer subordinated rating. In cases where there is no subordinated rating,

subordinated bonds will be excluded from the indices. In both cases, the middle issuer rating

will be displayed at the security level as the “index rating”, while the ratings for each agency will

be displayed as NR. Issuer ratings are not used in cases where there are confirmed bond-level

ratings from at least one agency.

Ratings for Pfandbriefe

German Pfandbriefe are assigned ratings that are one full rating category above the issuer’s

unsecured debt rating.

Average Quality at the Index Level

A linear numeric system is used to average the bond-level index ratings. The index rating of

each bond is assigned a numeric value from 2 to 24, and the constituents’ numeric ratings are

market value weighted to arrive at the aggregate average quality for the index (Figure 6).

Figure 7

Numeric Value of Quality Ratings

20

The long-term local currency sovereign rating is used for treasury issues; the long-term foreign currency sovereign rating is used for sovereign issues for all currencies

except USD and CAD. For sovereign bonds denominated in USD and CAD, bond-level ratings are used.

21

For example, Japan’s sovereign rating is assigned to all Japanese government, government-guaranteed Japanese agency and local government securities

denominated in JPY. Similarly, all US MBS pass-throughs are assigned the US government rating for all agencies, even though the MBS pools themselves are not

explicitly rated.

22

US Agencies are assigned the same rating as US Treasuries.

23

If the local sovereign debt of a currency is not eligible for the Global Aggregate Index, then no other securities denominated in that currency will be eligible,

regardless of the securities' issue-level ratings.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 26

Numeric Value Index Rating Moody Rating S&P Rating Fitch Rating

2

AAA

AAA

AAA

AAA

3

Aa1

Aa1

AA+

AA+

4

Aa2

Aa2

AA

AA

5

Aa3

Aa3

AA-

AA-

6

A1

A1

A+

A+

7

A2

A2

A

A

8

A3

A3

A-

A-

9

Baa1

Baa1

BBB+

BBB+

10

Baa2

Baa2

BBB

BBB

11

Baa3

Baa3

BBB-

BBB-

12

Ba1

Ba1

BB+

BB+

13

Ba2

Ba2

BB

BB

14

Ba3

Ba3

BB-

BB-

15

B1

B1

B+

B+

16

B2

B2

B

B

17

B3

B3

B-

B-

18

Caa1

Caa1

CCC+

CCC+

19

Caa2

Caa2

CCC

CCC

20

Caa3

Caa3

CCC-

CCC-

21

Ca

Ca

CC

CC

22

C

C

C

C

23

D

D

D

D

24

NR

NR

NR

NR

Defaulted Securities

For index purposes, a security is considered to be in default if: 1) the company files for

bankruptcy; 2) a bond is in “Technical Default” (e.g. has missed an interest or principal payment

or is in covenant violation) which has neither been cured within the applicable grace period nor

subject to the terms of an applicable forbearance/standstill agreement; or 3) the bond is

subject to cross-default provisions that stipulate when an event on another bond or loan could

trigger a default on the subject security. Defaulted bonds from corporate issuers are not eligible

for Bloomberg Indices, such as the US High Yield Index. Once a corporate bond is identified as

in default from an index standpoint, its accrued interest is set to zero, reversing out any accrual

posted since the last coupon payment, and it will have a negative coupon return. The bond

continues to be priced in the Returns Universe until month-end, at which time it will exit the

index. When securities default, index users will see all analytics, such as duration and spread,

set to zero.

In the case of missed payments on treasury and sovereign debt issued by central governments,

debt is often restructured through a revision to the debt terms agreed upon by the government

and bond holders. Due to the increased probability that sovereign debt will come out of default

through restructuring or an exchange, BISL allows defaulted sovereign bonds to remain eligible

for indices, such as the EM USD Aggregate Index.

For US municipals, a bond is considered to be in default if an issuer misses a principal and/ or

an interest payment.

Minimum Amount Outstanding

The amount outstanding or par value of a bond determines not only the notional balance on

which an issuer pays interest, but the amount of principal to be repaid by an issuer at the end of

a bond’s term. Par amount outstanding is seen as a measure of relative liquidity and as a proxy

of the float available for investors to purchase, with larger bonds viewed as more accessible

than smaller ones. For purposes of inclusion, Bloomberg Indices have a minimum amount

outstanding rule that is applied on a security-level basis. This is sometimes referred to as a

minimum “liquidity” rule.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 27

The minimum amount outstanding size for the Global Aggregate Index, US Aggregate Index

and EM Local Currency Government Index are the same. Different minimums are used for the

High Yield, Inflation-Linked, EM Hard Currency and Municipal Index families.

Minimum market size at the country level is also a consideration for flagship inflation-linked

(“WGILB”) and EM local currency indices, but not a consideration for other broad-based indices,

such as the US Aggregate or Global Aggregate Indices. Additionally, no minimum issuer size is

applied to corporate or government-related issuers in standard benchmark indices.

Local currency minimums are

based on market-specific

issuance and benchmark issue

sizes, and a comparison of

thresholds across markets to

ensure similar size standards

Local Currency Minimums

Global Aggregate and EM Local Currency Minimum Issue Sizes

Bloomberg Indices use fixed minimum issue sizes for each local currency bond market. For

each currency included in the Global Aggregate and EM Local Currency Government Index

families, local currency minimums are established based on a number of factors, including

market-specific issuance patterns and benchmark issuance sizes, and a comparison of existing

minimum thresholds across markets to ensure similar size standards are applied. The local

currency minimums are reviewed on an annual basis to ensure an accurate representation of

each market. Figure7 lists minimum amounts outstanding for the Bloomberg Fixed Income

Indices.

Rules for Indices with Higher Minimum Issue Sizes

Higher liquidity versions of the Global Aggregate and EM Local Currency Government Indices

use adjusted local currency minimums for each currency that are scaled up proportionally to the

same desired percentage increase. This scaling factor is determined by dividing the new

desired minimum for a specific currency by its current Global Aggregate minimum, which is

then applied to all currencies eligible for the benchmark.

For example, setting a USD or EUR minimum issue size of 500mn represents a 2/3 increase over

their Global Aggregate minimum issue size of 300mn. This higher liquidity threshold is then

applied proportionally to all other Global Aggregate currency minimums, reflecting the same

percentage increase from 300mn to 500mn. The adjusted JPY minimum in this example would

be increased to JPY58.3bn from its current JPY35bn.

Investors who prefer market-specific local currency minimums that are not scaled proportionally

across the entire benchmark may do so in a customized index.

Figure 8

Fixed Local Currency Minimums for Bloomberg Indices

Region Currency

Global Aggregate/Global Treasury/EM

Local Currency Minimum (000s)

Inflation-Linked

Minimum (000s)

High Yield Corporate

Minimum (000s)

Americas

Global Aggregate

Eligible

USD

300,000

500,000

150,000

CAD

150,000

600,000

-

MXN

10,000,000

300,000 (UDI)

-

COP

1,000,000,000

1,000,000 (UVR)

-

PEN

1,000,000

-

-

CLP

100,000,000

1,000 (UF)

-

EM Local Currency

Eligible

BRL 1,000,000 400,000 -

EMEA

Global Aggregate

Eligible

CHF

300,000

-

100,000

CZK

10,000,000

-

-

DKK

2,000,000

5,000,000

-

EUR

300,000

500,000

100,000

GBP

200,000

300,000

50,000

HUF

200,000,000

-

-

ILS

2,000,000

1,500,000

-

NOK

2,000,000

-

500,000

PLN

2,000,000

500,000

-

RON

1,000,000

-

-

RUB

20,000,000

-

-

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 28

Region Currency

Global Aggregate/Global Treasury/EM

Local Currency Minimum (000s)

Inflation-Linked

Minimum (000s)

High Yield Corporate

Minimum (000s)

SEK

2,500,000

4,000,000

1,000,000

EM Local Currency

Eligible

EGP

3,000,000

-

-

HRK

3,000,000

-

-

NGN

100,000,000

-

-

TRY

2,000,000

500,000

-

ZAR

2,000,000

400,000

-

Asia

Global Aggregate

Eligible

AUD

300,000

700,000

-

CNY

5,000,000

-

-

HKD

2,000,000

-

-

IDR

2,000,000,000

-

-

JPY

35,000,000

50,000,000

-

KRW

500,000,000

500,000,000

-

MYR

2,000,000

-

-

NZD

500,000

1,000,000

-

SGD

500,000

-

-

THB

10,000,000

20,000,000

-

EM Local Currency

Eligible

CNH

1,000,000

-

-

INR

25,000,000

-

-

PHP

20,000,000

-

-

TWD

15,000,000

-

-

* The minimum for MBS generics is USD1bn.

Inflation-Linked Indices

The minimum issue size for inflation-linked government bonds in developed markets is higher

than their nominal counterparts in the Global Treasury Universal Index and slightly lower for

emerging markets (Figure 8). For most developed markets, actual issue sizes of index-eligible

government debt are substantially higher than the index minimums.

US Aggregate Minimum Issue Sizes

US Aggregate minimum issue sizes have evolved to reflect the growth and size of the USD-

denominated bond market and benchmark issuance sizes (Figure 9).

● The US Aggregate Index has a minimum issue size of USD300mn for government, credit

and covered bonds.

● For MBS securities, the minimum generic size in the US Aggregate is USD1bn as of April

2014.

● For ABS and CMBS securities, the original deal size minimum is USD500mn and the eligible

tranche size minimum is USD25mn. CMBS securities also must be part of a deal that has at

least USD300mn currently outstanding.

24

Other Bloomberg Flagship Indices

High Yield Indices

Issue sizes for the high yield market are generally lower than investment grade issue sizes, and

the minimums for these benchmarks reflect that.

● For the US High Yield Corporate Index, the minimum issue size is USD150mn.

● For the Pan-European High Yield Index, the minimum issue sizes for each eligible currency

are EUR100mn, GBP50mn, CHF100mn, SEK1bn and NOK500mn.

25

24

The Bloomberg Indices also offer broader CMBS indices that have no minimum tranche size rule and apply only original and current deal size constraints.

25

Prior to 2014, the Pan-European HY minimums were set as one-third of Global Aggregate minimums for each eligible currency.

Bloomberg Fixed Income Indices December 15, 2023

Bloomberg Fixed Income Index Methodology 29

EM Hard Currency Indices

For the EM Hard Currency Aggregate Indices, higher minimum issue sizes are used:

USD500mn, EUR500mn and GBP500mn. These are applied to the EM Hard Currency

Aggregate family only.

26

Municipal Indices

The tax-exempt US municipal market has substantially lower issuance sizes than the taxable

bond market. The minimum issue size for the flagship Bloomberg US Municipal Index is

USD7mn, and bonds must be issued as part of a transaction of at least USD75mn. For the High

Yield Municipal Index, the minimum issue size is USD3mn, and bonds must be issued as part of

a transaction of at least USD20mn.

Additional market size

minimums are used for EM

Local Currency Government

and WGILB Indices

Minimum Market Size